If you didn’t know already, we’re here to increase competition and disrupt the investment platform market by offering an easy, beautiful experience with the best possible fees — it’s kind of in the name!

The FCA’s interim report on investment platforms made for interesting reading in this context. So we thought we’d write a bit about how we at Freetrade stack up against the regulator’s own best practices and how we differ from everyone else on the market. 🙏

The first, important takeaway is that more people than ever are managing their own investments, with assets under management by the industry doubling since 2013.

In individual terms, circa 2.2 million more people have started investing independently. This is great and reflects well on the impact the internet and technology has had in empowering consumers.

But it’s not all good news. ⛈

Paying an advisor or wealth manager to take care of your affairs means they deal with all of the nitty gritty and can be held to account for good service and performance. Going direct makes it much cheaper but also brings responsibility and some risk.

Turning away from costly managers, average investors depend on broker platforms which vary widely in price, style and quality and are often difficult to compare.

The FCA has indicated some concerns with this dynamic.

Five specific points were raised:

The difficulty and cost of switching

Nothing screams old world more than arbitrary penalty fees for customers who decide to take their business elsewhere. As a customer-centric broker, obviously we’ll do everything we can to help persuade you to stay and resolve any issues as quickly as possible.

However, everyone’s needs are different and we understand sometimes people may prefer to go elsewhere — it’s a competitive market, after all. It doesn’t sit right with us that users be financially penalised for making such a decision. As you might expect, Freetrade will never charge exit fees. 💪

The FCA are considering banning exit fees, overall. It’s good to know we won’t have to change a thing.

The difficulty of comparing complex pricing models

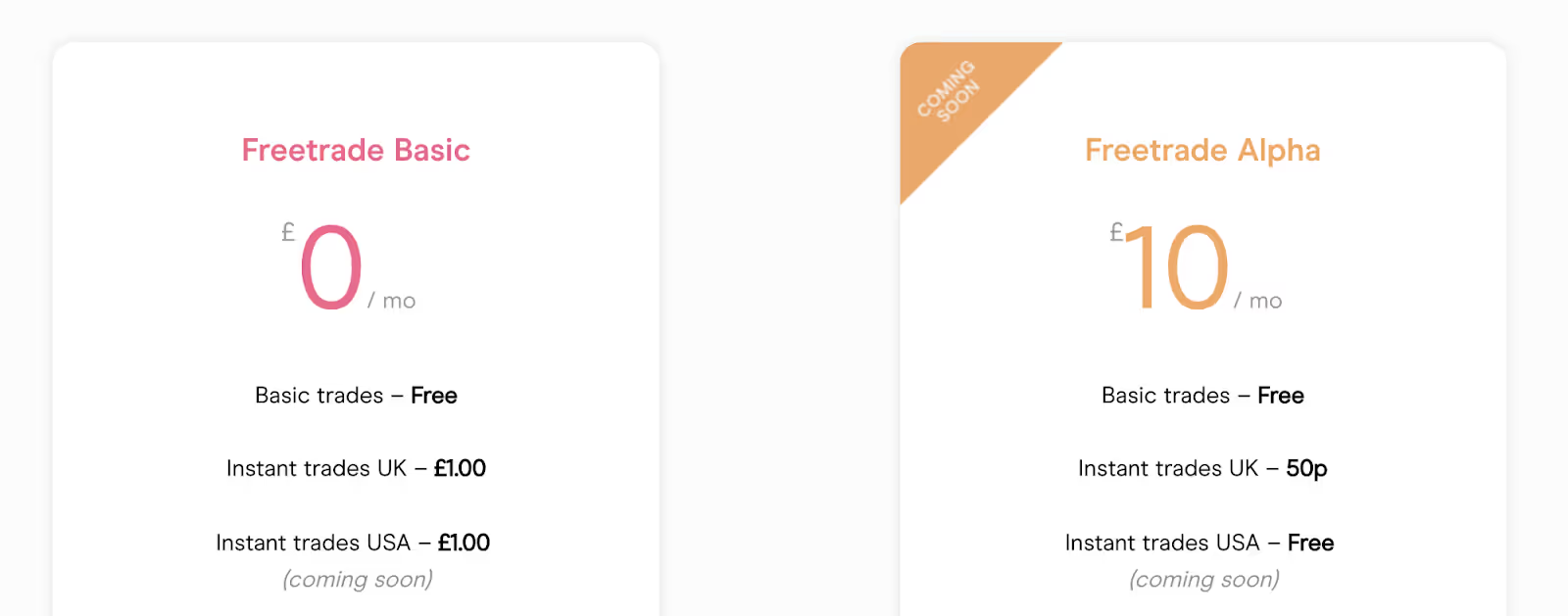

We announced the pricing model we’ll launch with in April. We’re proud to be the only broker with a pricing model built to align with our customers’ needs. Our priority isn’t just offering the best prices and value, but also the most transparency.

It’s easy and simple to understand and compare to other brokers (our community have been discussing it avidly).

It’s notable that all of our account and custody charges are either free or fixed, so you won’t pay more as your investments increase in value. The same goes for commissions on instant orders: they’re a low, transparent cost which doesn’t vary over time or encourage you to trade more than you actually want to (no churning here 😉).

The only percentage-based fee you will find on Freetrade is the conversion fee for foreign exchange when you want to trade a stock in a currency other than sterling. This is unavoidable at the moment, but we’re transparent that it’s objectively pegged to the interbank rate and therefore represents a fair and competitive fee relative to the industry.

The FCA has rightly brought attention to the fact that such simple pricing information is not the norm. An average UK broker’s pricing model will generally consist of:

- Percentage-based custody fees that are capped at a sterling amount, which is not always easy to calculate.

