You could say ISAs have a bit of an image problem.

They are one of the government's more generous inventions and could really be an important part of your financial toolbox alongside bank and savings accounts.

But ask a passerby about ISAs and you'll likely get an odd look (perhaps deservedly). ISAs are not as well known as they should be.

There's no real reason for this, ISAs are not some sort of exclusive club. In fact, each of us has an allowance to put into ISAs each year.

We think it's time more people knew about ISAs and how to make the most of these tax wrappers based on your own individual circumstances.

So we're going to spill the beans on the ISA allowance.

Before we start it’s important to know this article isn’t personal investment advice and that tax rules for ISA accounts can change and their benefits depend on your individual circumstances.

It’s also important to understand that the value of your investments and any income you receive from them can rise and fall, and you may get back less than you invested.

The ISA allowance (or you might hear it called the ISA limit) is the total amount of money you can put into ISAs in a tax year.

Why put money into an ISA?

The tax treatment on your investments in an ISA is different from that in a general investment account (or GIA). Because inside an ISA, you won't pay income tax on any UK dividends or interest and you won't need to worry about capital gains tax if you sell your investments for a profit.

Why do ISAs need a limit?

Because while the government is keen for us to save more and incentivises us to do so through tax-efficient investment accounts, it still has to collect some taxes. Which it does on investments outside of your ISA's annual allowance limit.

ISA allowance history

ISAs were introduced by the UK government in 1999 to help savers and investors shelter savings from tax and encourage us to save and invest more.Back then the yearly allowance for ISAs was £7,000 but now, your personal tax allowance on an ISA is much more generous.

How much is the current ISA allowance?

The ISA allowance for the current tax year is £20,000.

How you make use of the ISA allowance is up to you.

You can split it across different types of ISAs (say a cash ISA and a stocks and shares ISA) or you could put the whole £20,000 into a stocks and shares ISA.

A tax year runs from 6 April to 5 April the following year, which means the current tax year 2024/25 ends on 5th April 2025 at midnight.

After this point, we're into new tax year territory and a new ISA allowance.

How does the ISA allowance work?

There’s no need to complicate the ISA allowance.

HMRC sets the ISA allowance each year and it’s up to us how we use it.

The main thing to know about the ISA allowance is that it’s very much a case of use it or lose it.

Each year we’re given an ISA allowance and if we don’t use it up by the ISA deadline or tax year-end i.e. 5th April 2025 at midnight it’s gone. From the 6th April, we’re into a new tax year and a new ISA allowance.

So for anyone wondering, “if I don’t use my full ISA allowance can I carry it over to the next tax year?”

The answer is unfortunately no.

How to make the most of your ISA allowance

Here are our five top tips to help you make the most of your ISA allowance.

1. Use it, don’t lose it

How much of the £20,000 ISA allowance we will use will be different. It all comes back to how much we can afford to set aside for savings and investments.

Whether you're investing £100 or £10,000, start by looking at how much cash you need to pay for any short-term debt like credit cards and any regular payments, like rent, groceries and rainy day savings.

Doing this should help you understand what you can and can't afford to invest.

2. Invest it

Cash is a big thing in ISA land. The majority of people in the UK have a cash ISA over any other kind of ISA. Just because you have a cash ISA doesn't mean you can't have another kind of ISA too, though. After all, even when you look under the hood of the other types of ISA, most of them hold cash too.

Cash plays an important role in your finances but when it comes to growing your savings over the long term, cash is unlikely to be the answer.

There are two reasons why.

The first is to do with inflation (or the general rise in prices over time).

Unless the interest rate you're getting on your cash savings is higher than the rate of inflation, your money is likely to be worth less in the future.

On paper (or screen) your £1,000 will still say £1,000 but how much that £1,000 will buy you (if prices are rising) will have dropped.

