Pensions. They don’t always have the best reputation.

Maybe you’ve put them off for being too complicated, something you need loads of money for or just don’t need to think about until later in life.

But the truth looks a little different.

They don’t have to be complex, you don’t need loads of money to start, and the sooner you can start, the better.

Even better, if you’re employed and over 22, you probably already have.

Before we start, it’s important to understand that the value of your investments can fall as well as rise, so you might get back less than you originally invested. You also need to be aware that pension and tax rules can and do change. Any tax treatment depends on your individual circumstances.

What type of pensions can you choose from?

Before we dive into how to start a pension, it’s important to set the scene, as there are a few types of pensions in the UK. Some you set up yourself and others you don’t.

Workplace pension

This is set up by your employer if you’re over 22 and you meet the necessary criteria. This is known as auto-enrolment (1).

With a workplace pension both you and your employer tend to add money over the time you work there. So the size of this pension pot depends on how much goes in it and how the investments perform.

The State Pension

This is provided by the government when you reach State Pension Age (which is currently 66 but rising to 68 by 2039)so long as you have built up the required number of national insurance payments.

To get any State Pension you’ll need at least 10 qualifying years on your National Insurance record and to get the full State Pension you’ll need 35 years.

As a gauge of what you’d get, if you currently qualify for the full new state pension (so you’ve reached State Pension Age and have the required national insurance record) you’ll get £179.60 a week (2).

💡 Check out our guide for more info on the different types of pensions in the UK.

Personal pension

This is a pension you start yourself and contribute to over time. There are a few types of personal pensions to choose from including ordinary, stakeholder and SIPPs (self-invested personal pensions).

The main difference between them is investment choice.

Ordinary or stakeholder personal pensions, tend to offer you a restricted number of funds to choose from.

SIPPs on the other hand tend to offer more investment choices. From stocks to ETFs or investment trusts you decide what your pension is invested in.

Why does all this matter?

Firstly we think it’s important that everyone gets the full pensions picture.

We also think it’s important to be upfront and say that when it comes to a comfortable retirement, whatever that might look like for you, a workplace and State Pension may not cut it.

Our ability to retire and live the life we’d like to, is more than ever before, on us.

And this is where a personal pension could come in.

Why start a personal pension?

People start personal pensions for all sorts of reasons but here are some of the main ones.

📝 You’d to have more control over your retirement

Having enough money later in life is not guaranteed by a workplace or government pension. Adding a personal pension into the mix could help you take control and invest more for those later years.

📝 You are self-employed

When you work for yourself, your pension is your responsibility. A personal pension may be your key to retirement.

📝 You’d like to choose your own investments

How your pension is invested could be the difference between a comfortable and not-so-comfortable retirement. With a personal pension and in particular with a SIPP, you make the investment decisions.

📝 You’d like your pensions in one place

It’s important to hold on to old pensions and bringing old pensions under one roof could be the answer. You know where your pensions are, how they are performing and exactly what you’re paying in fees too. A personal pension is a place where you can transfer and combine old pensions.

How to start a pension

Starting a pension doesn’t need to be tricky.

Here are a few steps we suggest thinking about:

7 steps to start a personal pension

1. Check if a personal pension is the right account for you

Personal pensions are designed to help you save and invest for retirement. You can’t access your money until you are at least 55 years old, so double check you’re happy with this first.

If being able to access your money before 55 is important, a stocks and shares ISA might be more appropriate. Check out our guide on SIPP vs ISA for more info on choosing between the two.

2. Choose a pension provider

When it comes to choosing the best pension provider for your needs we think it’s best to think in terms of two things: features and fees.

For features here are some things to think about:

- How experienced an investor are you?

- Do you want to choose your own investments?

- What would you like to invest your pension savings in?

- Would you like your other accounts e.g. ISA in the same place?

- Is access to investment research important?

- Would you rather access your pension via an app, web or both?

