“All I did,” wrote Bernie Madoff in 2011, “was make rich people richer and some rich people poorer.”

It’s not exactly what you’d expect someone to say if you asked them how they carried out the biggest Ponzi scheme in history, even if there is an element of truth to it.

Madoff seems like someone that often defied expectations though. When his fraud came to light in late 2008 it shocked much of the financial world.

That may appear odd now given his name has become synonymous with ‘fraudster’. But to understand why people were so surprised you need to dig a little deeper into the now-disgraced financier’s background.

From pink sheets to Wall Street

Madoff entered the financial world in the early 1960s. He started out by founding his own company, Bernard L. Madoff Investment Securities (BLMIS), which was a market maker in ‘pink sheet’ stocks.

For those not in the know, a market maker is someone in the business of buying and selling stocks.

Much like a foreign exchange bureau on your local high street, they make money by buying low and selling high. The gap between those two prices, known as the spread, is where they make their money.

Pink sheet stocks are usually smaller, riskier companies that don’t trade on an exchange. Instead you buy them, in what’s known as an ‘over the counter’ (OTC) transaction, directly from a market maker.

Movie buffs may have noticed that this is exactly the sort of business that Jordan Belfort, more infamously known as ‘the Wolf of Wall Street’, was involved with.

Bernie Madoff — tech innovator

To be fair, Madoff doesn’t appear to have behaved so unscrupulously during his time in the lurid world of penny stocks. In fact, he ended up running a well-respected market making business.

Probably realising there wasn’t much money to be made in pink sheets, he moved into dealing in exchanged-traded stocks. Today that would include S&P 500 firms, like Facebook or Coca Cola.

Doing so required a couple of novel innovations. The first was developing computer software to match orders and both gather and distribute pricing, something of a novel idea at the time.

BLIMS’ technology was also so good that it ended up being used in the creation of the Nasdaq in 1971.

Inventing payment for order flow

Alongside this, Madoff was supposed to be the first person to have developed payment for order flow (PFOF). This practice, which remains controversial today and is illegal in the UK, involves a market maker paying a broker for giving it orders.

If that sounds odd then imagine you want to exchange some money at a bureau de change. The problem is there are lots of bureaus and you don’t know which one to go to.

Some happy intermediary guides you to one particular bureau and convinces you to use them. The bureau makes money on the spread and then gives part of those earnings to the intermediary that took you there.

PFOF works in a similar way. You submit your order to a broker. The broker then funnels that order on to a market maker. For providing them with the opportunity to make money off of the spread, the broker receives a kick back.

This neat innovation, along with the firm’s tech prowess, made BLMIS one of the biggest market makers in the US.

A 2008 article notes that it was, at one point, the largest market maker on the Nasdaq and the sixth-largest for all S&P 500 stocks. Another from 1992 notes gleefully that daily volumes at the firm equalled 9% of those on the New York Stock Exchange.

All the accolades

Along with a very successful business, Madoff was also active in several senior roles across the financial services industry.

He had stints as chairman of the Nasdaq, the National Association of Securities Dealers (a regulatory body), and the Securities Industry and Financial Markets Association.

All of this probably explains why people were so convinced by him. Not only had he founded a major market maker, he also seemed to have the seal of approval from respectable industry organisations.

But what did he actually convince them to do?

How Madoff’s Ponzi worked

The short answer is that he got them to part with lots of cash so he could invest it. He then claimed he was making abnormally good returns for them, which in turn encouraged more people to give him money.

Quite when he started doing this isn’t entirely clear. One ex-employee said it may have been as far back as the 1970s, although Madoff himself later said it was in the early 1990s.

The 1992 report would contradict those claims as it describes his investment activity going back to the early 1980s.

In the same article, Madoff said he had been using an arbitrage strategy on bonds and stocks throughout the 1980s. He’d then moved on to tracking an index and delivering outsized returns by using options.

None of this was actually true. The firm just took money in, did nothing with it, and issued fake statements to clients showing how much their ‘investments’ had gone up in value.

If anyone asked for their money back, Madoff’s company would simply use other people’s deposits to fund the request. As some readers will probably realise, this is pretty much the dictionary definition of ‘Ponzi scheme’.

Making it last

The thing is, these schemes usually don’t last very long. They promise too much and soon attract so much attention that they can’t keep the lie going.

