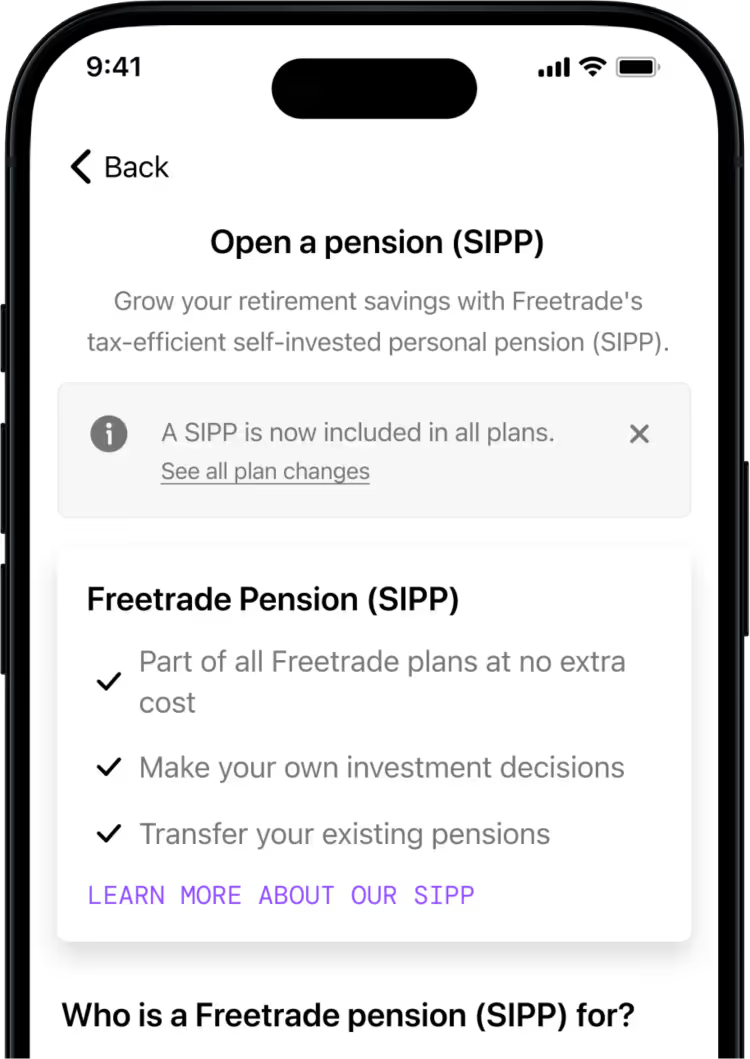

Self-invested personal pension (SIPP)

Take control with a free SIPP

Take control of your retirement pots with a self-invested personal pension (SIPP). Now available on all plans.

Capital at risk.

The value of your investments can go down as well as up and you may get back less than you invest. SIPP eligibility rules apply. Tax treatment depends on your personal circumstances and current rules may change.

A SIPP is a pension designed for you to save until your retirement and is for people who want to make their own investment decisions. You can normally only draw your pension from age 55 (57 from 2028), except in special circumstances.

At present, Freetrade only supports Uncrystallised Fund Pension Lump Sums (UFPLS) for customers who wish to withdraw funds from their SIPP after their 55th birthday. Each UFPLS withdrawal costs £240. We strongly encourage you to seek financial advice before making any withdrawals from your SIPP.

Pensions that are transferred to the Freetrade SIPP may lose the protected pension age benefit. This means that you will not be able to draw the monies from the Freetrade SIPP until you are aged 57. Please ensure you know what this means for you and the effect it may have on you and your savings. Check before you transfer a pension to us that we can accept your investments, you won’t lose any guarantees, and that you know what charges you may incur. Seek advice if you are unsure about making a transfer.

For your pension contributions, we'll claim the 'Basic Rate' tax relief from HMRC on your behalf and deposit it in your Freetrade SIPP account automatically.

It normally takes around 6-11 weeks from the contribution to the tax relief appearing in your account. The HMRC tax relief depends on your eligibility. You can read more about tax relief.

Costs are based on those published costs on the other providers’ websites as of 24 March 2026. They are shown for illustrative purposes only. For confirmation of their up-to-date charges and product information, you should visit their websites.

Calculations exclude interest on customer cash and do not include investment growth or tax relief. Annual percentage based charges and monthly fixed account fees are applied after UK and US trading fees and FX fees.

Freetrade: There are no commission charges per trade and no subscription fee on the Basic plan, which gives you access to a Stocks and Shares ISA, Self-Invested Personal Pension (SIPP), and General Investment Account (GIA). FX fees are 0.99% on Basic, reduced to 0.59% on Standard and 0.39% on Plus.