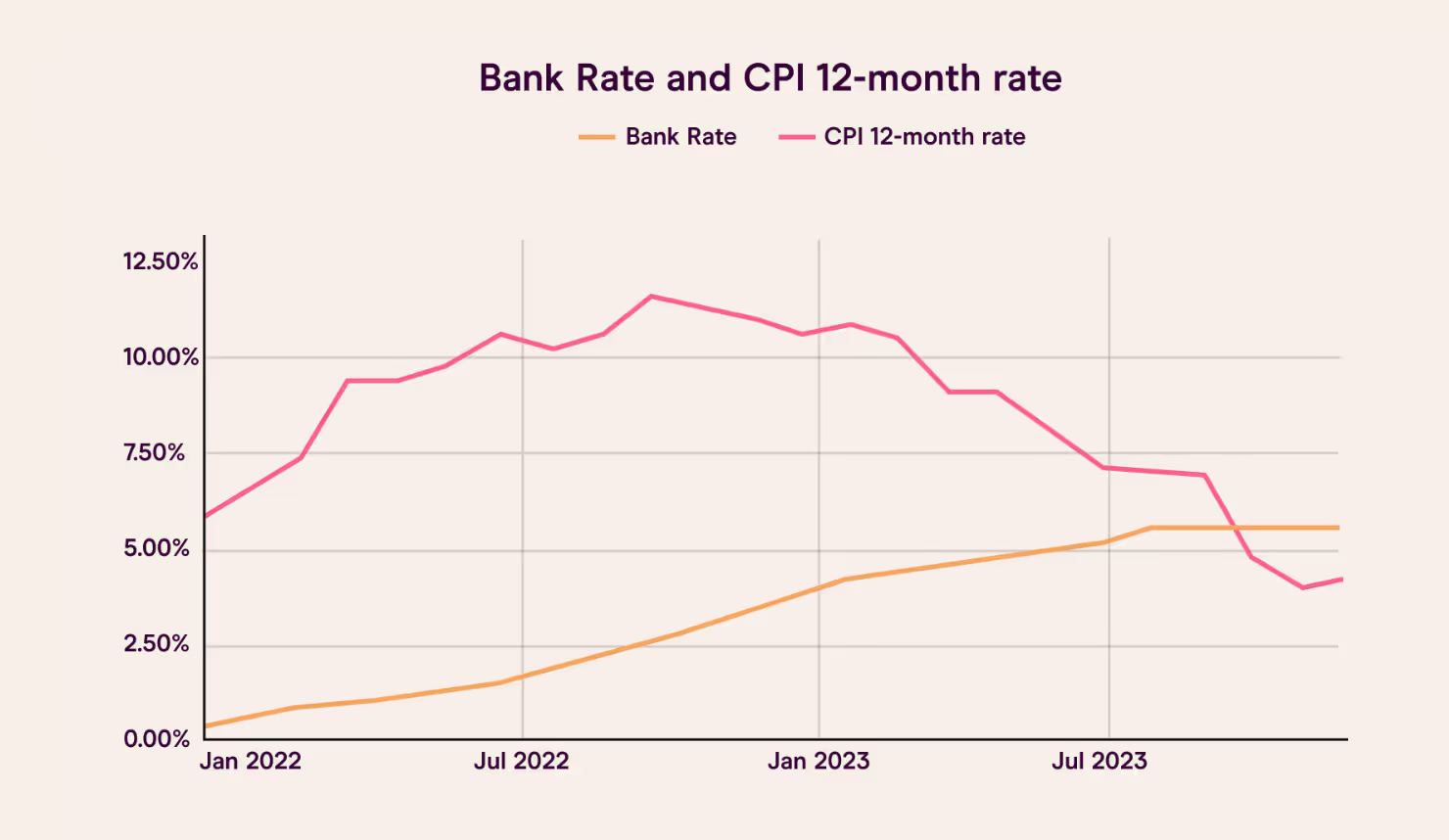

After more than a decade of interest rates sitting at record lows, the last two years saw a shift as the Bank of England steadily increased interest rates to the current high of 5.25% (as of 10 April 2024). But this wasn’t necessarily a win for cash savers. Inflation far outstripped interest rates until October 2023, meaning their cash was eroding in real terms.

