.avif)

Covid-19 hit emerging markets hard. With a high dependency on manufacturing, pockets of EM economies dried up overnight as orders came to an abrupt halt.

Those who did manage to maintain supply chains were forced to rethink costs, fulfilment capabilities and often new negotiated rates. And that’s just one sector in a vast selection of global emerging economies.

But the IMF’s World Economic Outlook update from October 2020 predicts emerging market and developing economies’ GDP will rebound from last year’s falls to 6% and 5.1% expansions in 2021 and 2022.

Part of the reason for that is how different emerging economies look than many investors realise.

Emerging markets are developing

It’s been too easy to tar all emerging market investment opportunities as a kind of ‘all or nothing’ approach to risk and reward. Such a large opportunity set will always yield some standout winners among a crowd of also-rans but there’s more going on than unique stories.

Over the past ten years, governments in developing nations have increased the adoption of technology at a state and consumer level and rates of participation in financial systems have increased.

Many emerging economies have felt the challenge of integrating all corners of their populations into the financial system but governmental reforms and better technology have boosted efforts.

It is this example of active inclusion and creating ways to drive social and financial progression that has long attracted investors to emerging market equities.

Why invest in emerging markets?

The growth potential of countries creating wealth for themselves and taking part in consumption, and the companies springing up to serve them, has been at the forefront of investing in emerging markets.

Favourable demographics in the form of young and increasingly educated populations as well as already evident GDP growth in countries like China form the basis of many investment theses.

As countries industrialise and go through waves of wealth creation, consumption and domestic stability, companies can spring up to serve nascent middle classes with new products and services designed to meet local consumers’ needs.

In this sense, countries experiencing high growth can lay the foundations for companies serving their populations to grow quickly too.

Developed economies can rarely offer this opportunity for growth on a similar scale or timeframe. But with that opportunity comes risk. It’s easy to fall into the trap of thinking every new emerging market company will be the next Alibaba or Tencent but the reality is most won’t. And the gap between the haves and have nots can be considerable.

This is the risk investors take in emerging markets.

Are all emerging markets the same?

Investors get a fairly clear idea of what distinct opportunities and challenges face the likes of the UK, US and Europe but emerging economies tend to get lumped in together.

That means it’s difficult to put your finger on the separate characteristics on show. There may be shared traits like rising middle classes, better access to healthcare or changing diets but there can be very real differences between countries in the EM bucket.

It’s hard to see how useful it is to compare the likes of China, Brazil and India and conclude they’re similar enough to be talked about as one homogenous group.

Taking the EM label at face value only allows a superficial top-down view of economies and markets which are ‘developing’ and misses the individual stock stories playing out on the ground in these nations.

That part is so important as these companies can often be the driving force behind the entire index, with a long tail of less explosive firms holding them back.

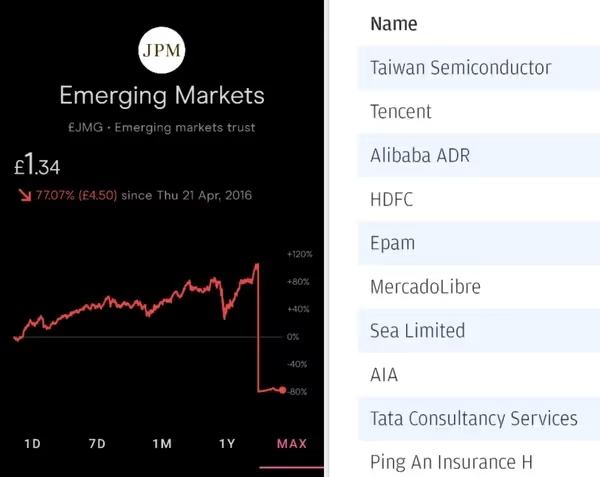

We tend to get those stories from some of the bigger country constituents and hear about the big names like Taiwan Semiconductors and Samsung but we can end up missing the winners further down the index as they pale in comparison.

This can prevent meaningful diversification for investors, as huge conglomerates and individual countries can end up dominating the index.

Is it good to invest in emerging markets?

With an incredible selection of companies and demographics to benefit from, sometimes investors forget to keep in mind the fact that certain economies are not yet ‘developed’ for a reason.

Poor corporate governance, political instability, underdeveloped legal systems and things like low infrastructure spending can be hallmarks of emerging economies.

Corruption in local government has been a huge target for China’s president Xi Jinping and when scandals like Brazil’s Petrobras debacle pop up it gets a bit clearer how that shift from developing to developed can have real hitches.

That’s not to say developed nations like the US or UK don’t have their problems but hopefully the legal systems and governance practices are enough to prevent or dissuade the likes of large scale corruption.

That said, it seems strange for investors to ignore some of the biggest global markets in their portfolios. China makes up nearly 5% of the MSCI All Countries World Index, more than the UK’s 4%.

If we are trying to avoid home bias, we should think about how we are representing good geographical diversification and try not to focus on the firms on home soil.

Active vs passive: emerging market equities

There are options for investors looking for broad exposure to emerging market economies like the iShares MSCI Emerging Markets ETF. Some investors only want passive funds so type of fund could fit the bill.

The country weightings won’t suit everyone though. It might be that you actually want much more exposure to opportunities in China or, if you already have China well-represented in your portfolio, holding an ETF with over a third of its assets allocated to the country might not be attractive.

Or you may want the opportunity to identify the winners among the vast array of EM firms and, just as important, leave out the laggards.