Hargreaves Lansdown: Subscription fee is based on the annual 0.35% charge on the value of shares held in a SIPP. This is capped at £12.50/mo. Fee per trade reduces, depending on the number of trades executed in the previous month, from £6.95 for up to 19 trades to £3.95 for 20 or more trades. The FX rate is tiered by transaction value: 0.99% for the first £10,000, 0.50% for £10,001–£24,999.99, and 0.20% for £25,000 or more.

Interactive Investor: Subscription fee is based on the Core plan at £5.99/mo, which allows for a maximum portfolio size of £100,000. For portfolios above this, customers are switched to the Plus plan, which costs £14.99/mo. The FX rate varies by plan: 0.75% on Core, 0.75% on the first £50,000 and 0.25% for over £50,000 on the Plus plan, 0.25% on the Premium plan.

AJ Bell: Subscription fee is based on the annual 0.25% charge on the value of shares held in a SIPP. This is capped at £10.00/mo. Fee per trade reduces, depending on the number of trades executed in the previous month, from £5.00 for up to 9 trades to £3.50 for 10 or more trades. The FX rate is tiered by transaction value: 0.75% for up to £10,000, 0.50% for £10,001–£20,000, and 0.25% for above £20,000.

Costs are based on those published costs on the other providers’ websites as of 24 March 2026. They are shown for illustrative purposes only. For confirmation of their up-to-date charges and product information, you should visit their websites.

Calculations exclude interest on customer cash and do not include investment growth or tax relief. Annual percentage based charges and monthly fixed account fees are applied after UK and US trading fees and FX fees.

Freetrade: There are no commission charges per trade and no subscription fee on the Basic plan, which gives you access to a Stocks and Shares ISA, Self-Invested Personal Pension (SIPP), and General Investment Account (GIA). FX fees are 0.99% on Basic, reduced to 0.59% on Standard and 0.39% on Plus.

Hargreaves Lansdown: There is a 0.35% charge on the value of shares held in the share dealing account, ISA and SIPP, capped at £12.50/mo for the all three accounts. Fee per trade reduces, depending on the number of trades executed in the previous month, from £6.95 for up to 19 trades to £3.95 for 20 or more trades. The FX rate is tiered by transaction value: 0.99% for the first £10,000, 0.50% for £10,001–£24,999.99, and 0.20% for £25,000 or more. The illustration assumes £6.95 trade per fee and 0.99% FX fee.

Interactive Investor: Subscription fee is based on the Core plan at £5.99/mo, which allows for a maximum portfolio size of £100,000. For portfolios above this, customers are switched to the Plus plan, which costs £14.99/mo. ii platform fees are charged per customer and have been allocated to GIA for modelling. The FX rate varies by plan: 0.75% on Core, 0.75% on the first £50,000 and 0.25% for over £50,000 on the Plus plan, 0.25% on the Premium plan.

AJ Bell: Subscription fee is based on the annual 0.25% charge on the value of shares held in a SIPP. This is capped at £10.00/mo. Fee per trade reduces, depending on the number of trades executed in the previous month, from £5.00 for up to 9 trades to £3.50 for 10 or more trades. The FX rate is tiered by transaction value: 0.75% for up to £10,000, 0.50% for £10,001–£20,000, and 0.25% for above £20,000.

Costs are based on those published costs on the other providers’ websites as of 24 March 2026. They are shown for illustrative purposes only. For confirmation of their up-to-date charges and product information, you should visit their websites.

Calculations exclude interest on customer cash and do not include investment growth or tax relief. Annual percentage based charges and monthly fixed account fees are applied after UK and US trading fees and FX fees.

Freetrade: There are no commission charges per trade and no subscription fee on the Basic plan, which gives you access to a Stocks and Shares ISA, Self-Invested Personal Pension (SIPP), and General Investment Account (GIA). FX fees are 0.99% on Basic, reduced to 0.59% on Standard and 0.39% on Plus.

Hargreaves Lansdown: Subscription fee is based on the annual 0.35% charge on the value of shares held in a SIPP. This is capped at £12.50/mo. Fee per trade reduces, depending on the number of trades executed in the previous month, from £6.95 for up to 19 trades to £3.95 for 20 or more trades. The FX rate is tiered by transaction value: 0.99% for the first £10,000, 0.50% for £10,001–£24,999.99, and 0.20% for £25,000 or more.

Interactive Investor: Subscription fee is based on the Plus plan at £14.99 per month, as the portfolio exceeds £100,000 after the first monthly contribution. The Plus plan includes one free trade credit per month, worth £3.99, which has been applied to UK trading in this calculation. The FX rate varies by plan: 0.75% on Core, 0.75% on the first £50,000 and 0.25% for over £50,000 on the Plus plan, 0.25% on the Premium plan.

