Get ready to hear a lot more about individual savings accounts (ISAs).

Your annual allowance (we'll go into what that is in a sec) for an individual savings account runs until early April so you'll probably see big posters as we inch closer to that period of time, guiding you politely towards using yours.

That means now seems like a good time to get to grips with these ISAs, their tax rules, and how you might use these tax wrappers for your own individual circumstances.

Read more:

The (more realistic) ISA millionaire

Is crypto right for my ISA?

ISA investors, keep your coffee

What is an ISA?

An ISA is an account you can put your money into to leverage certain favourable tax treatments. This article is focused on two of the five types of ISAs. We'll dive into stocks and shares ISAs and cash ISAs, but you might want to brush up on innovative finance ISAs, help to buy ISAs (closed to new applicants since 2009), and Lifetime ISAs as well.

For a full rundown on all of them and how they might be beneficial for your personal goals and financial decisions, check out this guide on the different types of ISAs.

You might choose a stocks and shares ISA (one of the four types of ISA currently available) with the hopes of achieving investment returns by investing in a wide range of assets, to increase the likelihood you’ll meet your future financial goals.

There are important benefits included in this ISA, like not paying tax on dividend income from the UK as well as not paying capital gains tax on gains from your investments. You also have the flexibility of putting money in (be it a single lump or regular contributions) and taking it out when you need it. Be aware that withdrawal charges may apply, depending on your ISA provider.

You should also note that withdrawing any amount from your Freetrade ISA will not increase your subscription limit for that tax year, and you may not be able to pay any withdrawn amount back into your Freetrade ISA in that same tax year if you have already reached your limit. For more information, you can check out our Freetrade ISA Terms which outline transfers in, out, and withdrawals.

Read more:

Dividends and your stocks and shares ISA

How to diversify your portfolio

What is a stocks and shares ISA?

A key thing to understand from the get-go is that the stocks and shares ISA is just the outer shell for you to fill with your investments (these could be stocks and shares in companies, investment trusts or ETFs, to name a few) - but the ISA isn't an investment itself.

That's why you'll often hear it described as a ‘wrapper' - you get to decide on the filling.

And the reason you'll hear that term be one-upped to a ‘tax wrapper' is because when you put your investments in an ISA, you’ll benefit from tax efficiencies.

That’s because the most common way to add money to your ISA is from your post-tax pay. Meaning, this money has already been taxed, unlike pension savings which skip tax on the way in and only get taxed on the way out.

A cash ISA (another one of the four available) differs from an investment ISA, as it's more to help you set aside cash to save up for your emergency fund or day-to-day expenditures. These cash ISAs might be fixed-rate cash ISAs, based on the presiding interest rate when you open an account, or flexible cash ISAs, which could have a variable rate that changes according to the presiding UK interest rate at the time.