Here are the fees to understand:

- Platform charges - how much the pension account costs

- Trading commission - how much it costs to place a trade or invest

- Foreign exchange fees - how much you are charged to buy overseas investments

- Ongoing charges - how much you are charged for products like ETFs, investment trusts and funds

- Exit charges - some providers will charge you for leaving

- Drawdown fees - how much it costs to start taking money out of your pension

Keep a particular lookout for any percentage account fees. If your pension pot grows, your account fees will too and this will impact your pension’s growth.

Check out our investment fees calculator to compare charges across different SIPP accounts.

3. Open a personal pension

Once you’ve chosen the personal pension provider for you, it should only take a few minutes to set up an account. You’ll likely be able to do it online or via an app.

Learn how to open a SIPP account with Freetrade.

4. Contribute to your personal pension

When it comes to saving enough for retirement, habits are key.

And one of the most important habits is investing regularly.

For some, this might mean investing monthly, perhaps in line with your wages. But for others, this might be a few lump sum contributions a year or an annual deposit.

The sooner you start, the sooner your contribution is boosted by tax relief and the more time you give your pension pot to grow.

Take a look at the next section ‘when should you start a pension’ for an example.

5. Invest your pension

What’s in your pension in your 20s and 30s should look a little different to your 40s, 50s and beyond.

Time is on your side when you’re young, particularly since you can’t touch the investments until at least 55 years old (and likely older). So you should be able to afford to take on more risk, for instance, by investing more in shares rather than bonds.

But as you move closer to using your pension, you’ll likely need a bit more certainty when it comes to the value of your SIPP investments and the income they could provide.

That’s why we tend to see a shift from share heavy SIPPs in the earlier years like your 20s, 30s and some of your 40s but a shift towards assets that tend to hold their value in the short term like cash or bonds as people get closer to using their SIPP.

💡 Learn more in our guide to understanding investment risk.

6. Transfer and combine old pensions

More often than not, each new job brings with it a new pension pot.

And as we’re all moving jobs a lot more, lost pensions are a real and growing problem.

When it comes to a pension we need to know where it is, what it’s invested in and how it’s growing.

Check out our guide on how to find old pensions and learn how a pension tracing service could help.

Once you’ve found your old pensions, you can then decide what to do with them.

You can keep them where they are (often a good idea if there are big benefits attached) or you could transfer those old pensions into one account.

People tend to do this to get a clearer picture of things like performance and costs while reducing admin and to start making the investment decisions themselves.

Head here for more info on how to transfer old pensions.

💡 Before transferring your pension to Freetrade, make sure it is the right action for you to take. It might not be if you could lose valuable guaranteed benefits. Some people speak to a financial advisor to help them make this decision.

7. Check pension performance

Just because you can’t access the money in your pension until 55 (57 in 2028) doesn’t mean you should wait until then to see how your investments have performed.

Check in every year or so to see how your pension pot is doing and whether you are on track to reach your retirement goals. This way, nothing will be a surprise when you reach retirement, and you’ll be well aware of what your pot has in store.

When should you start a pension?

The answer really is the sooner the better. And here’s why.

The earlier you start saving into a pension, the more opportunity you’re giving your pension investments to grow and benefit from compounding.

The importance of compounding can’t be understated here and it’s best explained by showing you some numbers.

Compounding example

Let’s say a family member gives you £100 for a birthday and they tell you from now on, each year they will give you 5% more than last year.

Once your next birthday comes around, so does the card and their cash. But this time, there will be the £105 inside, 5% more than last year.

The year after you get £110.25 and wonder if they’ve done the maths wrong. But it’s right, £110.25 is 5% more than last year’s £105, the little bit extra is because it was 5% of a slightly bigger number (105 not 100).

Fast forward to 5 years into this arrangement and you get £127.63. You can start to see how each year the same 5% is applied to a bigger number. And the result is your family member having to shell out increasing amounts of cash while you get to rake in the extra birthday dough.

After 15 years, 5% applied to an increasingly bigger pot means your birthday gift has doubled to £207.89.

Stepping back into the investing world, compounding works in the same way, it just won’t always be 5%. Some years it might be 5%, others -5% or even 0%. This all depends on what you’ve invested in.

The earlier you invest the earlier you can take advantage of compounding. It really is the secret growth sauce.