AJ Bell: Subscription fee is based on the annual 0.25% charge on the value of shares held in a SIPP. This is capped at £10.00/mo. Fee per trade reduces, depending on the number of trades executed in the previous month, from £5.00 for up to 9 trades to £3.50 for 10 or more trades. The FX rate is tiered by transaction value: 0.75% for up to £10,000, 0.50% for £10,001–£20,000, and 0.25% for above £20,000.

Costs are based on those published costs on the other providers’ websites as of 24 March 2026. They are shown for illustrative purposes only. For confirmation of their up-to-date charges and product information, you should visit their websites.

Calculations exclude interest on customer cash and do not include investment growth or tax relief. Annual percentage based charges and monthly fixed account fees are applied after UK and US trading fees and FX fees.

Freetrade: There are no commission charges per trade and no subscription fee on the Basic plan, which gives you access to a Stocks and Shares ISA, Self-Invested Personal Pension (SIPP), and General Investment Account (GIA). FX fees are 0.99% on Basic, reduced to 0.59% on Standard and 0.39% on Plus.

Hargreaves Lansdown: Subscription fee is based on the annual 0.35% charge on the value of shares held in a SIPP. This is capped at £12.50/mo. Fee per trade reduces, depending on the number of trades executed in the previous month, from £6.95 for up to 19 trades to £3.95 for 20 or more trades. The FX rate is tiered by transaction value: 0.99% for the first £10,000, 0.50% for £10,001–£24,999.99, and 0.20% for £25,000 or more. See how Freetrade compares with Hargreaves Lansdown.

Interactive Investor: Subscription fee is based on the Plus plan at £14.99 per month, as the portfolio exceeds £100,000. The Plus plan includes one free trade credit per month, worth £3.99, which has been applied to UK trading in this calculation. Standard trading fees are £3.99 per trade on Core and Plus plans for UK and US shares and ETFs, reduced to £2.99 on the Premium plan. FX fees vary by plan, with 0.75% on Core, 0.75% on the first £50,000 and 0.25% above £50,000 on Plus, and 0.25% on Premium. See how Freetrade compares with Interactive Investor.

AJ Bell: Subscription fee is based on the annual 0.25% charge on the value of shares held in a SIPP. This is capped at £10.00/mo. Fee per trade reduces, depending on the number of trades executed in the previous month, from £5.00 for up to 9 trades to £3.50 for 10 or more trades. The FX rate is tiered by transaction value: 0.75% for up to £10,000, 0.50% for £10,001–£20,000, and 0.25% for above £20,000. See how Freetrade compares with AJ Bell.

Check before you transfer a pension to us that we can accept your investments, you won’t lose any guarantees, and that you know what charges you may incur. Seek advice if you are unsure about making a transfer. Always do your own research.

Pensions that are transferred to the Freetrade SIPP may lose the protected pension age benefit, if applicable to you, meaning that you will need to wait longer until you can draw monies from your Freetrade SIPP. Please ensure you know what this means for you and the effect it may have on you and your savings.

Freetrade won't charge you to transfer your pension to us, but please check with your existing provider what fees or restrictions may apply from them. We cannot provide you with any advice therefore it is your responsibility to ensure you are happy that transferring to the Freetrade Pension is right for you.If you're unsure if transferring your pension to Freetrade is right, you should take advice from a suitably qualified financial adviser. For more info, see our SIPP Key Features Document, Terms and Conditions, SIPP Charges and SIPP Declarations.

Here you'll find answers to the most frequently asked questions. If you have a question that's not listed, please contact support.

When you invest, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you invest.

Stocks and shares ISA

Junior stocks and shares ISA

Pension (SIPP)

General investment account

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.99% on non-GBP trades

1% AER on up to £1k uninvested cash

Mutual funds and gilts

Stocks and shares ISA

Junior stocks and shares ISA

Pension (SIPP)

General investment account

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.59% on non-GBP trades

2.5% AER on up to £2k uninvested cash

Mutual funds and gilts

Stocks and shares ISA

Junior stocks and shares ISA

Pension (SIPP)

General investment account

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.39% on non-GBP trades

3.5% AER on up to £3k uninvested cash

Mutual funds and gilts

Stocks and shares ISA

Junior stocks and shares ISA

Pension (SIPP)

General investment account

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.99% on non-GBP trades

1% AER on up to £1k uninvested cash

Mutual funds and gilts

Stocks and shares ISA

Junior stocks and shares ISA

Pension (SIPP)

General investment account

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.59% on non-GBP trades

2.5% AER on up to £2k uninvested cash

Mutual funds and gilts

Stocks and shares ISA

Junior stocks and shares ISA

Pension (SIPP)

General investment account

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.39% on non-GBP trades

3.5% AER on up to £3k uninvested cash

Mutual funds and gilts