The self-employed pension gap

Self-employment. The benefits are obvious.

So much so that more and more people are choosing to work for themselves.

Between 2000 and 2020, the number of self-employed workers in the UK rose by 50%, peaking at just over 5m before the outbreak of COVID-19 (1). And while that’s dropped off to around 4.3m now, it’s still a big number.

We’re talking not far off the size of the entire public sector in the UK (2).

But, while the public sector is generally well looked after when it comes to their pension and retirement, it’s a different story for the self-employed.

When it comes to saving for retirement, the challenges of being your own boss are less well advertised.

Incomes fluctuate, there’s no luxury of auto-enrolment and the maze that HMRC calls guidance is not always the most digestible.

The worrying result is that around only a third of self-employed people are paying into a pension (4).

That’s not only a huge chunk of the workforce not saving for retirement at all but a huge number of people missing out on the best investment growth ingredient of all. Time.

The good news is there is still time to get things sorted. Starting with this guide, we’re going to simplify the world of self-employed pension options.

Before diving in, it’s important to understand that pension and tax rules can and do change. Any tax treatment depends on your individual circumstances.You also need to be comfortable with the fact that the value of your investments can fall as well as rise, so you might get back less than you originally invested.

Why it's important to save into a pension when you’re self-employed

Pensions and saving for retirement are crucial things for everyone to be thinking about. But they are particularly important for self-employed workers because:

- You may not have a workplace pension scheme to fall back on

- The State Pension is unlikely to cut it and you have to wait longer to get it

- Personal pension tax benefits can be generous

- The later you start saving into a pension the less opportunity you are giving your pension pot to grow

Different types of pension for the self-employed

Personal pensions - a pension you set up yourself. You add money and the government tops up your contributions via tax-relief.

State Pension - a weekly income provided by the UK government as long as you are eligible and you’ve reached State Pension Age.

Workplace pensions - these are set up by employers and are only an option to the self-employed that operate as a limited company. Of course, you could have one from an old job.

Personal pensions for the self-employed

Personal pensions are the go-to pension for the self-employed.

Without a workplace pension to fall back on and the prospect of a slim state pension, personal pensions fill an important gap for the self-employed.

There are three different types of personal pension to choose from and they all offer a few key things:

Control

You control how much and when you contribute to your pension, giving you more flexibility in case your income fluctuates.

Top-ups

The government tops up any contributions you make via tax relief (subject to certain limits of course… it’s the government).