We should say the current levels of inflation are unusual by recent historic standards and the result of a few pandemic induced factors. How long prices are likely to keep rising is also hotly debated.

October 2023’s drop in inflation brought good news to cash savers - their cash stopped eroding in value thanks to CPI dipping to 4.6% whilst interest rates remained at 5.25%.

So, why invest when cash savings are generating returns?

Keeping some cash in a savings account is important as it gives you easy access for those ‘rainy day’ moments. Cash is safe, but the trade off is that you haven’t taken any investment risk so you might not gain as much as you would in a long-term well-diversified stocks and shares ISA, but you might not lose as much either.

Investing is for the long-term (think five years or more) and historically has been a better way to grow your wealth because the stock market can generate returns that outstrip the risk-free rate and inflation.

Scrutinising what you hold in cash and whether it should really be in cash is a good first step. Will you need to use this cash in the immediate future, say within the next few years?

Here’s an example of how inflation could hurt your spending power over the long run

The longer you leave it, the less your £1,000 is worth.

Disclaimer: This table is just for illustrative purposes only and does not use real inflation rates.

The second reason comes back to an opportunity to grow your savings

When we invest we're putting our money to work. Our aim is for it to be worth more in the future and to get a better return than if we had left it as cash in the bank.

Take investing in shares as an example.

When you buy shares in a company, you're becoming an owner of that company. You've chosen it because you think the company and in turn, the value of your share of it will grow over time.

However, as an owner, you'll share in the downs as well as ups of the business. In exchange for taking on this risk, investors have historically been rewarded with a higher rate of return on their investment.

When you're investing, the longer you can leave your investments, the better. A good rule of thumb is to be prepared to keep your money invested for at least five years.

3. Make it a habit

Making investing a regular habit comes with a few benefits.

Once you do you’ll get used to it being a regular thing you set money aside for each month.

And when you do it regularly you’ll likely become less worried about when you invest too.

Timing the market is notoriously difficult and lots of research has shown that dipping in and out of the market will likely hurt your investment returns.

You might miss the worst days but you’ll also miss the best days.

The key thing to remember is that stock markets are meant to move. But over the long term and despite short term dips, markets tend to rise and have historically rewarded investors who have stayed put.

4. Check fees aren’t eating it

There’s no reason why investing should be costly.

Charges eat into your investment performance, so it's important to understand how much you are being charged by your ISA provider and what for.

Here are the ISA charges to understand:

- Account charges - how much does an ISA account cost? Is it a flat fee or a percentage fee that could grow as your investment does?

- Trading commission - how much does it cost to place a trade?

- Foreign exchange fees - how much are you charged to buy overseas investments?

- Ongoing charges - how much does it cost to invest in ETFs, investment trusts and funds?

- Exit charges - will you be charged by your ISA provider to leave?

💡 Percentages. Scrutinise every percentage charge you see. Percentages can often mean your charges will grow as the value of your investments do.

5. Do it all again

This is the easy bit. After making the most of your current ISA allowance, it’s time to do it again next tax year.

ISA allowance FAQs

Cash ISA vs stocks and shares ISA, which one is best?

The answer could be both.

You could think about a cash ISA as a place for your savings that you know you’ll need to use over the next few years. Then for any longer term savings, you could think about investing them with a stocks and shares ISA.

There is no right or wrong, start with what your goal is for your ISA, and go from there.

Can I have more than one stocks and shares ISA?

You can have as many stocks and shares ISAs as you like.

Previously, you could only contribute to one stocks and shares ISA at a time.

However, as of 6 April 2024, this rule was scrapped and you can now contribute to multiple cash ISAs and stocks and shares ISA each tax year.

