For a while there it felt like it made sense to install a few revolving doors on Downing Street. The current bunch in charge seems to be sticking around but investors might have noticed their prudent approach to balancing the books comes at a price.

In November, the chancellor laid out clear plans to raise tax on investment gains and 2023 is when it all kicks off.

Read more:

ISA vs savings account

The (more realistic) ISA millionaire

Cash ISA vs stocks and shares ISA

The amount we can earn in dividend income and outright investment growth (capital gains) fell in April 2023. With both allowances being chopped in half, and then again in 2024, it means a lot of investors will pay tax on their investments for the first time.

If you haven’t thought about investing tax efficiently, then, it might be wise to at least work out if a tax-efficient account like a stocks and shares ISA or self-invested personal pension (SIPP) could help now more than ever.

Eligibility to invest into an ISA or SIPP and the value of tax savings both depend on personal circumstances and all tax rules may change.

2023/24 dividend and capital gains allowances

If you aren’t investing using a stocks and shares ISA or a longer-term tax-efficient account like a SIPP you could be forking out a load of extra tax come April.

Often, investors will opt for the cheapest investment account out there and on the surface that makes sense. Why pay more than you have to? But investing solely in a general investment account (GIA) because it has a lower headline cost than an ISA risks missing the whole point, tax.

Now, it may be that you’ve decided you’re unlikely to go above your personal investment tax allowances. In which case, it’s probably true that an ISA wouldn’t be as useful. But, given those allowances are coming down fast (see the chart above) it’s maybe worth revisiting those assumptions.

