“It’s tough to make predictions, especially about the future.”

Yogi Berra said it best but it doesn’t stop investors from dusting off the crystal ball at this time of year.

Instead of channelling our inner fortune tellers though, we think our time is better spent looking at a few themes from 2022, some ways the narrative could change and, most importantly, what that could mean for your investments.

That means looking at the storylines already playing out as well as the changes to the ISA world waiting for us in 2023.

Read more:

- The (more realistic) ISA millionaire

- Cash ISA vs stocks and shares ISA

- The Freetrade stocks and shares ISA

The big picture doesn’t always translate into a simple investment thesis though. Just look at the market’s slingshot after the onset of the pandemic. Who saw that coming?

But getting an idea of how the path for interest rates, inflation and the war in Ukraine could affect market optimism should help us prepare our portfolios as much as we can.

No doubt there will be a whole host of market influences and ‘unknown unknowns’ popping up in 2023. So, we’ve stuck to the four things we’re already seeing. Here’s what we’ll be keeping an eye on.

1. The UK/US rotation

Dan Lane, senior analyst & manager of investment writing

It’s been a topsy-turvy few years for UK and US stocks. US tech had its time in the sun over the pandemic but started to give way to the written-off UK large caps towards the end of 2021.

A higher rate environment has taken the shine off the American lockdown leaders now and the UK market enters the new year ahead of its transatlantic pal.

What’s this got to do with 2023 though? Well, it’s about which sectors investors are likely to run from and to, given the inflation picture.

A nod from the Fed that rate rises will stall or even potentially reverse would likely trigger a flight back to US tech. In the meantime, it’s the stocks with high quality, strong balance sheets, stable margins and low debt that will attract capital, as well as ones that stand to benefit from higher inflation.

That could mean investors stick with UK names in large dominant consumer sectors, as well as banks with widening net interest margins and miners benefiting from high commodity prices.

The relief rally in November, as US inflation came in lower than expected, is a sign investors are begging for permission to be positive and pounce on falling valuations, which could start to look too tempting to ignore, even in tech. But despite their fall so far, it’s the threat of a hard slog through a higher rate environment in 2023 that’s keeping investors on the sidelines.

The market will want solid earnings with proof that margins aren’t falling victim to inflation as well as a slowing rate trajectory before any fleeting bounce can turn into a sustained recovery. JP Morgan is predicting US earnings to fall by 10-20%, so we’ll have to see if the market rewards the ‘least worst’ balance sheets or if there’s still appetite to punish missed forecasts.

Gemma Boothroyd, analyst & investment writer

The US tech sector was this year’s biggest casualty. But for investors keen to take advantage of a potential resurrection, price corrections could be just the opportunity to get in at a discount.

Of course, cheap doesn’t mean good value. And what needs to be front of mind for investors are the companies actually demonstrating quality rather than just promising it. The ‘growth-at-all-costs’ model won’t keep investors happy in the coming months. It’ll no longer be enough to just have a profitability plan in the far-off future. All eyes will be on the firms that have proven they can generate cash and grow it too.

Meta is evidence of what can happen if they don’t. Going from an ad-pumping machine to a metaverse flop took Zuck’s stock down to levels not seen in over five years.

Though, Meta is still cash-generative and profitable too. It’s just that it’s shown a few quarters of those two vital metrics flipping into reverse.

It’s simply a case of risky bets (ahem - Oculus goggles, anyone?) not paying off. And Meta isn’t alone in that. Shopify and Square are two other behemoths to admit they have overshot forecasts and growth expectations.

The point here though is that if tech leaders like Meta can get back to the basics, and get a bit leaner in the process, then they might actually be at a much fairer valuation now.

If investors hop on that, then it’s the tech companies focusing on their core that will benefit.

Selectivity will be key for investors ready to dip a toe back into the tech waters across the pond.

2. True pricing power, who has it?

Dan Lane

While headlines are based on yesterday, the markets are always looking beyond the now. The thing is, they don’t tell you when they’re done with one timeline and are moving on to the next.

We might be waiting for official news of a recession, but in market-world, we’re in the thick of it.

So, don’t waste your time or energy preparing for something that, in the eyes of the market, has already happened.

In fact, instead of predicting what other investors might do, focus on the companies creating value no matter what happens out there.

Those firms who told us they had pricing power, but probably didn’t, got a free ride after the financial crisis - they’re now being found out. So, be picky and don’t mindlessly buy into past successes, because it might have all just been wishful thinking.

Waxing lyrical about future world domination is all well and good but when a recession hits, investors prefer cold hard cash to those hopes and dreams.

That’s why large firms with little to no debt, sprawling revenue streams and dominant market positions can stand to benefit. Where they can show a clear ability to keep margins intact and pass price rises onto customers without annoying them, the market is likely to take note.

