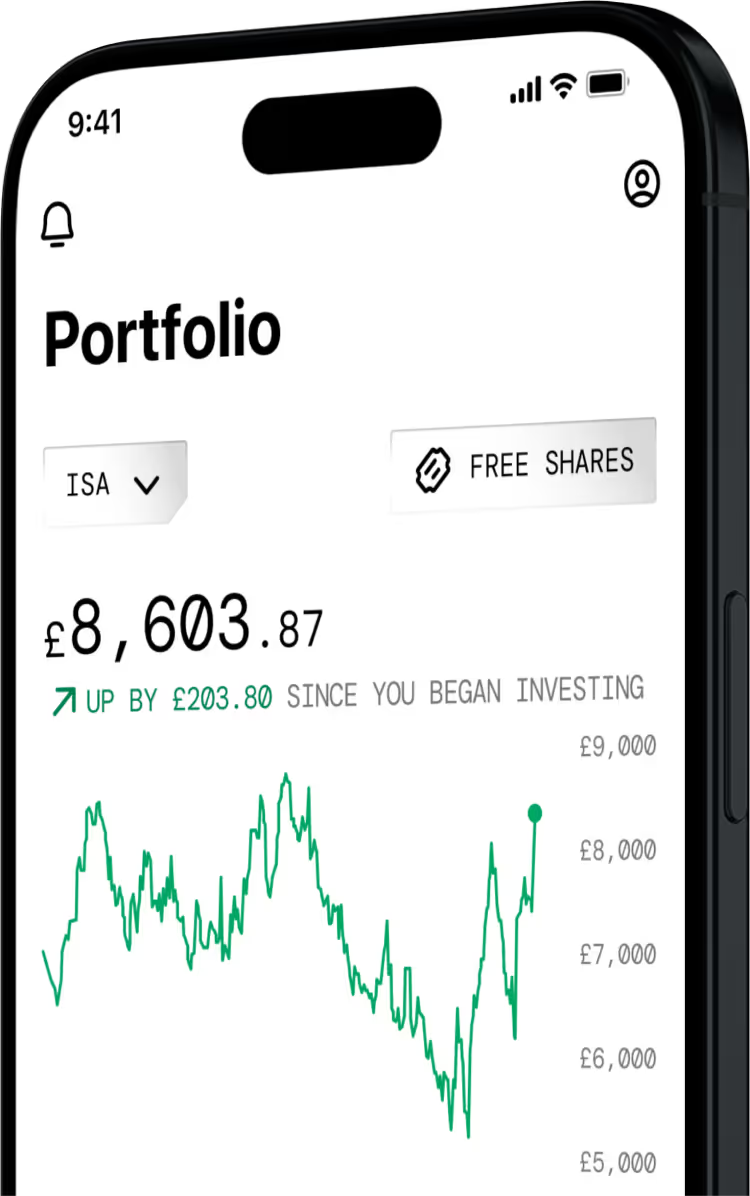

Self-invested personal pension (SIPP)

PERSONAL PENSION

Take control of your retirement pots with a self-invested personal pension (SIPP). Now available on all plans.

Capital at risk.

The value of your investments can go down as well as up and you may get back less than you invest. SIPP eligibility rules apply. Tax treatment depends on your personal circumstances and current rules may change.

Ready to take control over your scattered pension pots? Contribute £10,000 to a Freetrade SIPP to get up to £5,000 cashback.

Offer ends 5 April 2026.

