You can think of tax relief as money that would have gone to the taxman, but instead goes towards building your pension.

In this guide, you’ll find everything you need to know about tax relief on pension contributions and how it can boost your pension pot.

What is pension tax relief and how does it work?

For most of us, each time we pay into our pension (known as a pension contribution), the government adds money too. This is called tax relief, and it’s one of the key reasons opening a pension can be so beneficial.

How does pension tax relief work? A full guide

When it comes to getting tax relief on pension contributions, there are a few key things you need to know.

How much money can you put in a pension?

How much you can contribute depends on your annual income, and is called an “annual allowance”.

Annual allowances vary, based on factors like your income. Below is a list of different pension annual allowances.

Low or no-income earners

If you earn less than £3,600 or have no earnings, the most you can put in your pension and get tax relief on is £2,880 a year (that’s £3,600 after tax relief has been added).

Standard annual allowance

This allowance applies to most people. With the standard annual allowance, you can put up to 100% of your annual earnings or £60,000 (whichever is less) each year into a pension.

If your annual earnings are £36,000, you can add up to £36,000 into pensions that year with tax relief.

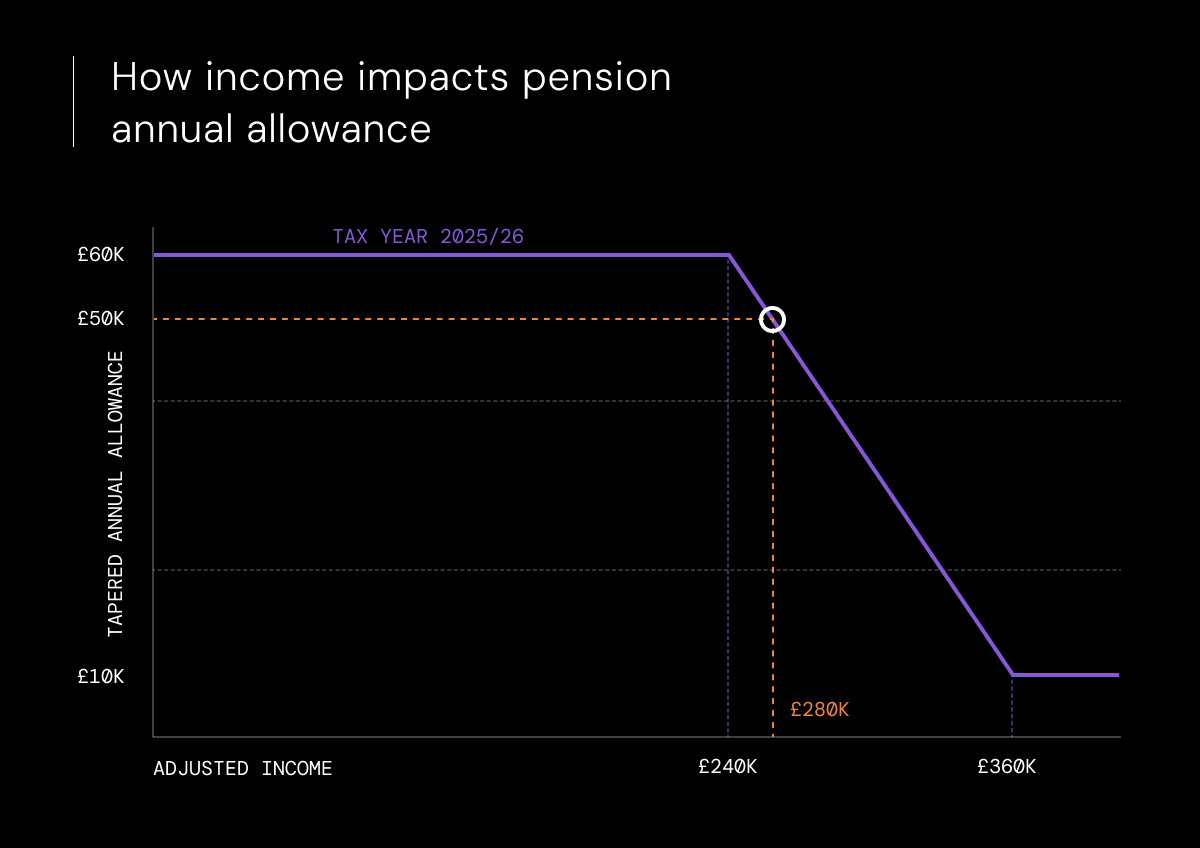

Annual allowance for high earners

A high earner is someone who has a ‘threshold income’ of above £200,000 and an ‘adjusted income’ of over £260,000. If you think you might fall into this category, you can work out your tapered annual allowance.

If you meet the above criteria, your annual allowance will drop by £1 for every £2 of adjusted income over £260,000, down to a minimum of £10,000.

For example, if you have a threshold income above £200,000 and your adjusted annual income is £280,000, your annual allowance will be reduced by £10,000 to £50,000.

Money purchase annual allowance

If you’ve already started taking money from a defined contribution pension pot, you will have likely triggered the Money Purchase Annual Allowance (MPAA). After this has been triggered, your annual allowance will be capped at £10,000.

What happens if you exceed the annual allowance?

If your pension contributions go above the amount allowed by your annual allowance, you could face a personal tax charge at your highest marginal rate of income tax.

You pay this to HMRC by declaring any excess contributions on your self-assessment tax return.

How much tax relief do you get on pension contributions?