If that sounds like what you’re after, here are three emerging market investment trusts on Freetrade with stock pickers at the helm. None of this is intended to be investment advice or an inducement to buy or sell any security.

It’s just an illustration of how these managers run their investment trusts. This should not be read as personal investment advice and individual investors should make their own decisions or seek independent advice.

Fundsmith Emerging Equities Trust (FEET)

Trust managers Michael O’Brien and Sandip Patodia took the reins of the Fundsmith Emerging Equities portfolio around 18 months ago but their predecessor’s fingerprints are firmly etched into the objective of the fund.

Company founder Terry Smith launched the trust in 2014 with the intention of applying his tried and tested approach to investing in global quality companies to emerging markets.

O’Brien and Patodia try to identify and invest in companies making their money through a large number of everyday, repeat, relatively predictable transactions.

They focus almost exclusively on consumer stocks and prioritise companies set to benefit from a rise in consumption in developing economies.

They avoid financials and cyclical sectors like construction and manufacturing, utilities, resources and transport. Instead, they prefer firms with relatively predictable revenues and strong market positions, often thanks to leading brands, trademarks and distribution networks.

A couple of shining lights in the trust over the past year have been the Amazon of Latin America, MercadoLibre and Foshan Haitian, the world’s largest soy sauce maker.

Latin America is the world’s fastest growing region for e-commerce - a point reflected in the trust as MercadoLibre takes top spot.

The company is still in loss-making mode for now but grew its net revenues by 148.5% year-on-year to $1.3bn in the fourth quarter of 2020. Its active user base grew by 71.3% to 74m, as the firm seeks to cement the kind of dominance the managers look for.

Foshan Haitian’s simple business model and leading presence in its sector are hallmarks of the Fundsmith approach. The company aims to hoover up market share in the Chinese condiment sector through strong brand recognition and attention to developing a reputation for quality and reliability.

Fidelity China Special Situations Plc (FCSS)

Fidelity China Special Situations manager Dale Nichols is another investor with an eye on the consumer story in emerging markets. His hunting ground is China, where his focus on companies contributing to the country’s growth often takes him towards some lesser-known, unlisted or small cap names.

Nichols takes full advantage of the ability of investment trusts to hold private companies. He believes the pre-IPO space offers the opportunity to be a part of some of the country’s most innovative and entrepreneurial companies. As a long-term investor, he is happy to stick with them from private to public markets.

This is one area where investment trusts can add value. Given the lack of access to private markets available to everyday investors, having a strong bottom-up research team who can talk to company management and appraise investment ideas can be useful.

The manager sees a big opportunity in China’s post-pandemic recovery. And despite a general global shift online, Nichols sees the trend towards fintech and e-commerce happening quicker and more efficiently there than anywhere else. Alibaba and Tencent typify this thought process.

The rise of China’s middle class is also a central theme to the trust. Nichols expects wealth management, insurance and travel services to be long-term beneficiaries of this demographic shift.

This is reflected in the fund through the likes of Ping An and China Pacific Insurance.

JPMorgan Emerging Markets Investment Trust

JPMorgan Emerging Markets manager Austin Forey looks for high quality emerging market companies with the ability to deliver sustainable long-term returns. Forey has been at the helm for 27 years and has benefited, particularly in the past 10 years, as high quality companies with good growth characteristics have outperformed so-called value stocks.

The manager’s commitment to investing in companies with strong earnings growth comes through in the portfolio, with many of the top names now ubiquitous among emerging market investors.

That resilience was tested in 2020 but the trust is now back above pre-pandemic levels. The chart might cause a few palpitations but worry not, it’s simply the result of a 10:1 stock split in November 2020.

For Forey and Co. fretting over near-term hurdles like US-China relations, falling earnings and currency weakness risks obscuring medium to longer-term thinking.

Instead, the manager reaffirms his commitment to evidence-based stock selection, targeting strong fundamentals and long-term growth potential.

Being able to navigate emerging markets and deal with the volatility they can bring can be another reason investors turn to investment trusts run by experienced managers.

JPM investment specialist Emily Whiting explains, “The minute all these analysts and portfolio managers move into EM they get absolutely shocked by double-digit declines in a day, which we’re quite hardened to. Thankfully they’re not too frequent but the increased volatility comes as part of the asset class.”

That ability to stay composed and keep an eye on the big picture is key to the process.

Whiting says, “There are times the market will sell down everything in a country just because of the country it’s in. But if you believe that you’ve bought good quality businesses, if you trust their management, if they have a robust balance sheet, and if they have a superior product – then, sitting on your hands is the best course of action.”

For Whiting, it goes back to recognising that there is opportunity in diversity and that starts with acknowledging how diverse the EM label really is.

She explains, “Out of any asset class the breadth and the cultural differences across emerging markets make it so important not to just be sat behind a Bloomberg terminal looking at numbers. Having people on the ground in the likes of Shanghai and Taipei means we see first-hand the pick-up in traffic, or queues for restaurants again.”

Freetrade is on a mission to get everyone investing. Whether you’re just starting out or have plenty of experience, you can buy and sell hundreds of investment trusts commission-free on our stock trading platform. Before investing, look at the most traded shares on the platform to see which investment trusts are the most popular with our clients.

This should not be read as personal investment advice and individual investors should make their own decisions or seek independent advice. This article has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is considered a marketing communication.When you invest, your capital is at risk. The value of your portfolio can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future results.Freetrade is a trading name of Freetrade Limited, which is a member firm of the London Stock Exchange and is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales (no. 09797821).

.avif)