So why does this matter for pensions?

The earlier you start making contributions to your pension, the better.

It gives more time to build up a bigger pension pot, to benefit from tax relief and the opportunity for your savings to grow.

The later you leave it, the less time you’ll have for any compounding and it’s going to cost.

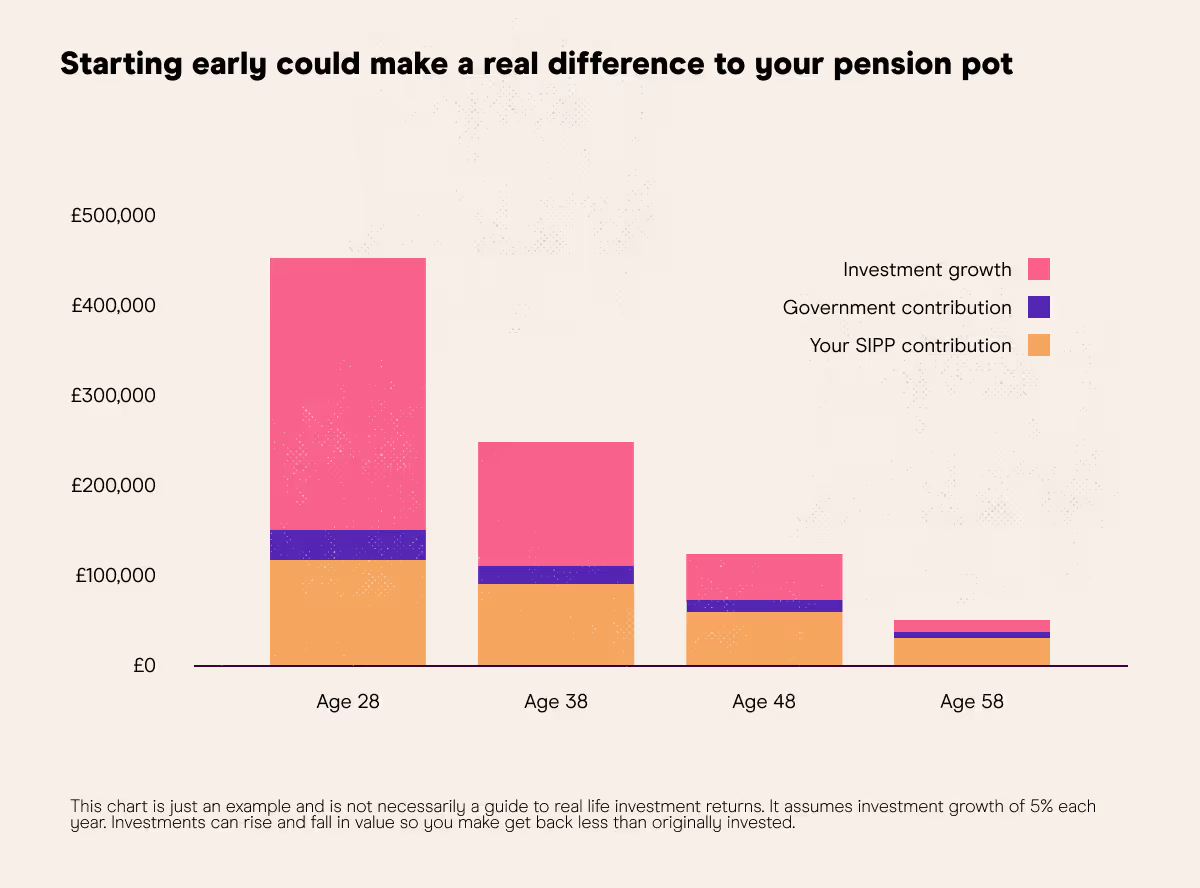

Here’s an example.

Each month you save £250 into a pension which means you’ll get £62.50 (20% basic rate tax relief) added automatically to your pension too.

So a £312.50 monthly pension contribution in total.

We’ve assumed your pension pot is invested and grows each year by 5%. In reality, some years it might be more and others less.