Opportunity to grow your retirement savings

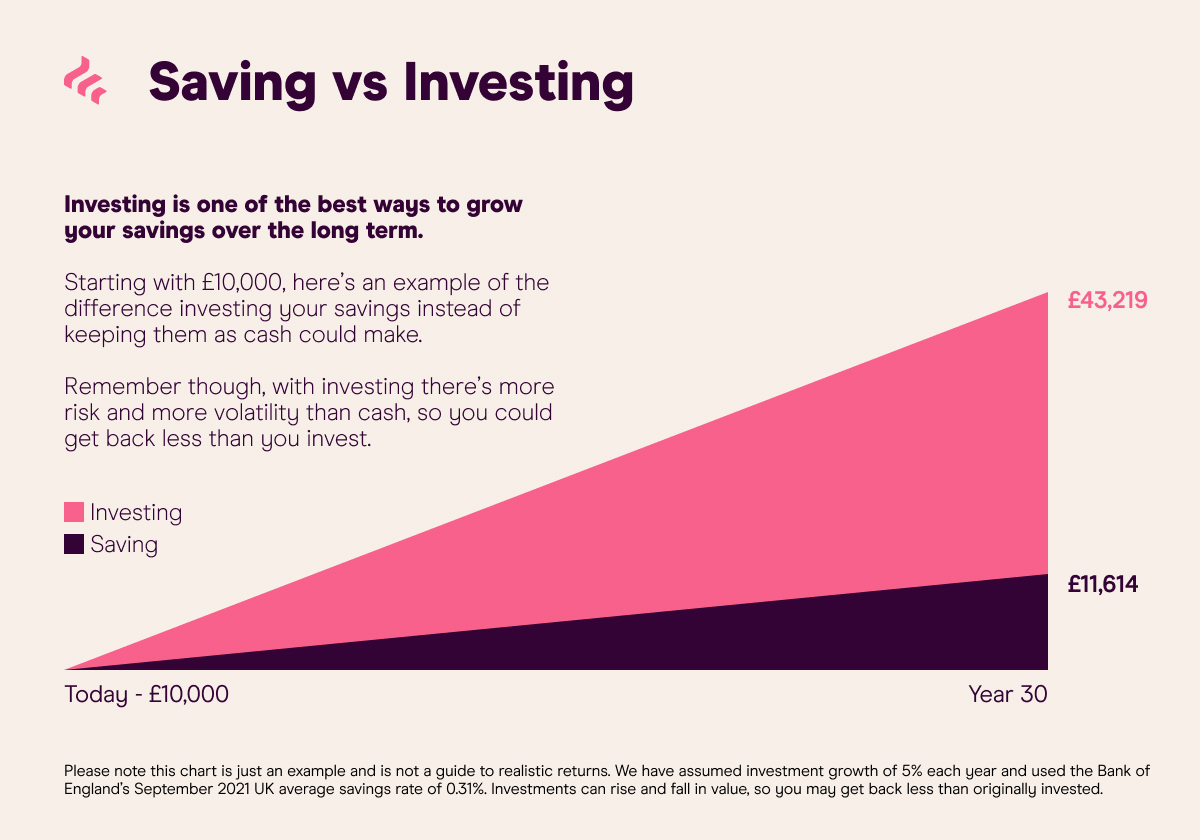

Investing is one of the best ways to grow your savings over the long term, left as cash your savings are likely to lose value over time.

Personal pension, stakeholder pension or self-invested personal pension (SIPP)?

We’ve covered what each personal pension has in common, so here’s a closer look at the differences and why one might suit more than another.

| Personal pensions for the self-employed | \n|||

|---|---|---|---|

| Types of personal pension | \nSIPP (self-invested personal pension) | \nOrdinary personal pension | \nStakeholder pension | \n

| How does it work? | \n\n SIPPs tend to offer a wider choice of investment options. \n You decide what your pension is invested in. \n You can build your own portfolio of stocks or other assets. But you can also select ready-made investment options too, like ETFs and investment trusts.\n | \n \n Personal pension plans tend to have set investment options that you choose from. \n Each ready-made portfolio is designed with a specific investment goal. \n For instance, this could be a portfolio of sustainability-focused investments, or one tailored to a specific retirement date.\n | \n \n Stakeholder pension plans work similarly to personal pensions but must meet certain government criteria. \n These include cost limits and a minimum contribution level. \n You or a financial advisor choose your portfolio, but a fund manager manages the underlying investments.\n | \n

| Who makes the investment decisions? | \nYou or your financial advisor decide what your pension is invested in. | \nYou choose the portfolio, but a fund manager decides what goes in it. | \nYou choose the portfolio, but a fund manager decides what goes in it. | \n

| Who might suit this one? | \n\n You’d like to choose your own investments. \n You’d like to keep costs low and know exactly what you’re paying for. \n You’d like the option to combine old pensions.\n | \n \n You don’t want to choose your investments. \n You’re not worried by a lack of investment choice. \n You’re not too worried about the price. \n You’d like the option to combine old pensions.\n | \n \n You don’t want to choose your own investments. \n You’re really not worried by lack of investment choice. \n Keeping costs low is a priority.\n | \n

SIPP pension with Freetrade

With Freetrade, you can open and invest in a SIPP pension as part of any Freetrade plan, including the Basic plan, giving you control over how you save for retirement.

- You decide how much to invest and when

- You choose how your retirement savings are invested. Choose from over 6,000 UK, US and European stocks to invest in, ETFs and more.

- You can transfer and combine old pensions in a one SIPP account.

Find out more in our what is a SIPP guide.

State pension for self-employed

The headline news is that the State Pension is for everyone. Employed, self-employed or unemployed.

You can get the State Pension so long as you have reached State Pension Age (which is currently 66 but that’s set to rise to 67 by 2028 and to 68 by 2039) and you meet the necessary criteria.

For anyone reaching State Pension age after 6 April 2016, it’s all based on your National Insurance record.

To get any State Pension you’ll need at least 10 qualifying years on your National Insurance record and to get the full State Pension you’ll need 35 years.

What is a ‘qualifying year’?

Generally, a qualifying year for the State Pension can be made up through National Insurance contributions made while working (employed or self-employed), National Insurance credits or any voluntary National Insurance contributions.

For the full ins and outs on National Insurance contributions and qualifying years, it’s best to check with the government directly.

How much state pension can you get when you’re self-employed?

There’s no such thing as an employed or self-employed state pension. The State Pension is the same for everyone.

The only difference in how much State Pension anyone gets is whether you’ve got enough years of National Insurance contributions under your belt.

At the moment if you qualify for the full new state pension, you’ll get £179.60/week. But this will change over time.