- Huge trading commissions that vary based on either the volume you trade or the underlying instrument if the broker has a special deal with a fund provider.

- Foreign exchange rates that are higher than they should be and not pegged to anything in particular.

- Other obscure, ad-hoc charges that may or may not apply to your account depending on how you use it.

- This information is listed in complex form across several different pages

At best, it’s time-consuming to compare brokers and at worst it leads to inertia by consumers as it doesn’t seem worth the hassle and cost to consider switching.

Combined with the exit penalties described above, the whole thing is a bit of a mess — but it’s great to see the FCA bring attention to this and start to drive improvement. 👏

The difficulty of assessing the risk of model portfolios

At launch we’ll simply offer the ability to trade stocks and ETFs without direct guidance or insight. This encourages customers to do their own research, however, the ability to put investments on ‘autopilot’ and benefit from support and analysis is something we’ve got on our roadmap.

The FCA have pointed out that such predefined model portfolios don’t always explain clearly what the actual risk is to the consumer is. If something is described as ‘cautious’, this probably implies lower volatility in return for lower expected return, however, there may be a difference between the customer’s expectation and the portfolio’s holdings and performance.

This is something we’ll consider carefully when we begin to develop our offering beyond just trade execution. 🤓

Dealing with large cash balances that do not attract interest or investment returns

We won’t pay interest on cash balances held with us, and we think this is fair given that we don’t charge custody fees for stocks and shares. However, it’s a good point that the FCA makes in that brokers should be proactive in communicating to clients that large cash balances might be better off stored in places where they do attract meaningful interest, and that in the long run cash will not see anywhere near the same return as the stock market.

We’re looking into what notifications we can give users to remind them things like their cash balance being unusually high over an extended period. Watch this space!

Keeping customers on a higher price plan when they can no longer utilise some services

This was the point most picked apart by the media — so-called ‘orphan clients’ who were once advised through a platform, and remain with that platform without their advisor, are still on a higher pricing plan. They’re essentially being charged for services they cannot use, by definition.

This doesn’t feel comfortable and, again, we’re glad the FCA is driving change by encouraging consumers to break out of their apathy and demanding brokers prioritise the needs of clients over collecting fees.

We’re not set up to allow advisers to manage client accounts, but this may change in the future. If we ever do, we would of course implement best practices and never sneakily overcharge customers if their circumstances change — but that should be obvious. 😉

Those were the five key points of practice that the FCA brought up.

However, interestingly the FCA also paid specific regard to features other than costs when analysing the market and competitiveness.

Higher prices, they say, can be justified if it provides genuine benefit for the customer. This is a fair point, but we’d argue that it’s possible to lead the market on top quality features and on prices. That’s our plan anyway. 🔥

Here are the other points we reckon you should keep in mind when choosing a broker.

Customer service availability

This is one of the core components of a brokerage from a customer perspective. All brokers facilitate trading in one form or another, but how quickly and attentively will they react when things don’t go to plan? With lots of money at stake and markets moving all the time, sometimes good, old human interaction is what you need to get things moving again.

We’re investing heavily in this part of our stack, using the best live chat technology and recruiting the brightest people to help keep everything running smoothly. We’re already set up to answer questions and help with support queries for the app.

You can expect quick response times, helpful answers and the odd emoji. Nothing else will do.

Usability — look and feel of the experience

This one is easy and I’ll just let the app do the talking; there’s no way my words can do it justice. Compared with other brokers it’s simply chalk and cheese.

Product range and wrappers

ISAs are around the corner, with SIPPs and other wrappers like the Lifetime ISA firmly on the long term roadmap. We think this is a good way to start off and will react to user demand in terms of what to prioritise here.

The instruments you can buy and sell with Freetrade are collectively considered our Stock Universe 🌎 — this is open and transparent and additions will be driven by the community (you can make a request here).

We’re also working on adding more international markets that trade in multiple currencies over the long term. We want to offer what our customers want to invest in, its as simple as that. Anyone for crypto?

Tools and features for research and portfolio management

We take analytics features very seriously. Recently, we’ve been debating the merits and drawbacks of measuring investment performance on money-weighted vs. time-weighted basis. We understand the need to make data digestible and useful to the average investor. In addition, some users need and want a step up in analytics and market metrics.

As a mobile-first platform, we also have to contend with the parameters of screen size and interface design. This is our bread and butter as a technology firm, making our product as sophisticated as possible while keeping it accessible and elegant.

We’re providing the basics from launch, with a firm commitment to improve the feature-set of the product over time, in line with user demand.

Guidance and suggestions for what to invest in

As above, as soon as we’ve made the investing process as simple and easy as possible, we’ll move on to helping customers choose what to invest in using objective analysis and some handy insight. We think this is important but naturally comes later than the services we’ll offer at launch.

TL;DR

To bring this novel to a quick conclusion, I think it’s fair to say that the FCA are cottoning on to the tricks old world brokers have been at for decades.

We no longer live in a market of paper share certificates and telephone deals; it’s time for all platforms to stop acting (and charging) like it. There are a few slight glimmers of organic change, but way too slow for our liking.

We’re going to rock the boat and accelerate it massively.

~Calum, Compliance Officer

We’re on a mission to bring fee-free investing to Europe and beyond. 🔥

This should not be read as personal investment advice and individual investors should make their own decisions or seek independent advice. This article has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is considered a marketing communication.When you invest, your capital is at risk. The value of your portfolio can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future results.Freetrade is a trading name of Freetrade Limited, which is a member firm of the London Stock Exchange and is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales (no. 09797821).

.avif)