New UK dividend tax allowance from April 2023

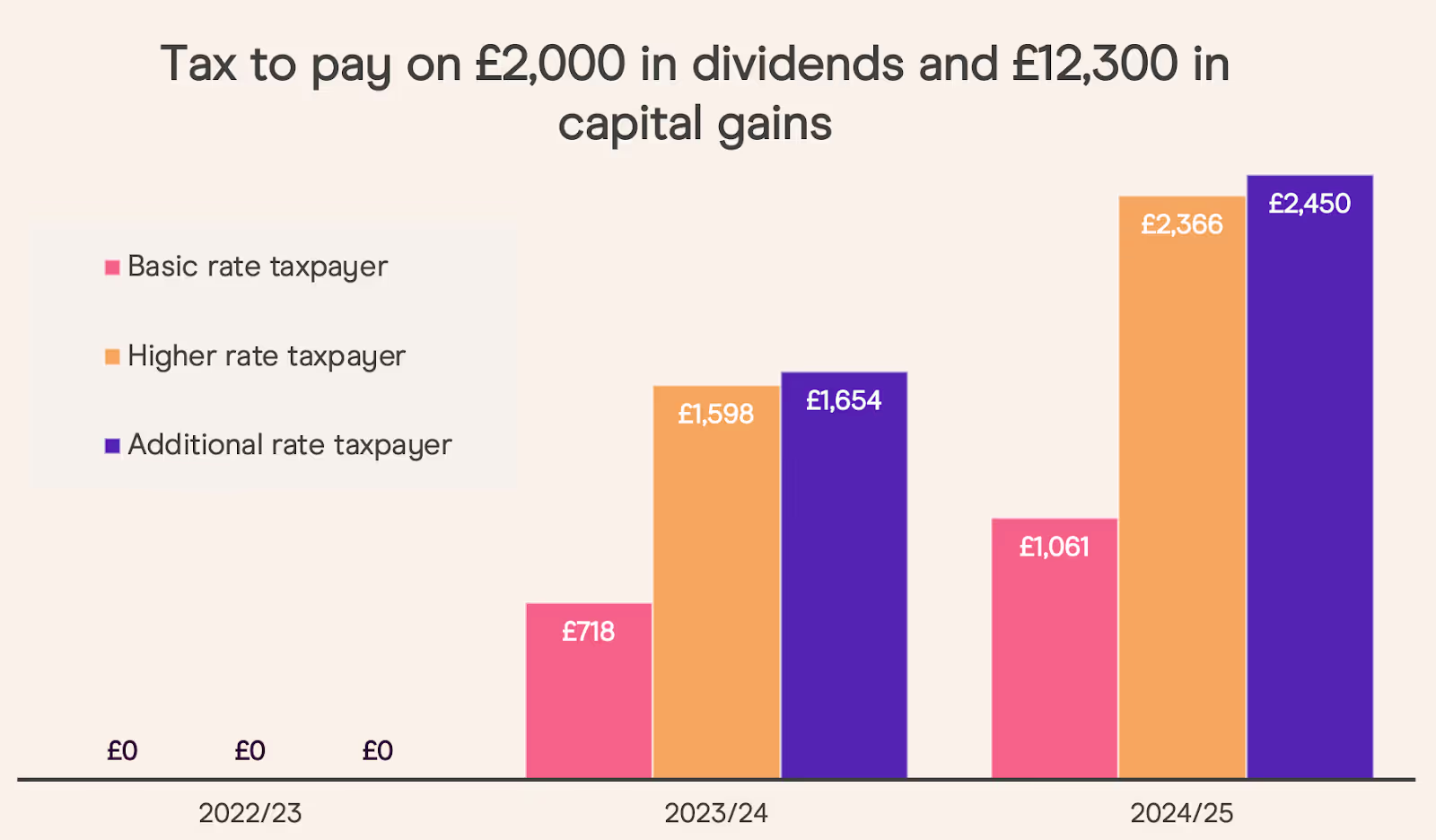

Putting the changes to the dividend allowance into perspective, a basic rate taxpayer earning £2,000 in dividends in the 2022/23 tax year, and earning the same dividend income for the next two years, would suddenly have to pay £87.50 in 2023/24, then £131.25 in 2024/2025.

Read more:

Your pocket guide to ISAs

What is a stocks and shares ISA?

Subscribe to Honey by Freetrade, our free investing newsletter

The rise in dividend tax is even more pronounced for higher rate taxpayers, who would pay £506.25 in 2024/25, and additional rate taxpayers, who’d owe £590.25.

That’s a big chunk of change for anyone, and let’s not forget it could be even bigger if your dividend payments grow, like we all hope they do.