Be wary of fees, though. Paying into multiple ISAs may cost you more in fees than if you had a single ISA.

People that have been on the ISA scene for a while may have old stocks and shares ISAs they’ve opened with other providers in previous tax years, so these are fine to hold on to.

It’s worth remembering that you can combine old ISAs by transferring them all to one provider.

Before transferring an ISA it’s important to understand whether you’ll be worse or better off by doing so. For example, check for any exit fees that your current provider might charge and that you can actually transfer.

How can I check if I have used my ISA allowance?

You’ll be able to check directly with your ISA provider.

If you have an ISA with Freetrade, you can see how much of your ISA allowance you’ve used in your app. Simply toggle to your ISA, then tap the Account tab.

When does the ISA allowance reset?

The ISA allowance resets at the start of each tax year, which means the current ISA allowance (for the tax year 2024/25) will reset on the 5th April 2025 at midnight.

How does transferring affect my ISA allowance?

ISA transfers do not count as new ISA subscriptions.

If you’re transferring ISAs from previous tax years, it will have no impact on your ISA allowance for the current tax year.

If you’re transferring ISAs from the same tax year then you’re remaining ISA allowance won’t change.

What happens if I take money out of my ISA?

While we’d encourage you to stay invested for as long as feasible, you can take your money out of a stocks and shares ISA whenever you like.

If you do take any money out it’s important to know you will lose your tax-free allowance.

What does this mean?

Let’s say you’ve added £16,000 to your stocks and shares ISA this tax year and you withdraw £2,000. While the amount left in your ISA is now £14,000, the remaining amount you can put into your stocks and shares ISA this year is still £4,000.

It’s worth noting that while this is true for most ISAs (including Freetrades stocks and shares ISA) it isn’t always the case. In your ISA explorations, you might also come across something known as a flexible ISA and the rules here are slightly different.

With a flexible ISA, you can take money out of your ISA and put it back in again without it affecting your annual ISA allowance.

Using the same example, having added £16,000 to your ISA and taken out £2,000 in the same tax year, with a flexible ISA, you’d still be able to add £6,000 to your ISA for the rest of the tax year.

What happens if I exceed my ISA allowance?

The good news is if your stocks and shares ISA is with Freetrade you won’t be able to go over your ISA limit.

If you have ISAs elsewhere, you’ll have to keep track of how much you’ve subscribed and where you are versus the limit.

If you've accidentally paid too much into an ISA, you won't get any tax relief on any payments over the ISA allowance you've made. And if you do exceed your ISA allowance, HMRC will get in touch with you after the end of the tax year to let you know what you need to do to correct it.

What happens to my ISA allowance if I die?

If you die, your ISA allowance goes too.

However, your spouse or civil partner can inherit your ISA’s tax-free status as a one-off boost.

This means if you have an ISA worth £40,000, when you die your spouse or civil partner will get an additional one-off ISA allowance of £40,000 as well as the standard ISA allowance (which is £20,000 this year).

What do this year's changes in UK capital gains allowances mean for my ISA?

This tax year (from April 6, 2024) the capital gains tax allowance was halved from £6,000 to just £3,000.

If your investments grow in an ISA though, then you'll be sheltered by any capital gains tax anyway.

Here's an example of what that might look like:

What do this year's changes in UK dividend allowances mean for my ISA?

This tax year (from April 6, 2024) the dividends tax allowance was reduced from £1,000 to £500.

If your investments grow in an ISA though, then you'll be sheltered from UK dividend tax, no matter how high they go.

Here's an example of how that could pan out:

💡 Learn more:

Understand how ISAs work with our stocks and shares ISA rules guide.

The role of cash in your portfolio

The (more realistic) ISA millionaire

Build your financial knowledge and be in a better position to grow your wealth. We offer a wide range of financial content and guides to help you get the insight you need. For example, learn how to invest in stocks if you are a beginner, how to make the most of your savings with ISA rules or how much you need to save for retirement.

.avif)

.webp)