Average pension growth in the UK is a minefield, because growth depends on how your pension is invested, how much you contribute, and what markets do.

Even then, we have to separate out investment return from overall growth. Let’s explore key drivers, recent UK benchmarks, and how to estimate your pension pot’s growth.

What is average pension growth?

Average pension growth rates are hard to nail down because portfolios grow at different speeds depending on factors like market conditions and asset mix.

It’s also important to understand the difference between investment return and overall growth.

The former simply accounts for the increase in value of assets held within a pension pot, while the latter accounts for investment growth AND contributions.

According to data from The Pensions Regulator, assets per defined contribution (DC) member increased by 17% between 2023 and 2024.

This is an example of a rough image of overall growth, including the impact of contributions and investment performance. However, the figure is also impacted by new members joining and people leaving the scheme.

Looking at investment returns offers a different picture.

Figures from the Department for Work and Pensions’ Pension Provider Survey 2024/25 show gross annualised investment growth for the largest default funds over the prior five years was 8.6% for savers with 30 years to retirement.

This dropped to 3.6% for those with five years to retirement and 3.0% at retirement.

Freetrade users’ mean average annual returns from Self-Invested Personal Pensions (SIPPs) were around 9% in 2025, and have exceeded 12% in the past. Past performance is not a reliable indicator of future returns.

Average pension growth over the last 5 years

According to CAPAdata, the performance of default funds of the UK's biggest DC workplace pension providers averaged a 9.3% annualised return for young savers over the last five years. Young savers are defined as those 30 years from the state pension age.

Pre-retirement pots, defined as those within five years of state pension age, achieved a 6.1% annualised return.

Investment growth depends on distance to retirement. This is because of changes in how pensions tend to be invested as you age.

How are pensions invested?

A workplace DC pension pot is usually pooled with many other pots and invested in a variety of assets. The performance of these investments impacts the growth of your pot.

Typically, your pension will be invested in a default fund.

This is a basket of investments, such as shares, bonds, and ETFs, selected by your pension provider. It is usually highly diversified, and may include so-called “lifestyling” features to ensure the asset mix and risk level are appropriate for someone of your age.

When you are younger, it will be weighted heavily towards higher risk investments like equities. As you near retirement, and there is less time for bumps in the market to be smoothed out, your portfolio will become more heavily filled with lower risk investments like bonds.

You do not have to stick with a default fund. With most pensions, you may be able to choose between a selection of alternatives.

With a SIPP, you can access even greater choice. Freetrade’s SIPP allows you to pick from over 7,000 different investments.

Levels of investment risk and pension growth

Different levels of investment risk influence your pension pot’s growth. Pension pots weighted heavily toward high-risk investments like stocks tend to have higher long-term growth potential, but are more likely to experience bigger ups and downs.

Lower-risk approaches, which might focus more on bonds or cash, tend to be steadier but offer lower expected growth.

This is why funds with “lifestying” or target date features do something called “de-risking”. They will typically reduce exposure to higher-risk assets as you near retirement. This might reduce annual returns but it can protect your retirement portfolio from volatility.

Learn more with Freetrade’s guide to investment risk.

What affects pension growth?

- Contributions: Increasing your contributions and ensuring you are maximising employer contributions should increase growth.

- Investments: The performance of the assets in your pot, and the asset mix of your portfolio, make an enormous difference to growth.

- Fees: Most providers charge fees, like an annual management fee or a platform fee. They might seem small, but they can add up over decades.

- Time: The longer you leave your pension pot, the more time it will have to increase in value. Contributions stack up and compounding accelerates growth.

How to maximise the value of your pension

- Employer contributions: Are you taking full advantage of employer contributions? As a minimum, employers must match employee contributions up to 3%, but some employers will contribute even more. Check with your employer to see how much they can contribute.

- Claiming tax relief: Are you claiming the full amount of tax relief you are entitled to? If your pension scheme uses the relief at source method, you could be entitled to claim more tax relief through a self-assessment tax return. Check Freetrade’s guide to pension tax relief for more information.

- Check fees: High fees can limit pension growth, or even erode value over time.

- Combine pots: Tracking down and combining pensions can boost your retirement. You might find lost pots, exert more control, or save on fees.

- Check your investments: If your investments fail to deliver growth, you might end up with a smaller pension than you hoped for. If you are not satisfied with how your pension is performing, seizing control by opening a SIPP could help you to turn things around.

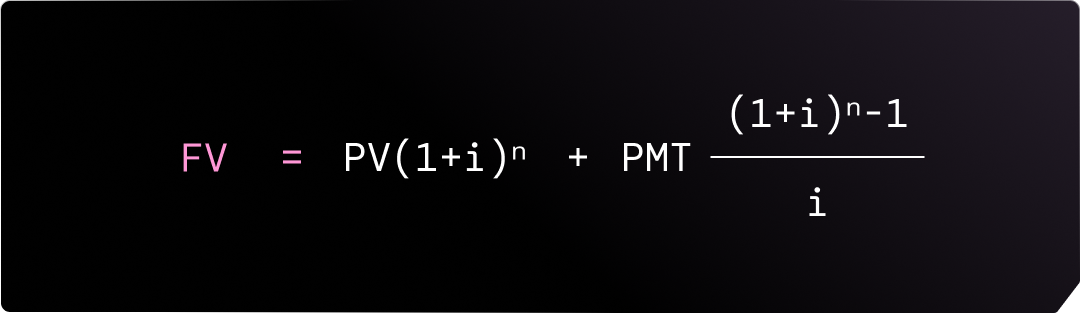

How to estimate your own pension growth

Your pension provider may provide projections and illustrations of how your pot could grow over time. Make sure to check statements or log in online for this information.

You can also manually estimate pension growth. First, establish:

- your current pot (PV)

- monthly contributions (PMT)

- months until retirement (n)

- expected effective annual return after fees (r)

- monthly rate (i)

This last figure is simply your expected effective annual return after fees (r) divided by 12.

Plug these values into this formula:

Here’s an example.

- Current pot: £50,000

- Monthly contribution: £200

- Time until retirement: 20 years (240 months)

- Annual return after fees: 5% (0.05)

Now we can plug these numbers into the formula, like this:

The figure obtained is your projected pension pot.

Remember to consider the impact of inflation and to test multiple annual return assumptions.

For more information about checking in on your pension and ways to manage your pot, explore Freetrade’s guide to pension underperformance.

.webp)