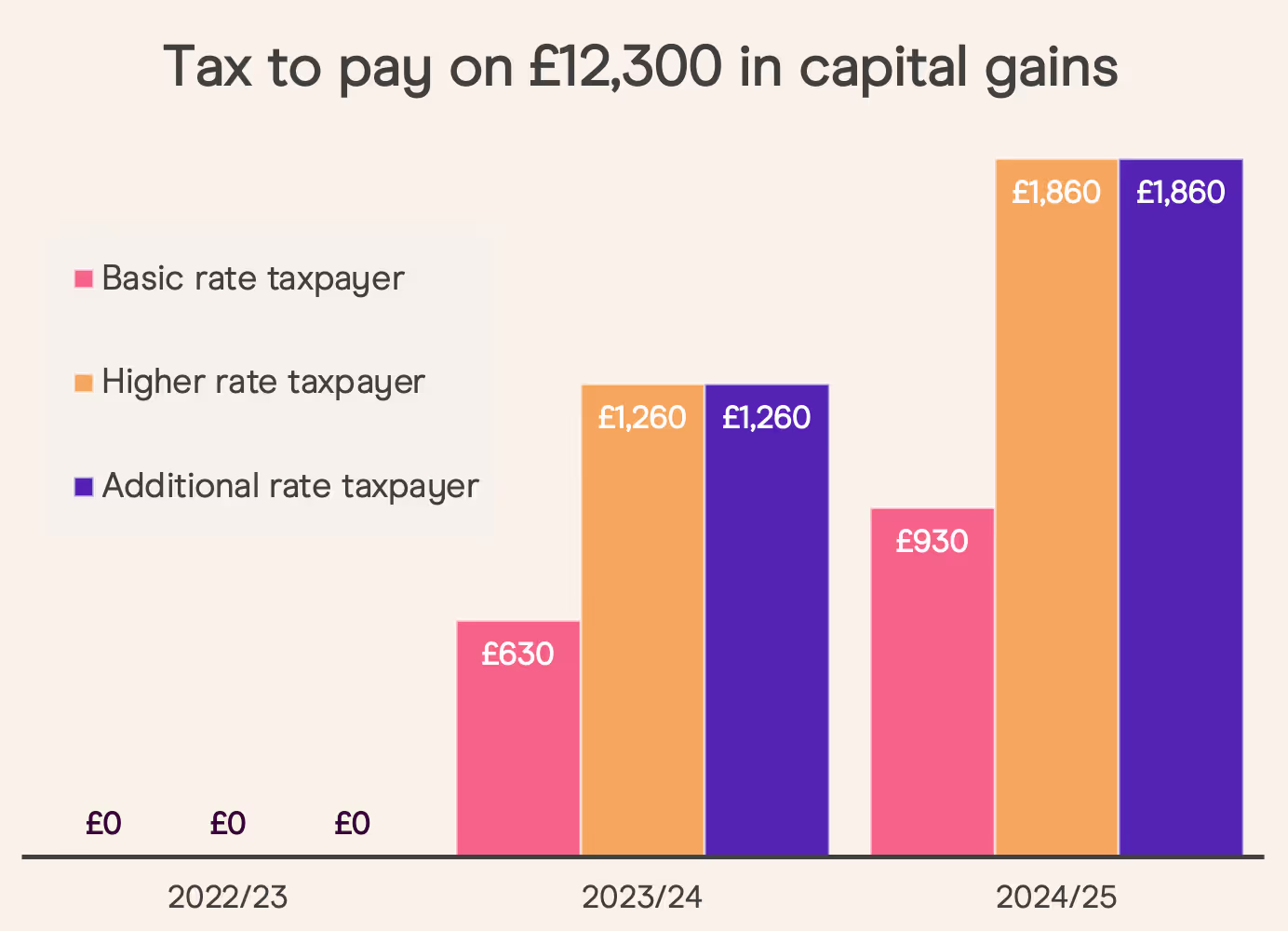

New UK capital gains tax rates from April 2023

Dividend allowances aren’t the only limits that got the chop in the 2023/24 tax year. The amount we can earn from the growth of our assets and not pay UK tax each year (your capital gains tax allowance) also fell from £12,300. First, to £6,000, then to £3,000 next year.

Of course, if you don’t sell any assets it doesn’t matter all that much right now. But eventually we all want to hit the sell button and actually put that money to use. And it’s at that point that we’ll potentially have to pay tax on any gains we’ve made.

The thing is, making all that hopeful growth tax efficient needs to start long before you actually sell up and move on. If you get to that stage, the last thing you want is to be kicking yourself just because you didn’t use the most tax-efficient account to begin with.

Get planning for lower allowances and higher tax rates

It’s even more important to lend a thought to tax efficiencies when you consider the route most of us want to take is into the higher tax bands at some stage in our working lives. With that prospective rise in salary and tax rate comes a rise in dividend and capital gains tax rate too.

For example, going from being a basic rate taxpayer to being a higher rate taxpayer means potentially paying 33.75% instead of 8.75% on dividends above the allowance.

That’s even more of an issue for the UK’s highest earners from April 2023 as the additional rate income tax threshold came down from £150,000 to £125,140. Granted, this bunch might not get a whole lot of sympathy from the rest of the nation’s savers and investors.

Read more:

2023 ISA income investing

Dividends and your stocks and shares ISA

Choosing the right investment account: GIA or ISA?

But the fact remains that anyone tipping the scales above £125,140 suddenly found themselves in a 45% income tax band, a 39.35% dividend tax rate, 20% in capital gains tax and staring down the barrel of two successive reductions in investment tax allowances.

Get ISA ready

All of these hits to what investors can earn before tax kicks in mean it’s just got even more important that we make our money as tax efficient as possible. That might mean looking beyond what our current investment gains and dividend income look like, and planning for what could come down the line.

It’s a harsh reality that a lot of investors investing outside of an ISA will eventually have to stump up tax payments eventually, when they could have just used an ISA instead.

It’s still important to make sure an ISA is right for you though. It could be that you genuinely get nowhere near these allowances or tax thresholds and never plan to. But that’s often the thing with investing. Compounding small amounts and incremental contributions over the years can really build up the snowball effect that good investing is based on.

Whichever way you go, deciding if an ISA suits you or not is at least worth the peace of mind right now.

Build your financial knowledge and be in a better position to grow your wealth. We offer a wide range of financial content and guides to help you get the insight you need. For example, learn how to invest in stocks if you are a beginner, how to make the most of your savings with ISA rules or how much you need to save for retirement.

Important information on SIPPs

SIPPs are a pension product designed for people who want to make their own investment decisions. You can normally only access the money from age 55 (set to rise to 57 from 6 April 2028).

Before transferring a pension you should ensure you will not lose valuable guarantees or incur excessive transfer penalties. Pensions are usually transferred as cash so you will be out of the market for a period.

Freetrade does not currently offer drawdown products for our SIPP.

When you invest, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future returns.Freetrade does not give investment advice and you are responsible for making your own investment decisions. If you are unsure about what is right for you, you should seek independent advice. ISA and SIPP eligibility rules apply. Tax treatment depends on personal circumstances and current rules may change. Check before you transfer and ISA and/or SIPP that we can accept your investments, you won’t lose any guarantees, and that you know what charges you may incur. A SIPP is a pension designed for you to save until your retirement and is for people who want to make their own investment decisions. You can normally only draw your pension from age 55 (57 from 2028), except in special circumstances. At present, Freetrade only supports Uncrystallised Fund Pension Lump Sums (UFPLS) for customers who wish to withdraw funds from their SIPP after their 55th birthday. We strongly encourage you to seek financial advice before making any withdrawals from your SIPP. Freetrade is a trading name of Freetrade Limited, which is a member firm of the London Stock Exchange and is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales (no. 09797821).

.avif)

.avif)