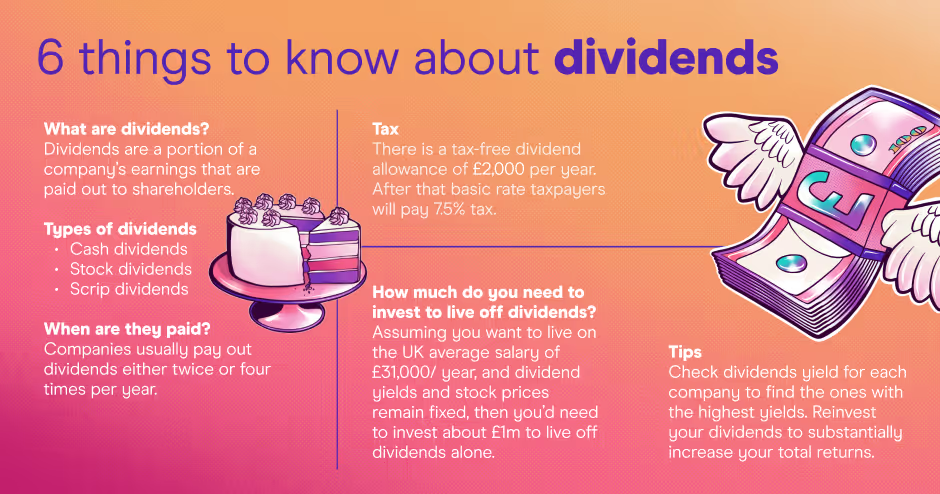

UK dividends are back. Payments to shareholders leapt to £34.9bn during the third quarter of this year. That’s an 89% uplift on 2020, when pandemic-induced belt tightening meant income payments halved in the corporate space.

The figures from Link Financial will be a huge confidence booster for income-seekers across the board. If there’s one thing dividend investors appreciate it’s consistency and after a very rough year for payouts, the taps being turned on again will be a big sigh of relief.

That said, after the virus took the whole market down in March last year, the road out of the pandemic has begun to look different in most sectors, sometimes markedly so.

Rising raw materials costs and shipping traffic jams are just two forces that could derail profits and put payouts in peril in 2022.

So, which income-payers are the professional investors sticking with?

Here are three investment trusts with clear dividend mandates, whose managers have been tasked with keeping those payouts online as they navigate their way out of 2021 and beyond.

Merchants Trust

Taking an income from UK shares has been a popular approach among British investors since the financial crisis. With bond yields nailed to the floor, climbing the risk scale into equities has been the only way to get a decent yield for most of us.

But how we choose to get that dividend income can throw up a bit of a problem.

Lift the bonnet on the majority of open-ended funds in the UK equity income sector and you’ll likely see the same old names and the same old strategies. If you aren’t careful you can snap up a few and end up doubling down when you thought you were diversifying.

What might set the Merchants Trust apart is its value approach, even if a few familiar names prop up the top 10 holdings.

Manager Simon Gergel looks for lowly-valued shares the market has either overlooked or ignored on purpose.

He buys where he thinks those sentiments are unfair or just don’t reflect reality, in the hope that the market will come round to his way of thinking and his shares will make a comeback.

It’s not generally a style that provides a stable income but a 39-year streak of consecutive dividend increases shows it can be done. And a current yield of 4.9% might be attractive if that value style continues to gain traction.

When the Merchant goes shopping

Alongside companies that could benefit from a sustained economic recovery in the UK, and increasing interest rate expectations, Gergel has recently added Tesco.

The UK’s leading supermarket now has a 27.5% market share according to Kantar, well ahead of second place Sainsbury’s (14.9%).

Its resilience during the pandemic has been a draw for the manager and stands out to him as a stock listed in ‘one of the cheapest major countries’ out there.

More relevant for dividend hunters are signs of a progressive policy of returning cash to shareholders. A recent announcement of plans to implement a £500m share buyback programme over the next 12 months follows a special dividend paid out in early 2021.

The portfolio addition diversifies some stalwart UK dividend-payers in the trust but it might not be enough to convince some ESG-minded investors to get on board.

Both British American Tobacco and Imperial Brands appear among the top names and won’t pass many sustainability screens. While both may offer attractive yields at the moment, they have a lot to do if their models are to survive the inevitable increased regulatory focus and health-oriented crackdowns, not to mention any tax hikes on their products in future.

Murray International

Bruce Stout’s global portfolio runs into a similar snag in its inclusion of cigarette firm Philip Morris. It may be a leader in the non-combustible smoking revolution but it’s unlikely to make it into a sustainability-led portfolio until it gets rid of the sin stock label.

For investors looking to be part of that turnaround rather than blacklisting it, Murray International might be a useful dividend source.

The manager scours the globe for high-quality companies with strong financials, aiming to grow income and capital over the long term for the trust’s investors.

In particular, Stout is drawn to opportunities in the US and emerging markets. That means the strategy might serve as a useful diversifier for UK-heavy portfolios or dividend-seekers drawing a blank beyond Blighty’s borders.

Read more:

Finding dividends on AIM

Four ‘sin-free’ dividend stocks

Sign up to Honey, our daily market newsletter

Not every company in the trust will be a clear dividend stock, Stout blends high yielders and growth-focused firms with the aim of achieving a mix of income and growth. With a current yield of 4.9% that strategy and exposure to non-UK assets might complement a few portfolios.

Global exposure can often prompt managers to find more ideas than they know what to do with, ending up in a bloated portfolio.

That’s not the case here, with Stout’s team whittling down the 13,000 prospective firms in the waiting room to a fund of around 40-60 names. Chief attributes among the chosen companies are resilient business models, unique advantages over the competition and experienced management teams.

The result is a portfolio containing Samsung, Unilever and Taiwan Semiconductor Manufacturing Co.

HICL infrastructure

If you want to diversify away from some of the big dividend-payers, alternative income sources like infrastructure might come in handy.

HICL infrastructure currently offers a 5.1% yield, generated through funding big projects across the UK and further afield, which produce a steady stream of income for the trust’s investors.

It was the first infrastructure investment company to be listed on the London Stock Exchange and its management team, InfraRed Capital Partners, has a history of investing in the space stretching back to 1990.

Schools, hospitals and care homes make up the bulk of the UK portfolio with around 70% of projects completed in partnership with the government.

The trust’s exposure to toll roads last year demonstrated one of the risks to investing in infrastructure - empty roads mean shallow coffers - but the relative stability that comes with government-backed initiatives will be attractive to many.

Inflation-conscious investors might also like the trust’s exposure to utilities like water and gas services, which make up around 10% of the portfolio.

As essential economic assets, they can often raise their prices in line with inflation and offset cost pressures other non-inflation linked projects might run into.

There is also a deliberate effort to include assets which support the UK’s transition to a net zero carbon economy. HICL has a 39% holding in the Walney Extension Offshore Wind Farm, which should provide investors with a steady income stream for the next 19 years.

Freetrade is on a mission to get everyone investing. Whether you’re just starting out or an experienced investor, you can buy and sell thousands of UK and US stocks, ETFs and investment trusts commission-free on our trading app. Download our iOS trading app or if you’re an Android user, download our Android trading app to get started investing.

This should not be read as personal investment advice and individual investors should make their own decisions or seek independent advice. This article has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is considered a marketing communication.When you invest, your capital is at risk. The value of your portfolio can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future results.Freetrade is a trading name of Freetrade Limited, which is a member firm of the London Stock Exchange and is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales (no. 09797821).

.avif)

.avif)

%252520(1).avif)