The sun’s out, someone has turned up the thermostat and we’ve taken a big step forward towards normality. The past few days have changed 2021 as we know it.

And the market seems to have decided to chop the year in half too.

The ‘reopening trade’ gathered momentum right up until we actually reopened. Up until now, expectations of government spending, economies finding their feet again and consumers spending lockdown savings had all gone some way to support markets.

The UK's top index hasn’t felt entirely comfortable setting up camp above the 7,000 mark since May though. And the extent of fears over a spread of the delta variant and those stubborn inflation figures finally made themselves known over the past few days.

Investors have clearly started to look past the reopening trade to what might be the driving forces behind markets for the rest of 2021.

That’s not to say it’s the end of government spending and consumers supporting corporate earnings but there are a few more possible influences the market is eyeing up.

One theme investors are honing in on now is whether it’s time to back lowly-valued economically sensitive stocks or stick to the big growth pandemic winners.

Here are some things to keep in mind as chat around that balance starts to heat up.

Love it or hate it, ‘growth vs value’ rages on

Like Sisyphus and his favourite rock, there’s just no let up in the growth vs value debate.

We’re all sick to death of hearing both sides slug it out by now but it might actually be getting interesting again.

Big quality growth companies like Ben and Jerry’s-owner Unilever certainly had the edge as income-starved investors hopped into large dividend-payers since the financial crisis.

These stocks passed the baton to the tech giants over lockdown and, despite periods when their shares have looked a bit lofty, shareholders seem to be sticking around.

Lowly-valued old economy stocks in energy, banking and airlines have steadily come back onto the radar as a result, as they can tend to do well in times of economic recovery.

What that means though, is that both approaches make a fairly decent argument at the moment.

Read more:

A guide to investing in commodities

Banks: selling picks in the IPO gold rush

Sign up to Honey, our daily market newsletter

The big names that have shone through the pandemic don’t look excessively vulnerable to life after Covid just yet, and companies hoping for a post-corona economic boost could have a beast of an opportunity set ahead of them.

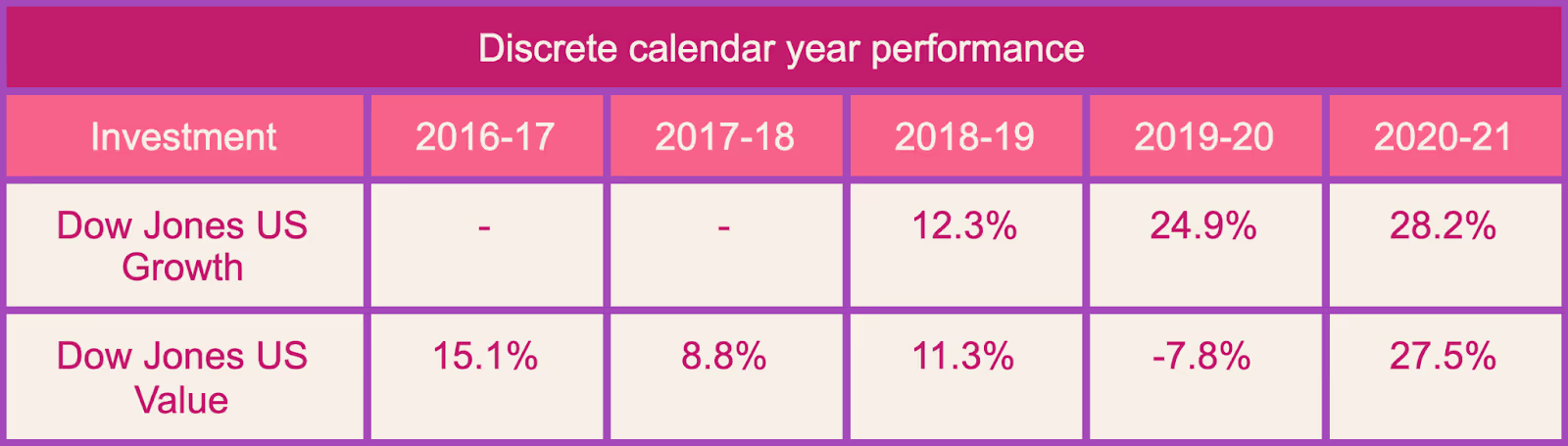

And the market seems to agree. Over the past year the Dow Jones US Growth index is up 28.2%, with its value-oriented cousin up 27.5%.