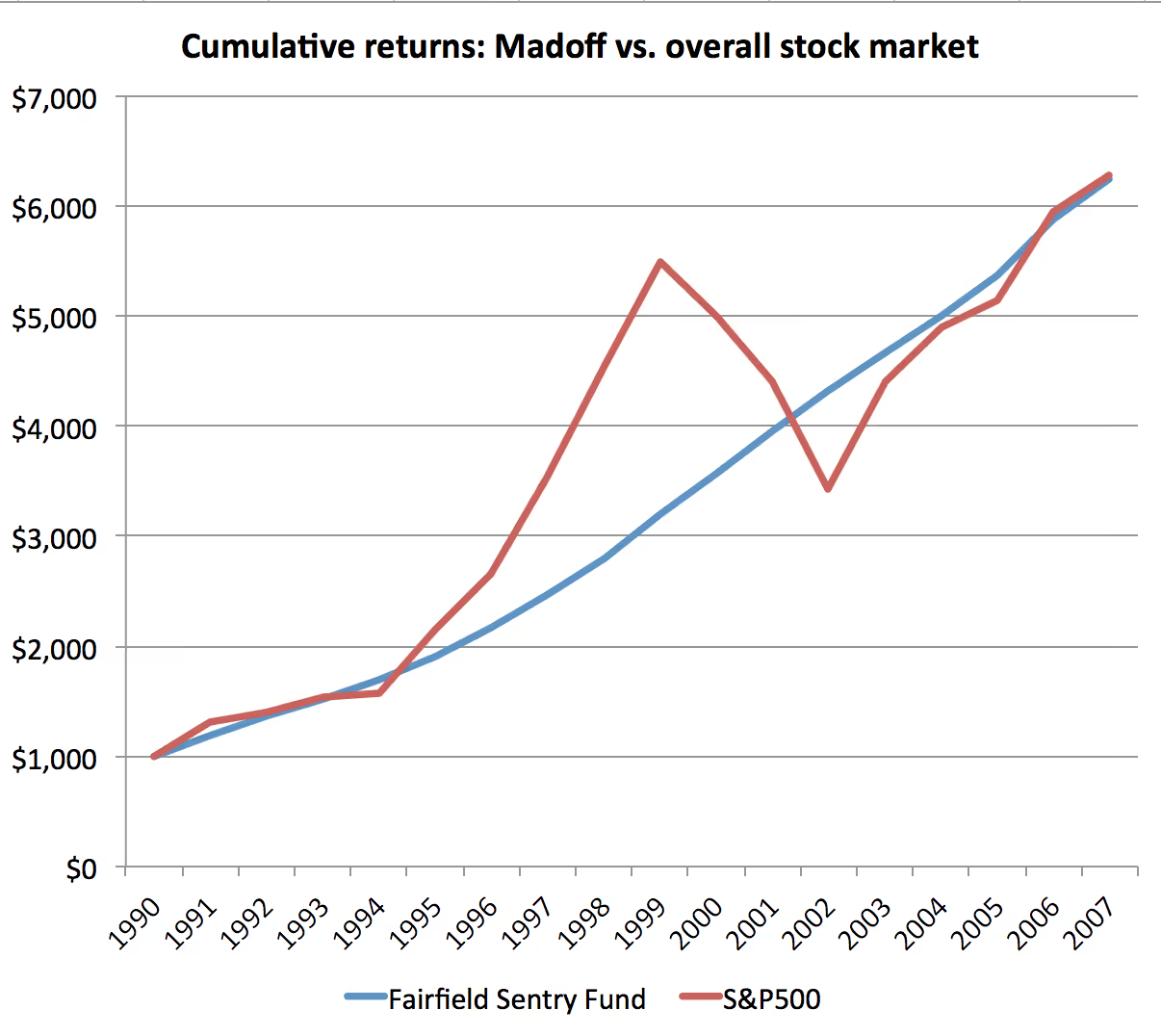

Madoff did things differently. Although he delivered eye-catching returns, it was usually ‘only’ 13% to 20% per year. This was not the ‘make 1,000% returns in five days’ sort of thing that you see spewed across your spam box today.

He also asked people not to tell anyone about the fund and didn’t publicly reveal he was doing it. The 1992 article seems to be the first time it became widely known he was managing money.

Still, as it grew in size, question marks did start to emerge about how he could possibly achieve the returns he claimed he was achieving. The 1992 piece was also on the back of an investigation from the Securities and Exchange Commission into his fund. Amazingly they found nothing wrong.

A similar story emerged about a decade later. Harry Markopolos, an analyst and forensic accountant, was asked by his firm to try and create a strategy similar to the one Madoff said he was using.

Markopolos later said it took him five minutes to see that Madoff’s fund was fraudulent. One of the more amusing facts he uncovered was that for the ‘strategy’ to be working, BLMIS would have to be trading more options on the Chicago Board Options Exchange than existed.

Front running or scamming?

Markopolos’ work sparked another couple of critical articles. But the belief at the time seems to have been more that Madoff was front-running his orders, rather than being a Ponzi scheme.

This is where a broker identifies a large batch of trades in a particular asset. They then execute their own orders, before those other trades are placed, so they can take advantage of any market movements the latter cause.

As BMLIS ran a huge market making business, they’d have been privy to information that would probably have allowed them to do this.