As we said above, the past few years may have rewarded passion over profit but we’re back in the real world now and solid earnings in Q1 will reward the winners and punish the losers.

Gemma Boothroyd

One sector we know doesn’t have pricing power is commodities.

When demand falls for oil, copper, or lithium, their prices do too. So the miners and producers don’t have the ability to raise prices in the good times and the bad without losing customers. Instead, they’ll have to adapt.

And that’s one reason why the 2023 outlook for commodities is mixed. If global growth slows as BMO Economics expects, from 3% in 2022 to 2.3% next year, demand for commodities should too.

Just because commodities don’t have pricing power though doesn’t mean they can’t be a worthwhile addition to your portfolio. But unlike in 2021 when practically all precious metals got a lift, 2022 showed the importance of having a refined taste for just the right materials.

Though, energy prices are a whole other beast. If OPEC cuts oil output in response to falling demand, then those prices will grow. This will only make matters more expensive (or more profitable, depending on where you’re sitting at the table) for the legacy energy firms in oil and gas. They could certainly be staying in vogue as long as the war in Ukraine stunts supply.

If China’s early moves to relax its zero-Covid policy are a sign of things to come, renewed appetite for raw materials in the country could unleash another bull period for commodities. As we’ve seen though, that’s a story that can change direction on a sixpence so investors should be prepared for it to change, rather than planning to pounce on any headlines.

Read more:

- Pricing power: who actually has it?

- Dividends and your stocks and shares ISA

- Your ISA allowance: what is it and how can you make the most of it?

3. Back to bonds?

Gemma Boothroyd

Gilts will never rake in glitzy returns, and nor should they.

After all, they’re supposed to provide a relatively low return in exchange for a low level of risk.

But 2022 threw that narrative in the bin. It was an especially turbulent (and frankly, unattractive) year for these assets with the deadly economic duo, Truss ft. Kwarteng, sending UK bonds into an absolute tailspin.

Though, a glass-half-full view here has led some investors to the belief these are now fairly priced assets. While out of favour for decades, 2023 might mark the return of the gilt (or at least, a return of sorts) to portfolios.

For plenty of investors, this could be their first time dabbling into bonds too.

Following one of the most volatile years on record for the stock market, it’s no wonder investors are now warily giving them a chance.

In the latter half of 2022, Freetrade users invested 11% more in the iShares GBP Index-Linked Gilts UCITS ETF (Dist.) than in H1.

It seems likely that gilt ETFs, especially those linked to interest rates, will rise in the popularity ranks this year. For starters, they offer investors an easy way to dip in and out of gilts. Buying and selling a bond ETF is usually a lot faster and easier than trading those underlying bonds themselves.

Secondly, a well-diversified bond ETF should hold a wide range of bonds with different maturities. In turn, this spreads the ETF’s exposure to changes in interest rates.

And thirdly, as it says on the tin, these ETFs aim to protect you from rising rates which could devalue your bond.