That near-identical performance is obviously backward looking but it reflects how investors are shaping up their portfolios for the rest of the year and beyond.

Their trajectories from here will depend on the magnitude of the global economic recovery and just how relevant those Covid winners can stay when normality ultimately resumes.

Is the US-UK rotation still on?

Funds set on buying forgotten or overlooked companies like Fidelity Special Values got a boost in November as vaccines arrived and investors started to allow themselves to think about economies eventually opening back up.

But maybe the best example of how the growth-value tussle played out earlier this year was investors leaping out of US tech at the end of February.

Just as US tech-heavy portfolios like the iShares S&P 500 Info Tech ETF sold off, UK-focused value options like Special Values went the other way.

The interesting part here is that, while valuations across the water might have felt a bit too high heading into March (with a price-to-earnings ratio of around 22), the overall US market is actually no more expensive now than it was then.

When PE ratios look high - one of two things normally happens. Either that price comes down eventually if the earnings are too low to support it, or the price stays put and the earnings jump up enough to make the price reasonable in the market’s eyes.

And those big US names have been able to back up those high prices with their earnings so far.

They might not justify a 2020-style nosebleed-inducing price hike but they’ve gone some way to assuage a few fears that the pandemic favourites would drop out of the sky as soon as investors thought about normal life again.

That might be welcome news for tech investors but it also means the US large cap space really isn’t ripe for bargain hunting now.

Given this backdrop, and the fact that the UK’s valuation trails all major global regions, there’s a case for a more pragmatic approach to the rest of the year.

Low PEs can tell you that the broader market hasn’t factored higher earnings (the bottom part of the calculation) into the price yet, or that the stock is on its way out.

That’s the game value investors are always trying to get on the right side of. But inflation coming back might just be the trigger this side of the market needs to joly life back into those prices.

What shares should I buy to protect against inflation?

If inflation starts to bite and turns out to be more than ‘transitory’ those seemingly boring, dusty old UK large caps might attract investors, at the expense of last year’s winners.

The UK index is big on miners, banks and companies with strong pricing power.

Commodity producers tend to raise their prices in line with inflation because their cost of production goes up. If you’re getting resources like gold, silver or lithium out of the ground, you can alter the price at source and hopefully maintain your margin as buyers come in.

Banks have been out in the wilderness in an era of low interest rates. They make a lot of their money on the difference between the interest they give you on your savings and what they charge you to take out a loan.

That’s been difficult with benchmark rates so low but, if they rise as a result of inflation growing, banks could benefit.

More broadly, you might want to hold companies that can attract customers and provide relatively resilient profit margins through thick and thin.

Consumer favourites with loyal followings tend to be able to raise prices and maintain their audience, up to a certain point.

If in doubt, be Coke

Warren Buffett’s 2013 point on Coca-Cola is a good way to think about it.

Given that Coke was selling 1.8 billion 8oz servings every day, if the firm had added a penny to the cost of each serving it could have raked in $18 million more each day.

Not every company is Coca-Cola but market-leading brands with strong balance sheets and the ability to do something similar can become very attractive when push comes to shove.

There’s still a big ‘if’ around inflation though.

In most countries, but especially in the US, consumer prices have spiked. But they might just be a short-term anomaly on the back of lockdowns last year. We just don’t know yet, which makes the case for being ready for either eventuality.

Past performance is not a reliable indicator of future returns.

What's your take on the old growth vs value argument? How are you positioned for the rest of the year? Let us know on the community forum:

Learn how to make better investment decisions with our collection of guides. They explain in simple language how to start investing if you are a beginner, how to buy and sell shares and how dividends work. We’ve covered investment accounts too, and how an ISA or a SIPP could be good places to grow your investments over the long term.

When you invest, your capital is at risk. The value of your portfolio can go down as well as up and you may get back less than you invest. This should not be read as personal investment advice and individual investors should make their own decisions or seek independent advice. Past performance is not a reliable indicator of future results.If you are unsure whether a product is right for you, you should contact a qualified financial advisor.Freetrade is a trading name of Freetrade Limited, which is a member firm of the London Stock Exchange and is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales (no. 09797821).

.jpg)

.avif)