How much tax relief you get depends on the rate of income tax you pay.

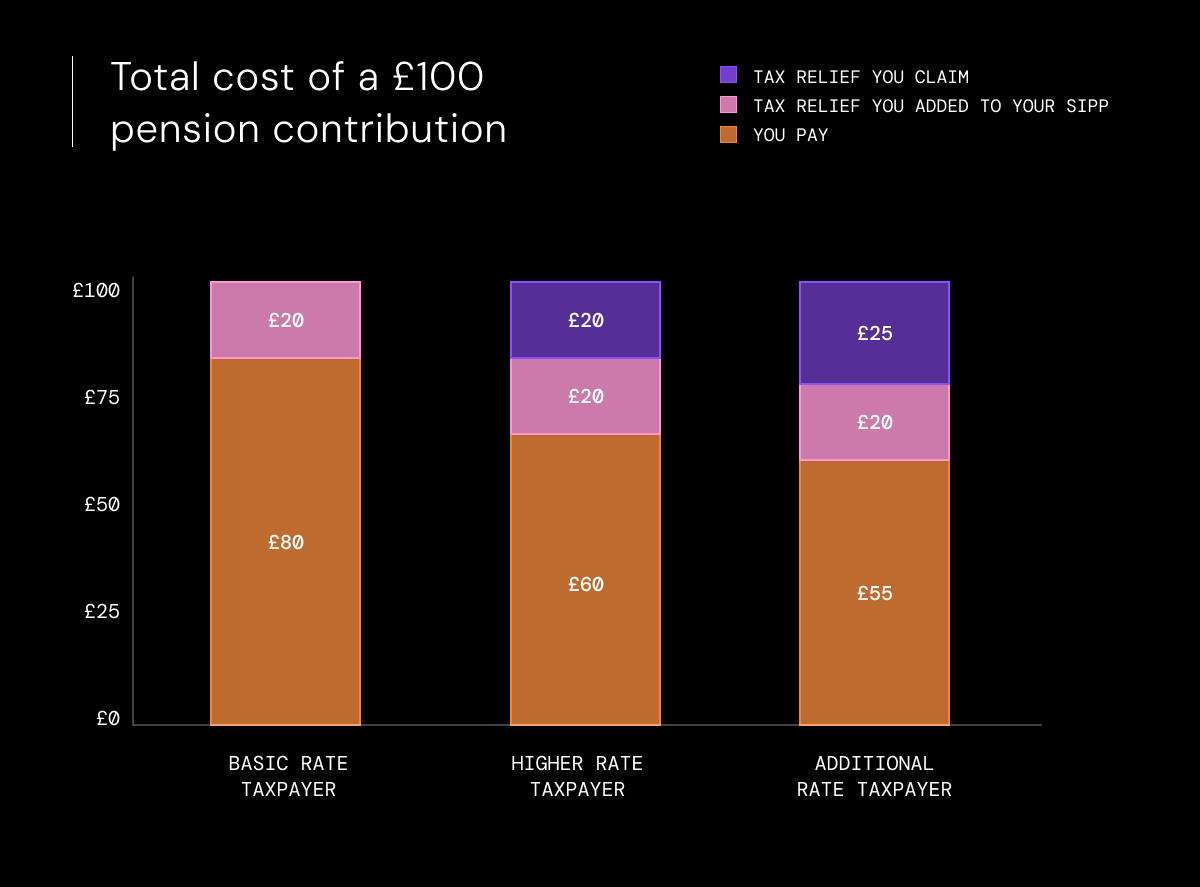

Most people in the UK are basic rate taxpayers. This means they earn less than £50,270 (bands differ in Scotland), so pay 20% income tax on these earnings. This means any tax relief is also at 20%.

.png)

As we saw with the annual allowance for low or no earners, the Government gives basic rate tax relief on all pension contributions up to a certain amount, regardless of whether you pay tax or not.

And if you pay more than the basic rate of tax, then you’ll be able to claim further tax relief yourself.

For example, if you pay tax at say 45%, you may be able to claim an extra 25% in tax relief. That brings total tax relief to £45 and means a £100 pension contribution only costs you £55.

How do I get my pension tax relief?

The good news is that usually you won’t have to do anything to get basic rate (20%) tax relief. It will happen automatically.

There are two main ways to get tax relief: relief at source and net pay.

For a personal pension, the relief at source method is always used.

For a workplace pension, your employer chooses which of these two methods is used.

If you are not sure what you have, read Freetrade’s guide to different types of pension.

What is relief at source?

With a personal pension, any payments you make to your pension will be made using your after-tax pay. So higher and additional rate taxpayers may need to claim back tax relief from the government.

With a private pension, such as a Freetrade Self Invested Personal Pension (SIPP) account, basic rate tax relief (20%) is automatically claimed and added to your SIPP account after each contribution.

If you pay tax at a higher than the basic rate than this, you will likely be able to claim extra tax relief by completing an annual self-assessment tax return and confirming any pension contributions.

What is the net pay method?

With net pay, your pension contribution is taken from your pay before you’ve paid any income tax and before it’s paid out to you.

This way, you get full tax relief at this time and don’t pay any tax on these earnings.

Maximising your allowances: The carry forward rule

The carry forward rule allows you to add more than the annual allowance (currently £60,000) to your pension in a year while avoiding the annual allowance charge.

As long as you have not triggered the MPAA, you can do this by carrying forward unused allowances from the previous three tax years.

.webp)

.avif)