You can see clearly from the chart, the later you start contributing to a pension the less growth you’ll see and the bigger the gap you’ll have to fill.

And this is even before considering any increases in the amount you contribute.

The investments in this example grew at 5% annually, every year, but it’s important to remember that this isn’t guaranteed. Some years it might be more and others less because you are buying things that can go up and down in value and could lose their value altogether.

This is why you see the warnings ‘capital at risk’ because what you’ve put your money in can change in value. You could get less than you put in.

Over the long-term (20, 30 years and more), however, investors in the stock market have historically been rewarded with a higher rate of return than just keeping savings as cash.

How old do you have to be to start a pension in the UK?

If you’re starting a personal pension for yourself you’ll need to be between 18 and 75 years old.

With a workplace pension, it’s slightly different. You’ll be automatically enrolled in a pension scheme by your employers from 22 years old if you earn over £10,000 a year.

While it won’t happen automatically, you can ask to join your workplace pension scheme from 16 years old.

Figuring out how much you need to retire

How much you’ll need to live off in retirement is different for each and every one of us.

It depends on a few key things like the lifestyle you’d like to have, other income you may have coming in (e.g. state pension) and what’s being paid out (e.g. on a mortgage or care costs).

When we start actually thinking about this, retirement can feel like it’s a lifetime away. Estimating ‘how much’ isn’t an exact science, luckily there are useful benchmarks around.

💡 We’ve dug into the details in our guide to pension planning and how much you need to retire, so take a look.

Starting a pension in your 20s and 30s

As we’ve mentioned, auto-enrollment means if you started work in 2012 or more recently, it’s likely you have already started saving into a pension through a workplace pension scheme.

That’s not necessarily job done though.

Do you know how much is going into your workplace pension?

At least 8% of your annual salary will go towards your workplace pension and your employer must pay at least 3% of this. But often they will pay more or increase their payments if you do too, so it’s worth checking.

Are you paying enough into pensions?

The answer to this falls back to your plan.

Compare how much you are paying into your workplace and any personal pensions, with how much you need to reach your retirement pot and income goal.

Could you afford to add more? If so, it may be worthwhile considering how that little bit extra now could mean much more in the future.

What are your pensions invested in?

How your pensions are invested can make all the difference when it comes to what type of retirement you will able to afford.

If you’d like to decide how you pension is invested, a SIPP account could be worth looking into.

💡 For more details on pension strategies check out our guide to pension savings in your 20s and 30s

💡 If you’re self-employed, remember the world of workplace pensions is unlikely to apply to you. Check our guide to self-employed pensions.

Starting a pension in your 40s

If you’re starting a pension in your 40’s, you will likely have a bigger gap to plug.

But the important thing to know is that there is still time. Nowadays, we’re all likely to be working for a lot longer. And you can still contribute to a pension and get tax relief up until 75 years old.

That’s why pension questions to be asking in your 40’s are no different to the earlier years. n fact, deciding how much and which investments to choose is even more crucial.

Is it worth starting a pension in your 50s or 60s?

Yes and yes.

When it comes to saving for retirement, something is better than nothing.

And remember, you can still contribute to a pension and get tax relief (up to certain amounts) until you’re 75.

Similar to starting in your 40’s, questions like ‘how much’ and ‘which investments’ become even more important as you move closer to your retirement age because your might have to start using it.

Rather than a portfolio weighted heavily towards shares, you’ll probably need to have a higher proportion of assets that hold their value in the short term - such as cash or bonds.

💡 We’ve gone into the details in our guide to pension savings in your 40s and 50s.

What to do once you've started a pension?

Once your pension is up and running and you’ve chosen your investments, your hard work is done for now.

As we’ve already mentioned it’s a good idea to check in on your pension every now and again, to see how it is performing and if you need to change how much you are contributing.

Building your wealth over the long term should help you create a more stable financial future. Open an ISA account or transfer from another ISA provider and make the most of your £20,000 annual ISA allowance. Alternatively, start your personal pension early by regularly contributing to a SIPP or moving old pensions to a single SIPP pension pot. Find out how to choose between an ISA and a SIPP.

.webp)

.avif)