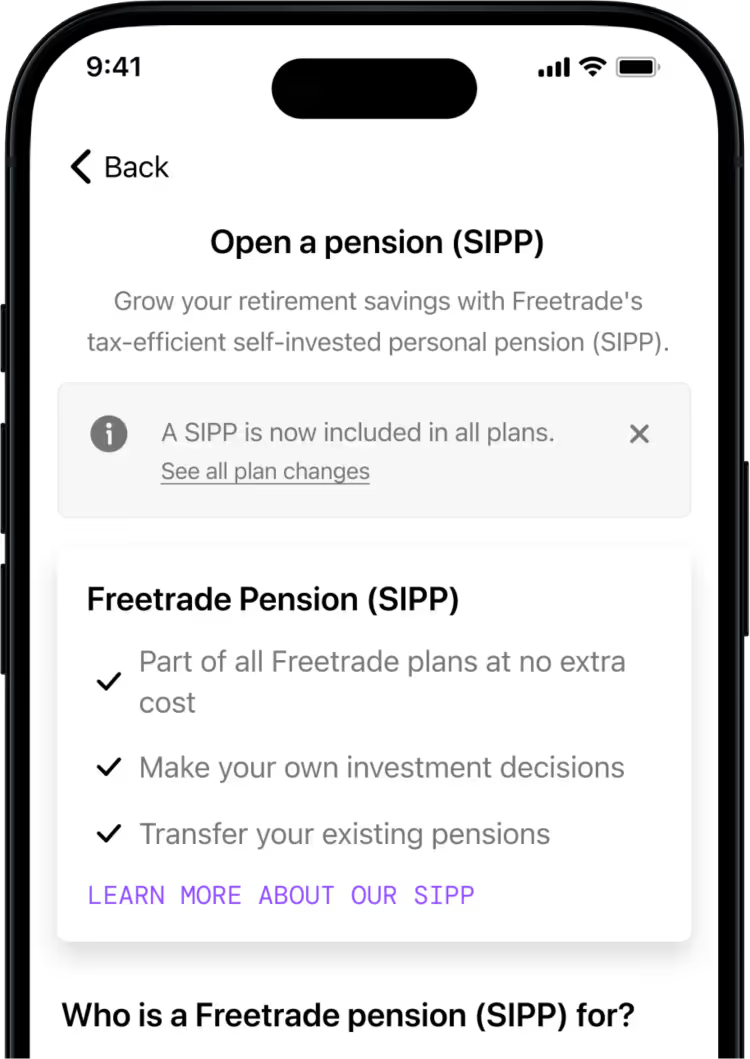

A SIPP is a pension designed for you to save until your retirement and is for people who want to make their own investment decisions. You can normally only draw your pension from age 55 (57 from 2028), except in special circumstances.

At present, Freetrade only supports Uncrystallised Fund Pension Lump Sums (UFPLS) for customers who wish to withdraw funds from their SIPP after their 55th birthday. We strongly encourage you to seek financial advice before making any withdrawals from your SIPP.

Pensions that are transferred to the Freetrade SIPP may lose the protected pension age benefit. This means that you will not be able to draw the monies from the Freetrade SIPP until you are aged 57. Please ensure you know what this means for you and the effect it may have on you and your savings. Check before you transfer a pension to us that we can accept your investments, you won’t lose any guarantees, and that you know what charges you may incur. Seek advice if you are unsure about making a transfer.

For your pension contributions, we'll claim the 'Basic Rate' tax relief from HMRC on your behalf and deposit it in your Freetrade SIPP account automatically.

It normally takes around 6-11 weeks from the contribution to the tax relief appearing in your account. The HMRC tax relief depends on your eligibility. You can read more about tax relief.

Check before you transfer a pension to us that we can accept your investments, you won’t lose any guarantees, and that you know what charges you may incur. Seek advice if you are unsure about making a transfer. Always do your own research.

Pensions that are transferred to the Freetrade SIPP may lose the protected pension age benefit, if applicable to you, meaning that you will need to wait longer until you can draw monies from your Freetrade SIPP. Please ensure you know what this means for you and the effect it may have on you and your savings.

Freetrade won't charge you to transfer your pension to us, but please check with your existing provider what fees or restrictions may apply from them. We cannot provide you with any advice therefore it is your responsibility to ensure you are happy that transferring to the Freetrade Pension is right for you.If you're unsure if transferring your pension to Freetrade is right, you should take advice from a suitably qualified financial adviser. For more info, see our SIPP Key Features Document, Terms and Conditions, SIPP Charges and SIPP Declarations.

A SIPP is a Self-Invested Personal Pension. It's a pension pot you build yourself to live off in retirement. Unlike other types of personal pension, a SIPP gives you much more flexibility when it comes to what you can invest in.

You can transfer the below types of pensions to a Freetrade SIPP:

*Subject to current plan rules. Some workplace pension plans cannot be transferred whilst still active.

Currently, we are unable to accept Final Salary Personal Pension, Defined Benefit Pension Plan or any pensions that contain Safeguarded Benefits including Protected Tax-Free Cash (PTFC), Protected Retirement Ages (PRA), Guaranteed Annuity Rates (GARs) or Guaranteed Minimum Pensions (GMP).

There is no limit on how many pensions someone can have (e.g. NHS pension and a Freetrade SIPP), but clients should be aware of their own circumstances.

Your SIPP gives you access to everything Freetrade has to offer. Invest in the full range of 7,000+ global stocks, funds, ETFs, trusts, bonds, UK Treasury bills, and more, and use limit orders and stop losses to stay in control of your trading.

Yes. You can transfer other personal pensions to the Freetrade SIPP. Transfers from defined benefit pension schemes and schemes that provide safeguarded benefits are not accepted.

Before transferring your pension to Freetrade, make sure it is the right action for you to take. Please ensure that you will not lose valuable guarantees or incur excessive transfer penalties.

Contribute up to £60,000 per year, or 100% of your annual income, into your pensions.

No, transfers don’t use up your annual allowance. You should be aware, though, that some providers may charge exit fees or other surcharges in order to transfer.

No, currently we don't accept employer contributions, but we hope to in the future.

We claim the 'Basic Rate' tax relief on your behalf and deposit it in your Freetrade SIPP account automatically. It normally takes around 6-11 weeks from the top-up to the money entering your account.

If you have made contributions to your SIPP

Once you have funded your SIPP, you can only cancel or close it within the first 30 days of opening it. After this point your SIPP cannot be closed and the pot of money you’ve built up will be preserved until you reach the age at which you’re allowed to access your pension (currently 55, rising to 57 in 2028).

To close your SIPP within the first 30 days of opening it, contact our Customer Service team. When you cancel within the first 30 days, we will refund any account fees taken.