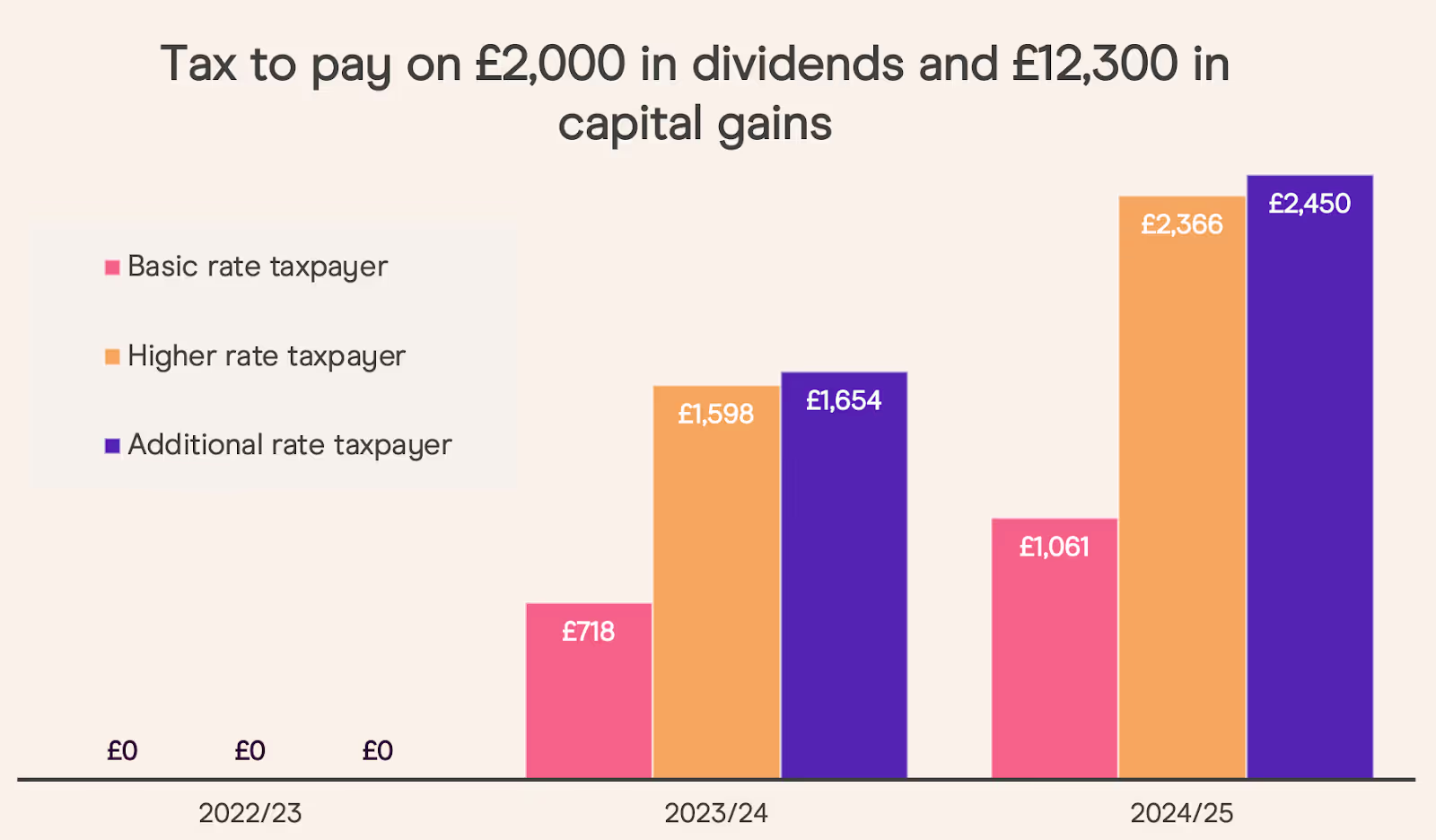

4. 2023 investment tax allowances: ISAs just got real

Dan Lane

For a while there it felt like it made sense to install a few revolving doors on Downing Street. The current bunch in charge seems to be sticking around but investors might have noticed their prudent approach to balancing the books comes at a price.

In November, the chancellor laid out clear plans to raise tax on investment gains and 2023 is when it all kicks off.

Read more

- Mistakes to avoid when transferring your ISA

- Your guide to the different types of ISAs

- ISA vs savings account

The amount we can earn in dividend income and outright investment growth (capital gains) is falling from April 2023. With both allowances being chopped in half, and then again in 2024, it means a lot of investors will pay tax on their investments for the first time.

If you haven’t thought about investing tax efficiently, then, it might be wise to at least work out if a tax-efficient account like a stocks and shares ISA or self-invested personal pension (SIPP) could help now more than ever.

Eligibility to invest into an ISA or SIPP and the value of tax savings both depend on personal circumstances and all tax rules may change.

If you aren’t investing using a stocks and shares ISA or a longer-term tax-efficient account like a SIPP you could be forking out a load of extra tax come April.

All of these hits to what investors can earn before tax kicks in mean it’s just got even more important that we make our money as tax efficient as possible. That might mean looking beyond what our current investment gains and dividend income look like, and planning for what could come down the line.

It’s a harsh reality that a lot of investors investing outside of an ISA will eventually have to stump up tax payments eventually, when they could have just used an ISA instead.

It’s still important to make sure an ISA is right for you though. It could be that you genuinely get nowhere near these allowances or tax thresholds and never plan to. But that’s often the thing with investing. Compounding small amounts and incremental contributions over the years can really build up the snowball effect that good investing is based on.

Whichever way you go, deciding if an ISA suits you or not is at least worth the peace of mind right now.

Build your financial knowledge and be in a better position to grow your wealth. We offer a wide range of financial content and guides to help you get the insight you need. For example, learn how to invest in stocks if you are a beginner, how to make the most of your savings with ISA rules or how much you need to save for retirement.

This should not be read as personal investment advice and individual investors should make their own decisions or seek independent advice.

When you invest, your capital is at risk. The value of your portfolio, and any income you receive, can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future results.

Eligibility to invest into an ISA or SIPP and the value of tax savings both depend on personal circumstances and all tax rules may change.

Freetrade is a trading name of Freetrade Limited, which is a member firm of the London Stock Exchange and is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales (no. 09797821).