An important thing to know about the State Pension is that it changes over time, both in terms of the value of benefits and the age at which you can access these.

Given this, it’s best to check your State Pension age and forecasted State Pension directly on the government’s site.

Workplace pensions

It’s not impossible for someone self-employed to also have workplace pensions.

If you’ve been employed by someone else in the past, it’s likely they’ll have set up a pension for you.

It’s important to keep a close eye on any old pension pots. What looks like a small sum, once invested into the stock market could grow into something crucial to your retirement.

If you aren’t quite sure where to find old pensions, take a look at our guide on finding old pensions.

Once you’ve found old pensions you can either keep them where they are (which can be a good idea if they come with benefits like guaranteed income) or you can transfer and combine them into one account.

SIPPs can be a useful account for this. They give you the flexibility to transfer pensions and keep old pensions under one roof.

How to start a pension if you’re self-employed

Starting a pension if you’re self-employed shouldn't be scary.

Here are a few steps we suggest thinking about:

1. Double-check if a pension is the right account

Pensions are there to help you save and invest for retirement. In a personal pension, you can’t access your money until you are at least 55 years old, so double-check this works for you.

2. Choose your pension provider

Take a look at our tips below on how to choose the best pension provider for your needs.

Think about what you’d like from a pension provider and then understand how they charge you.

Keep a lookout for any percentage account fees. If your pension pot grows your account fees will too and this will impact your pension’s growth.

Learn more about opening a SIPP account with Freetrade.

3. Contribute to your pension

Habits are key, start early and invest as regularly as you can.

The earlier you start, the sooner your contribution is boosted by tax relief and the more time you are giving your pension pot to grow.

4. Invest your pension

Depending on which type of personal pension you have chosen, your options will be slightly different.

A SIPP gives you the flexibility to choose your own investments. With an ordinary personal or stakeholder pension, you’ll likely have a limited number of investment options to choose from.

With Freetrade you can invest in a wide range of things with thousands of US, UK and European stocks to invest in, ETFs and investment trusts. You can even buy part of a share which could help you build a diversified portfolio.

5. Combine old pensions under one roof

If you haven’t always been self-employed, you could have old workplace pensions from previous roles.

It’s worth considering whether bringing old pensions under one roof would be beneficial.

6. Check in on your pension

Check in every year to see how your pension is performing and whether you are on track to reach your retirement goals.

How to choose the best pension provider for self-employed pensions

When it comes to choosing the best pension provider for your needs it’s best to think in terms of two things: features and fees.

For features here are some questions to think about:

- How experienced an investor are you?

- Do you want to choose your own investments?

- What do you want to invest your pension in?

- Would you prefer an app, web-based product or both?

- Would you like any other accounts e.g. ISA in the same place?

- Would you like educational content to help you make investment decisions?

When it comes to fees make sure you’re clear on how the platform charges you.

Here are the fees to understand:

- Account charges - how much does a pension account cost and is it a flat fee or a percentage fee that could grow as your investment does?

- Trading commission - how much it costs to place a trade

- Foreign exchange fees - how much you are charged to buy overseas investments

- Ongoing charges - for pension investments like ETFs, investment trusts and funds

- Exit charges - some providers charge you for leaving them

- Drawdown fees - how much it costs to start taking money out of your pension

Take a look at our investment fees calculator which compares SIPP provider charges.

How much should I contribute to my pension?

This is where pensions start to get personal.

How much really depends on a few different factors in your life but here are a few of the main ones.

- How much do you think you’ll need in retirement?

- How much can you put in a pension and still get the tax benefits?

- How much can you afford to put into a pension now?

How much will you need in retirement?

A good place to start when thinking about ‘how much to save’ is to work backwards from how much you might need.

This isn’t an exact science, if retirement is still a lifetime away it’s going to be an estimate.

So think roughly, how many years away is it? What level of income would you like to have then? Will you retire fully or still keep working?

Our guide on pension planning and how much you need to retire walks you through these steps.

How much can you put in a pension?

One of the main benefits of saving into a pension is tax relief.

For most of us, each time we pay into a pension, the government adds money too and it does this via tax relief.

It’s an incentive to get us all to save more for the future. And while it’s generous it’s not unlimited.

The UK government sets annual limits on how much we can each contribute to a pension and get tax relief.

This is known as the annual allowance. And for most savers in the UK, it’s the lower of 100% of your earnings or £40,000.

For example, if your earnings are £38,000 in a year, you can contribute up to £38,000 into a pension that year. This includes any tax relief too, so the amount that actually comes from your pocket will be less.