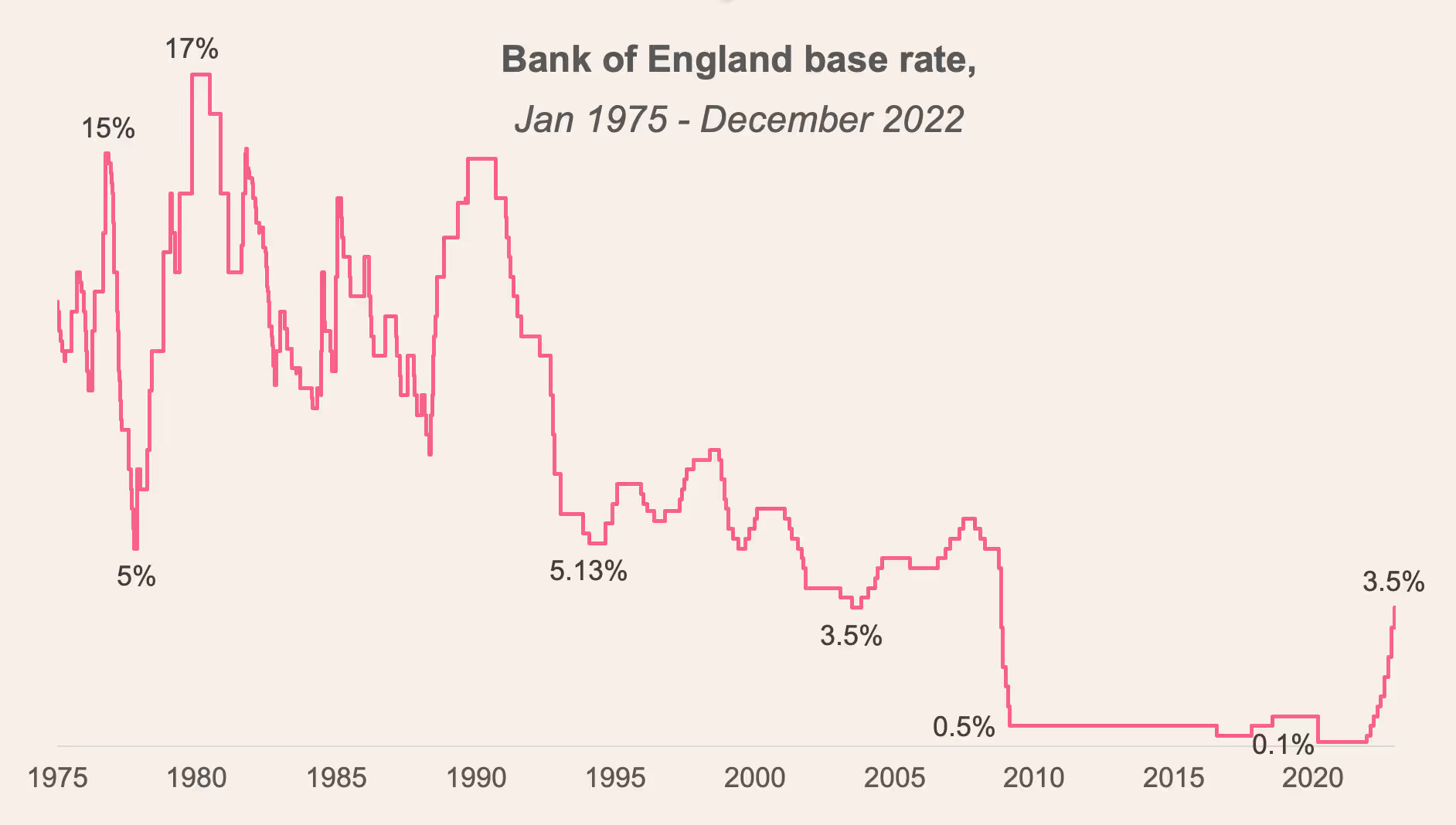

But the return on a cash ISA isn't great, and it's particularly low in the context of rising UK inflation. While a variable rate cash ISA might be better primed to take advantage of rising interest rates, those rates are still falling very short of the 10.7% annual UK inflation rate as of November 2022.

That said, if you have a short time horizon (or you're not yet sure of what that horizon even is), and are seeking a low level of risk with the main goal of preserving your capital, then these ISAs could be right for you.

If you want that money to grow and are comfortable with the element of risk involved with investing in the stock market, then a stocks and shares ISA is probably more up your street.

Though, as with anything when it comes to investing, there is always the potential downside of the value of your stock market investments going down as well as up. And it's important to be comfortable with putting this money aside for a fair bit of time, say at least five years, to take advantage of the long-term benefits of the stock market.

Read more:

Cash ISAs and stocks and shares ISAs

How to invest £1,000

How to value stocks

How much can I invest in an ISA?

ISAs and their tax benefits are capped at the annual contribution limit across all of your ISAs.

The current-year contributions limit is set at £20,000 from 6 April 2023 to 5 April 2024. Keep an eye out though as these allowances can change each tax year.

Whether you choose to open one type of ISA per tax year or a few of them, your combined contributions into all of them can’t go above that £20,000 in a single tax year.

You should also bear in mind that you can't roll over any unused allowances. So if your personal circumstances permit, try to use as much of your personal allowance as you can to maximise the benefits ISAs can offer. You don't have to do that in one go though, there’s no need to deposit all of your cash in one initial lump, you can make as many eligible deposits in a given tax year as you'd like.

The caveat here is that you can only open one type of ISA in a given tax year. For instance, you can only open one stocks and shares ISA with one provider each year.

If you find another company whose fees are lower, though, or whose platform just suits you better, you can either transfer your current ISA or wait until the new tax year to open a brand new ISA with them. Make sure you understand your current provider and future provider's transfer rules before you fill out the transfer form. Sometimes this process can come with fees attached.

When should I start investing in an ISA?

This brings us back to the investment ISA (or stocks and shares ISA) being the outer shell again. Once it comes to deciding when or why you should start investing (in an investment ISA or not) it's a very personal choice.

Everyone has their own goals and unique financial circumstances. These, along with your tolerance for investment risk and time horizon, should inform the mix of investments you choose for your ISA, if the decision to open one seems right for you.

Our resource hub for investing in the stock market and guides like those on how to start investing and the best investments for beginners might help make that blend a bit clearer for you. But if you are still unsure of how to pick investments, speak to a qualified financial advisor to develop your own investment strategy.

If you're ready to start investing and just umm-ing and ah-ing about when the best time is to start, then we might have the answer you’re looking for.

Investing is all about giving your money enough time to build up that snowball effect of compound interest.

Read more:

2023 ISA income investing

Dividends and your stocks and shares ISA

Choosing the right investment account: GIA or ISA?

As we mentioned above, time is such an important part of investing - the longer you give your money to grow, the better.

And while there are no guarantees on individual investment performance, when you take a step back and look at the history of stock markets, the trend goes towards the top right of the page.

As a simple illustration of compounding, imagine you put £10,000 into your stocks and shares ISA, and then you start to choose your own investments.

If those investments grew by 5% in the first year, you'd have £10,500. (Please note continuous 5% growth is not realistic. Some years it could be more, and some years less.)

In the second year, your initial £10,000 is still able to generate returns or losses, but now that extra £500 is too.

If you achieve 5% growth by the end of your second year, your new total would be £11,025 thanks to your growth generating its own growth. That's the beauty of compounding.

And remember, when your balance grows within your ISA, this isn't going towards your annual contribution limit. Your returns can generate in a tax-free way as long as your deposits are within the annual allowance limit. That means if you stay within your £20,000 allowance for 2023/24, then you won't pay taxes on capital gains from stock market investments, or on dividends from UK investments.

Back to our example again. Assuming this 5% growth continues (again, just an illustration) your initial £10,000 could become over £16,000 by the 10th year and over £26,000 by year 20.

Of course, it would be a bit weird and unlikely to generate exactly the same returns each year, but the point remains that time and compounding are two forces that work best the earlier you start.

As an old colleague always told me, “The best time to start investing was 50 years ago. The second best time is today.”

.webp)