.avif)

When the Covid fog clears the stock market will find a new worry to latch onto. But there will be no bell to let us know this one is finally finished and something else deserves our attention.

That risks preventing us from truly reflecting on the effects of the pandemic on UK companies. And if that seems unlikely, it might be that we’ve already fallen into this very trap.

Some UK firms have been able to use the past year to their advantage, either by refining their proposition or making the most of our move online. But some have benefited simply from investors suddenly having bigger things to attract their attention than some problems at a corporate level.

We should remember though that life will return to normal at some stage. And before we move past the Covid narrative, we need to question whether 2020 truly changed these businesses for the better or if it masked problems that are likely to reappear.

Here are a couple of examples where investors shouldn’t let 2020 tell the whole story.

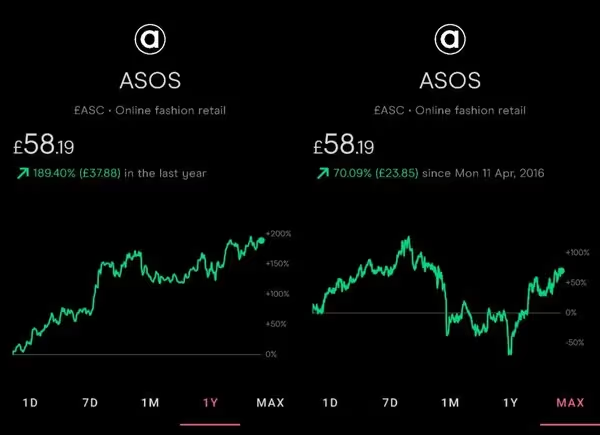

ASOS: did last year prove the model or did it just get lucky?

It rolls off the tongue to say online retailers cleaned up during the pandemic. ASOS has clearly benefited from shoppers stuck at home but go back to before the face masks and it’s a different story.

Before the Topshop acquisition and the mammoth share price hike since lows last March, ASOS was in real trouble.

Three profit warnings in 2018 and 2019 and a grossly mismanaged distribution rollout in the US and Europe showed that, despite its promise, there was still a lot of learning to be done.

The result was a 57% share price fall from highs in March 2018 to the end of 2019.

That’s not the narrative we’re broadly used to from one of the UK market’s growth darlings. And it might be one investors are quick to forget.

Today’s interim results tell a rosier story after a year in which the share price has boomed.

Sales, profits and customer numbers soared, with the firm’s customer base reaching 24.9m in the past six months, including 1.5m newcomers.

Sales grew by 24% in the six months to the end of February and profits jumped to £106.4m from £30.1m this time last year.

Takings among the company’s 7m UK customers were a particular highlight, growing by 39%.

ASOS needs to use cash wisely

Ultimately, the results will be a relief for shareholders who would have expected the online business to boom last year.

But the question is how efficient the firm is at expanding from here.

ASOS acquired the Topshop, Topman, Miss Selfridge and HIIT brands in February for £395m and investors will want to see a return on that outlay quickly.

And that still might be a worry. In 2016, £1 of investment back into the ASOS business generated £6.50 of sales, but in 2020 that return fell to £2.80.

Some of that reinvested cash was put to use in areas yet to bear fruit like technology and warehousing but it will be a key point of focus for investors regardless of the pandemic.

Will the pandemic prove to be a paradigm shift?

This is the tricky see-saw investors have to manage now. At-home consumption trends during the pandemic were the kick in the tail the firm needed but there won’t always be a revenue defibrillator on hand to jolt life back into the business.

On the other hand, the pandemic did happen and it did accelerate our move online. Given the past 12 months, it’s hard to imagine a future without online retail specialists. The likes of ASOS and Boohoo have the fashion side of that sewn up for now.

Once the dust settles, ASOS’s high valuation could end up looking a bit more reasonable.

But the firm owes its shareholders some clear evidence that it’s passed the phase of avoidable mistakes like having goods turned away at US customs.

A good way to steady the nerves would be signs of a solid return on the money pumped into Topshop and emerging from the pandemic retail wreckage as a clear retail leader.

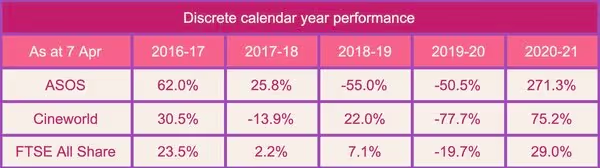

Cineworld

It might seem strange to say the pandemic masked Cineworld’s problems. After all, not letting film-goers anywhere near the big screens could only send the shares one way.

But that’s the big risk as we leave lockdown. Just as in the case of ASOS, we shouldn’t assume the problems that were there beforehand are suddenly gone now.

And Cineworld had its problems.

Shares hit recent highs in April 2019, long before last year’s existential threat to cinemas appeared.

But the writing was on the wall soon after.

In May 2019, Cineworld reported a sharp drop in sales as the flow of Hollywood blockbusters dried up. Revenues fell 9.4% with the US and the UK segments suffering particularly badly.

It showed just how dependent the screening industry is on big hit films. In years gone by, even low budget movies would play their part at the box office but the adoption of streaming services means we don’t have to go out for entertainment anymore - and we knew that before the pandemic.

The firm has slipped onto a lot of value investors’ radars over the past year as a result of the pandemic hit to trade.

But maybe shedding light on the problem is just what it needed.

Was lockdown just what Cineworld needed?

Bosses securing a £336 million cash lifeline in November seemed to put a bit of life back into shares.

Cineworld execs have more incentive than most to get the share price back up though.

Even with a third of shareholders voting against a plan that would see bosses split a £65m bonus pot if shares recover, it got the 50% it needed to be passed in January.

To get a £33m bonus Cineworld’s share price will have to reach 190p within three years – back to pre-pandemic levels. For the whole £65m it must hit 380p. Shares sit at 102p at the time of writing.

Many shareholders will be wondering why management needed such an incentive but it might be that the pandemic gave the firm the final kick it needed to enact a turnaround.

The lesson in all of this is to not see 2020 in isolation. It’ll be tempting but we really need to widen the frame to make sure the same old problems aren’t still there afterwards.

It may be that Cineworld recovers and, in the short term the share price is moving that way.

But the real question was present before the pandemic even began. What can it do to bring back customers and dissuade them from watching the straight-to-streaming movies at home, and only popping to the cinema when a huge franchise comes out?

Source:

- Asos's global growth potential still has much to offer investors, Investors’ Chronicle, 10 Mar 2021

Past performance is not a reliable indicator of future returns.

Make your money work a little bit harder with a tax-efficient investing account. First, learn the basics of how stocks and shares ISA works with our guide. Then, if you know that ISAs are right for you, go ahead and open an ISA account or transfer from another provider to start contributing regularly.

This should not be read as personal investment advice and individual investors should make their own decisions or seek independent advice. This article has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is considered a marketing communication.When you invest, your capital is at risk. The value of your portfolio can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future results.Freetrade is a trading name of Freetrade Limited, which is a member firm of the London Stock Exchange and is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales (no. 09797821).

.avif)