How much tax relief you’ll get ultimately depends on the rate of income tax you pay. But as a starting point, everyone gets 20% or basic rate tax relief.

With a personal pension, this 20% or basic rate tax relief is added directly to your SIPP account when you contribute.

So if you add £80 to your personal pension, the pension provider collects £20 (i.e 20% or basic rate tax relief) from the government and adds it directly into your account, making your total pension contribution £100.

This is useful because you can invest the bigger pension amount straight away.

The examples we’ve used here won’t work for everyone, as allowances and tax relief will change depending on different circumstances like income levels and whether you’ve started taking your pension already.

Check out our pension tax relief guide for the full ins, outs and examples.

How much can you afford to put into a pension now?

Again this is personal and if you are self-employed, not always a straightforward answer.

Some months you might be able to afford more, others less and in some months maybe none.

That’s ok though, pensions (like any investing) benefit from doing it regularly and while monthly is often suggested (to fall in line with other payments and bills), a few lump sum contributions a year or annually could work too.

Pension savings should fall somewhere after essentials (like housing, food and heating) and before or alongside the nice-to-haves (like new clothes, shoes and holidays).

Check out how our guide on how much money to invest in stocks

Just start it

If only Nike did pensions…

The most important decision when it comes to your pension is the day you decide to start one.

The earlier you start making contributions to your pension, the better.

It gives more time to build up a bigger pension pot, to benefit from tax relief and for your savings to grow.

The later you leave it, the more it’s going to cost.

Here’s an example.

.jpeg)

Each month you save £250 into a pension which means you’ll get £62.50 (20% basic rate tax relief) added automatically to your pension too.

So a £312.50 monthly pension contribution in total.

We’ve assumed your pension pot is invested and grows each year by 5%. In reality, some years it might be more and others less.

You can see clearly from the chart below, the later you start contributing to a pension the less growth you’ll see and the bigger the gap you’ll have to fill.

And this is even before considering any increases in the amount you contribute.

Take a look at our pension investment strategies, whether you’re in your 20s and 30s or 40s and 50s.

How best to save for retirement

There are a few ways to save for retirement.

Pensions are a great option because of the tax benefits but a pension is likely to be part of a wider strategy.

Here are a few of the most common ways to save and invest for retirement.

Personal pension

Putting money into a pension is a hard one to ignore.

The tax benefits are generous and it’s something you can add to over your working life, there is no big one-off cost.

- Tax relief - as we mentioned earlier, the government will top up any pension contributions you make. Boosting your pension savings.

- Savings grow tax-free - inside a pension, your investments have the chance to grow free from UK tax.

- Take 25% tax-free - you can access your pension from age 55 (rising to 57 in 2028). When you do, you can take 25% of your pot tax-free. The rest will be subject to income tax though.

Pay profits into a pension

If your business is a limited company you can pay profits into a pension as employer contributions.

Paying into a pension (as an employer) is classed as a business expense, so you could reduce the corporate tax you owe.

And any profits paid to your pension will no longer be paid to you as a salary, so should reduce your personal income tax too.

Stocks and shares ISA or SIPP?

This is a common conundrum. And the answer could be both.

ISAs, like pensions, are tax-efficient investment accounts. Inside both accounts, your investments have the chance to grow free from UK taxes.

However, beyond this headline, there are a few key differences between them:

- You can put £20,000 into an ISA each year but with a pension ‘how much’ depends on a few things (the key one being your annual allowance, as we mentioned above) There’s no tax relief added to an ISA but there is with a pension

- You can take money out of an ISA at any point but you can only access your pension at 55 (rising to 57 in 2028)

- When you take money out of an ISA there’s no capital gains tax to pay but there could be tax with a pension

Check out our SIPP vs ISA guide for a full breakdown.

Property as a pension

Without a workplace pension to rely on, self-employed workers are particularly keen on property when it comes to saving for retirement.

According to the ONS Wealth and Assets Survey, 42% of self-employed workers see property as the safest way to invest for retirement (5).

Whether it’s the best answer for retirement savings is something to consider though.

There is still risk involved in owning property, particularly investment properties. There’s no guarantee that house prices will rise, there’s always a risk someone might not rent it and there’s maintenance costs and tasks that can increase the burden. Property is a lot more illiquid too, you can’t sell part of it as soon as you need cash.

There are still taxes. Income from rental properties will be subject to income tax and when you come to sell, capital gains tax is higher on residential property.

There may be alternatives to owning the property yourself. Real estate investment trusts (REITs) offer a way to invest in all different types of real estate, commercial, residential and even industrial property.

.webp)

.webp)

.avif)