Coffee gets a bad rap in the world of stocks and shares ISAs. I think that's a bit unfair though.

And it's not because I don't see the point the personal finance commentators are getting at. Spending less on the shop-bought luxuries and investing more in an ISA is a no-brainer for a lot of eager savers.

It's just that this particular conversation always ends with a point about how we could all retire earlier or buy a house if only we had a bit more self-restraint or a better morning routine.

Read more:

ISA vs cash savings account

What is a stocks and shares ISA?

Cash ISA vs stocks and shares ISA

That part always feels a bit hard to place. Is it condescending? Is it even realistic? Why am I being scolded over £2.50?

So, fuelled by quite a lovely shop-bought flat white, I thought we'd see if I'm getting rubbed up the wrong way for no reason, and caffeine aside, where the overall message behind the coffee hate might lie.

Can homemade coffee make you a millionaire?

OK, let's pull off the plaster.

What if you did give up your shop-bought coffee altogether? Well, if a Starbucks flat white is £2.50, saving on 250 of those (a general working year) would pocket you £625.

If you were to redirect that expense into your stocks and shares ISA for 10 years you'd put away £6,250. If you achieve an annual 5% return you'd end up with £7,463.32.

That takes into account a £4.99 monthly fee for the Freetrade Standard plan which includes your stocks and shares ISA but assumes no further charges. If you invest in foreign shares, ETFs or investment trusts they'll have their own fees on top. It also assumes steady market performance which is in no way a certainty - we're just using it as an illustration.

Now, that's not to be sniffed at and it does go to show how a simple change in expenditure can have a big impact.

Read more:

Your pocket guide to ISAs

2023 ISA income investing

The (more realistic) ISA millionaire

...But why coffee? There are much more outlandish expenditures we could surely forego.

Sports bras, meat-free sausages and pet collars were all included in the CPI inflation basket this tax year due to their popularity but we aren't inundated with messages around the financial perils of veggie bangers or pampered pooches.

It's got a ‘hey fellow kids' ring to it, especially when there are normally a few nods to avocado on toast thrown in for good luck.

So there's a glaring finger being pointed at anyone under 40 here. And with that comes the nagging perception that everyone queueing in Costa is just hopeless at managing their personal finances.

So, while the intentions of praising frugality might be there, culturally it's wide of the mark.

There are other pressing money issues to tackle. Our Great British Financial Literacy Test highlighted the need for us to talk about more than skipping the café on the way to work.

Read more:

Dividends and your stocks and shares ISA

How to find the best and cheapest stocks and shares ISA

Choosing the right investment account: GIA or ISA?

In it, 88% of respondents from around the UK said they didn't feel confident in their financial literacy, with one third saying their mental health has suffered as a result.

91% of participants told us they lack confidence in investing in general, with 88% saying they weren't as confident as they'd like to be when it comes to ISAs.

Just under a quarter of the cohort didn't know the annual ISA allowance (23%) and 37% of people didn't know what ISA stands for.

So, we need help. And maybe the coffee hook is just a conversation starter.

In this sense it's just a short-hand example of a simple, low-cost repeat purchase that we take no notice of, but that racks up over time.

And that's actually where I can start to get behind the intention here.

Forget the coffee, think bigger

It can be enormously encouraging to see what those small investments could be worth in the future thanks to the value of time and compound interest. It can make it all feel a lot more worthwhile, especially for smaller savers.

For example, if you were to put away £100 every month over 10 years, achieving a 5% annual return over the period, you could end up with £15,057.32. Up it to £200 and that could grow to £30,905.47. Again, both of these are just illustrations and factor in the Freetrade Standard plan fee which includes your ISA. Other charges may apply like foreign exchange fees for non-UK stocks, or ongoing fees for ETFs and investment trusts.

But we shouldn't guess that young people are frittering away their money instead of doing their best with it. And who's to say that a vanilla latte in the morning isn't the only treat you should allow yourself amid an otherwise strict savings plan?

Don’t fall into resenting investing

The broader message of constantly denying ourselves something in order to fund a later lifestyle also risks making us resent our investing habits when really we should be looking forward to helping fund our future financial goals.

There's also a real danger that ISA savers shunning their morning cuppa think that's all they need to do and it's only a matter of time before they hit seven figures.

But it's not the empty mug where the latte should be that's going to automatically make you an ISA millionaire.

Focus on developing good investing habits

There have to be much better investing patterns built into our habits - ones that feel unintrusive, easy and repeatable.

The amount we can realistically afford to invest will ebb and flow with our lifestyles, our salaries and the financial commitments that life brings us.

It's much more important to focus on creating a good mindset around investing than pinpointing a daily figure to put away.

Here are four things to think about, away from the amount you actually choose to invest.

- Invest regularly and robotically, in a way that suits your budget. Consistent investors take advantage of the glorious magic of compounding returns over time. If you are saving up cash on the sidelines, waiting to jump into the market, you are depriving your money of that snowball effect. Timing the market is also notoriously difficult, let time in the market do the work instead. Setting up a recurring order on your Freetrade app can help you out here.

- Diversify and get an asset mix that works for your goals. Make sure your time horizon, tolerance for investment risk, and ultimate financial goals are informing the assets in your portfolio. When the asset balance fits, spread your money over a blend of assets and geographies.