The problem with this theory was it would be logistically hard to do. Excess money would have to be funnelled from the market making division to the hedge fund, something which clients of the former business would probably cotton on to.

The other reason to doubt it was the fact that Madoff’s trades didn’t appear to be showing up at all. Given the size of the funds he was supposedly managing, any buys he made would likely move the market — front running or not. But that wasn’t happening.

Crashing down

Despite various investigations and reports, it was ultimately the 2008 financial crisis which brought Madoff down.

With people panicking and markets sloping downwards, more and more investors were asking for their money back.

According to 2013 court documents, Madoff’s firm claimed to have $65bn in assets under management just prior to the fraud being exposed. In reality it only had $200m.

With more and more people asking for money that didn’t exist, and Madoff unable to pay it, he had to confess.

The collapse saw Madoff sentenced to 150 years in prison, where he died in April of this year aged 82. His brother Peter, who worked as the firm’s compliance officer, was also sentenced to 10 years.

Not just the rich

The fallout from the Ponzi scheme is still going on today, with a huge number of lawsuits filed in an effort to claw back the lost money.

The amount sought has totalled around $20bn. If that number seems small then remember much of the $65bn was fictitious — it only existed because of the ‘amazing’ gains the fund said it was making.

The main problem has been that some investors who took money out of the scheme before its collapse actually made sizeable profits.

Many of these people have since been forced to return them. The widow of one close associate of Madoff’s, Jeffry Picower, had to pay back $7.2bn after her husband’s death in 2009.

Although it does seem many of his ‘clients’ were very wealthy individuals, Madoff also had fund managers feeding him money. And those funds were usually made up of lots of smaller investments by regular people.

One teacher, for example, ended up having to work an additional ten years because of the money he’d lost in the fraud. So even though Madoff was probably partially correct in saying he’d just made some rich people richer, and others poorer, it certainly wasn’t true across the board.

The big why

Along with trying to recover their money, one of the things people have been trying to figure out is why Madoff actually carried out his scheme.

Most Ponzis or frauds are carried out by people that want to get rich. But Madoff was already very wealthy. In fact, this was another reason people doubted he’d be running a scam — he had no financial need to do so.

By one account, his market making business was worth $3bn and he appears to have been the sole owner of the business, meaning any sale of it would’ve made him very rich.

People’s minds and motives are often impenetrable. If you think about something dumb you’ve done before, you may even be at a loss to explain to yourself exactly why you did it.

But we do have a couple of clues that may provide some answer as to why Madoff behaved the way he did.

The first is from 1962. Very early on in his career, Madoff pooled some money together from a group of friends and family to invest in an IPO. The listing was a dud and he lost a lot of the money.

Rather than telling the people he took cash from, he borrowed $30,000 (about $260,600 in 2021 terms) from his father-in-law and paid them back. Apparently he couldn’t bear to tell anyone he’d lost their money.

The 2013 court documents also note that Madoff’s London operation, which was legitimate, wasn’t making any money. Apparently this didn’t bother him though.

“It was for him a matter of pride and prestige to have a presence in London,” wrote the judge, “and whilst he did not want to make losses, this was a secondary consideration to having a presence which would enhance his reputation.”

No one is immune from lying

What that suggests is, either for reasons of pride or not wanting to hurt people’s feelings, or perhaps some combination of the two, Madoff couldn’t deal with the idea of losing people money.

It also seems plausible that what started as a small lie mushroomed into something totally unsustainable. By the 1990s at least, it seems very likely that Madoff had taken in so much cash that his only option would be to come clean or keep the scam going.

Of course it may have been something altogether different. The odds are we’ll never know the whole truth.

What the whole affair does reveal is that if something is too good to be true, it almost certainly is, and no company or individual should be seen as so respectable that they can’t lie.

For us as investors that means not being seduced by promises of ridiculous returns or highfalutin language describing some novel technology or groundbreaking investment strategy. Taking five minutes, as Markopolos did, to examine something properly isn’t just a sensible thing to do, it could end up saving you a lot of money and stress.

Past performance is not a reliable indicator of future returns. Source: FE, as at 16th Sept 2021. Basis: bid-bid in local currency terms with income reinvested.

Thoughts on Madoff's Ponzi scheme? Share them on the community forum:

Make your investments work a little bit harder with one of the UK’s leading commission-free trading apps. Freetrade has transparent charges, no hidden fees and is one of the only brokers to offer fractional shares in the UK. Download our iOS trading app or if you’re an Android user, download our Android trading app to get started investing.

This should not be read as personal investment advice and individual investors should make their own decisions or seek independent advice. This article has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is considered a marketing communication.When you invest, your capital is at risk. The value of your portfolio can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future results.Freetrade is a trading name of Freetrade Limited, which is a member firm of the London Stock Exchange and is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales (no. 09797821).

.jpg)

.avif)