After the 30 days, if you have made contributions to your SIPP, you won’t be able to close it, but you can transfer it to another pension if you wish. This is because SIPPs are a bit different to other investment accounts and operate under slightly different rules.

If you have not made contributions to your SIPP

If your SIPP is empty, you can close your SIPP at any time. Simply contact our Customer Service team and they can organise this for you.

For more information take a look at SIPP key features.

A SIPP, or Self-Invested Personal Pension, is a type of personal pension. They are both pension pots that you build yourself.

A SIPP tends to offer you a wider choice of investment options and greater control over what they invest in. Other types of personal pensions, such as personal and stakeholder pensions, tend to have restricted invested options.

For more details on how pensions work in the UK, check our guide on what pensions are.

You normally need to be at least age 55 (rising to 57 in 2028) to access money in a pension fund.

If you want to take money from your Freetrade SIPP, please contact our Customer Service team and they will send you a Retirement Options Pack.

At present, Freetrade only offers “uncrystallised funds pension lump sums” (UFPLS) payments, but there are other options available that you can consider when deciding how to access your pension fund.

We have to tell you about your options before we can start processing your request as it’s important that you consider which option is right for your personal circumstances. The Retirement Options Pack will help you understand your options, but if you’re not sure, please take advice from a suitably qualified financial adviser.

If you then decide to access funds from your pension plan using UFPLS, you can ask us to send you an application form and risk warning questionnaire.

An “uncrystallised funds pension lump sum”(UFPLS) or lump sum payment is one way of withdrawing money from a pension.

You take cash from your pension fund as and when you need it and leave the rest invested, where it can continue to grow tax-free.

Normally the first 25% of each UFPLS payment is tax-free and the rest is taxed as income.

If you take money from your pension fund using UFPLS, the amount you can pay into your pensions and get tax relief on in the future is restricted. If you want to carry on saving into a pension, this option may not be suitable.

Before you withdraw money from your pension fund using UFPLS, you should think about whether it’s right for your personal circumstances, including the tax impact of taking UFPLS payments. If you’re not sure, please take advice from a suitably qualified financial adviser.

Yes.

You can use both drawdown and UFPLS to take benefits from just some of your pension fund or from all of your pension at once.

With UFPLS you take money out of your pension as a lump sum payment 25% of which is normally tax free and 75% taxable. With drawdown you can normally take up to a quarter (25%) of the money in your pension fund as a tax-free lump sum. The rest is moved to a drawdown pension fund, where it is available to provide taxed income. You can start taking your income straight away or wait until a later date and take your income at times to suit you.

If you take money from your pension fund using UFPLS, the amount you can pay into your pensions and get tax relief on in the future is restricted. With drawdown the same restrictions apply, but only once you have taken taxable income (not the tax-free cash) from your pension.

Please note, currently there is no option to take benefits as drawdown from your Freetrade SIPP and you would need to transfer some or all of your pension fund to another pension plan in order to take your pension benefits using drawdown.

If you want to take a lump sum from a pension that you haven’t accessed previously, you can contact our Customer Service team who will send you an application form. Please note you normally need to be at least age 55 to request this (or 57 from 2028).

Before you take UFPLS, you should consider whether it’s right for your personal circumstances. If you’re not sure, please consult an independent financial adviser first. By withdrawing money in this way, you may limit valuable tax benefits from your pension in the future.

At present, Freetrade only offers uncrystallised funds pension lump sums (UFPLS), but other options are available to consider when deciding how to access your pension funds.

Currently you will have to transfer your Freetrade pension fund to another provider if you want to take money from your pension as an income, known as a drawdown, or to convert it to an annuity.

Before you withdraw money from your pension fund using UFPLS, you should think about whether it’s right for your personal circumstances, including the tax impact of taking UFPLS payments. If you’re not sure, please take advice from a suitably qualified financial adviser.

Each UFPLS withdrawal from your Freetrade SIPP will cost £240.

When you invest, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you invest.

General investment account

Stocks and shares ISA

Pension (SIPP)

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.99% on non-GBP trades

1% AER on up to £1k uninvested cash

Mutual funds and gilts

General investment account

Stocks and shares ISA

Pension (SIPP)

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.59% on non-GBP trades

2.5% AER on up to £2k uninvested cash

Mutual funds and gilts

General investment account

Stocks and shares ISA

Pension (SIPP)

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.39% on non-GBP trades

3.5% AER on up to £3k uninvested cash

Mutual funds and gilts

General investment account

Stocks and shares ISA

Pension (SIPP)

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.99% on non-GBP trades

1% AER on up to £1k uninvested cash

Mutual funds and gilts

General investment account

Stocks and shares ISA

Pension (SIPP)

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.59% on non-GBP trades

2.5% AER on up to £2k uninvested cash

Mutual funds and gilts

General investment account

Stocks and shares ISA

Pension (SIPP)

Commission-free investing in Freetrade’s full universe of stocks, ETFs, and investment trusts

FX fee of 0.39% on non-GBP trades

3.5% AER on up to £3k uninvested cash

Mutual funds and gilts