- Keep learning. Investing is a funny business. The more you learn, the more you realise there is left to explore. Always try to be a better investor and keep up to date with the market with resources designed to take the jargon out of it all.

- Remember, it's your journey, no-one else's. Comparison is the thief of joy. It's also the cause of most anxiety when it comes to money. Yardsticks around what pension savings you might want to have at certain ages are just that - rules of thumb. They don't take into account your unique needs and wants. So personalise your budget and your investments. If that means there's room for a coffee stop on the way to work, grab that latté with a smile.

2023 investment tax allowances: ISAs just got real

With those habits in mind, there's another reason why your stocks and shares ISA is now even more important.

In November, the chancellor laid out clear plans to raise tax on investment gains and 2023 is when it all kicks off.

The amount we can earn in dividend income and outright investment growth (capital gains) is falling from April 2023. With both allowances being chopped in half, and then again in 2024, it means a lot of investors will pay tax on their investments for the first time.

If you haven’t thought about investing tax efficiently, then, it might be wise to at least work out if a tax-efficient account like a stocks and shares ISA could help now more than ever.

Eligibility to invest into an ISA and the value of tax savings both depend on personal circumstances and all tax rules may change.

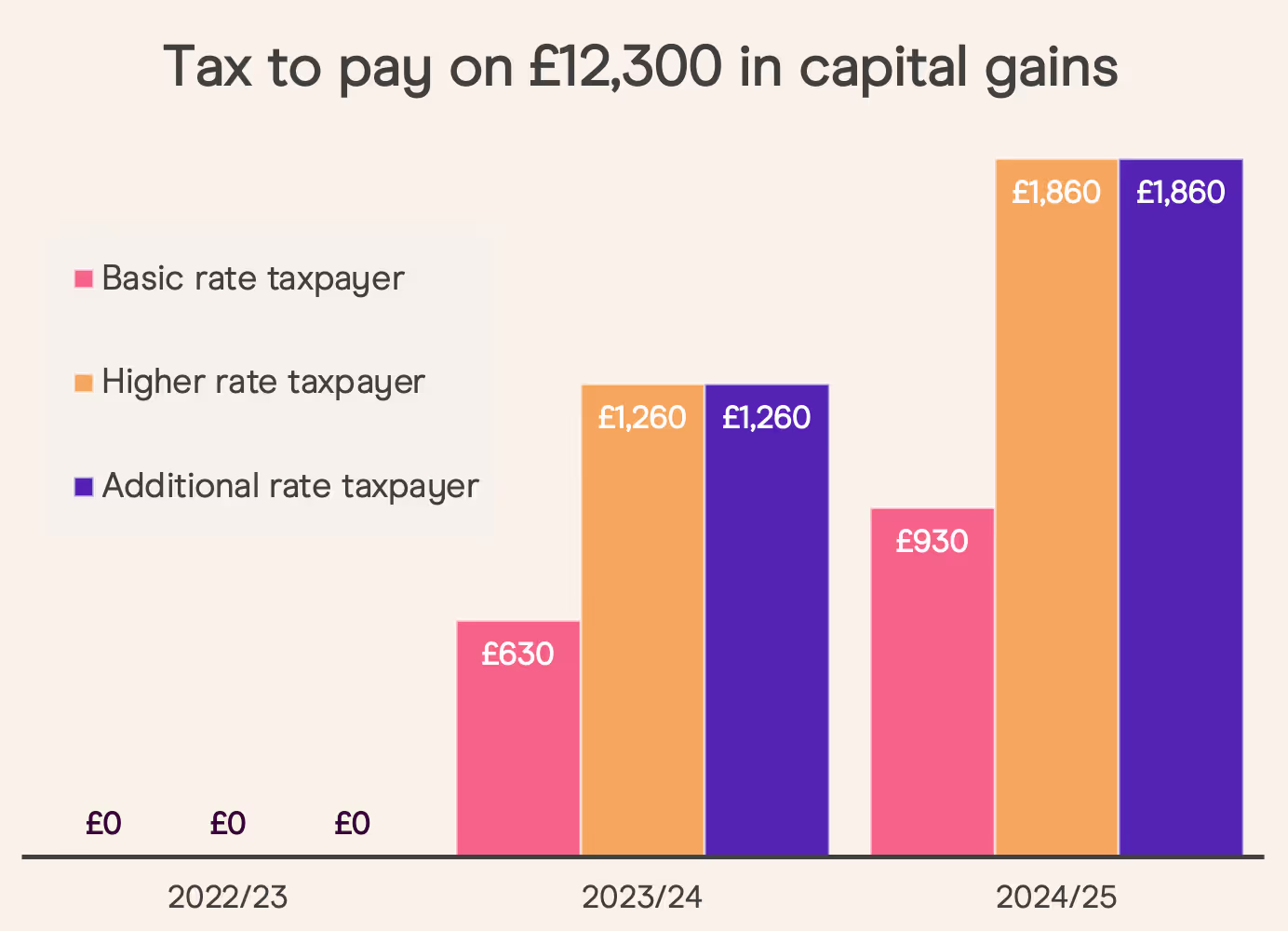

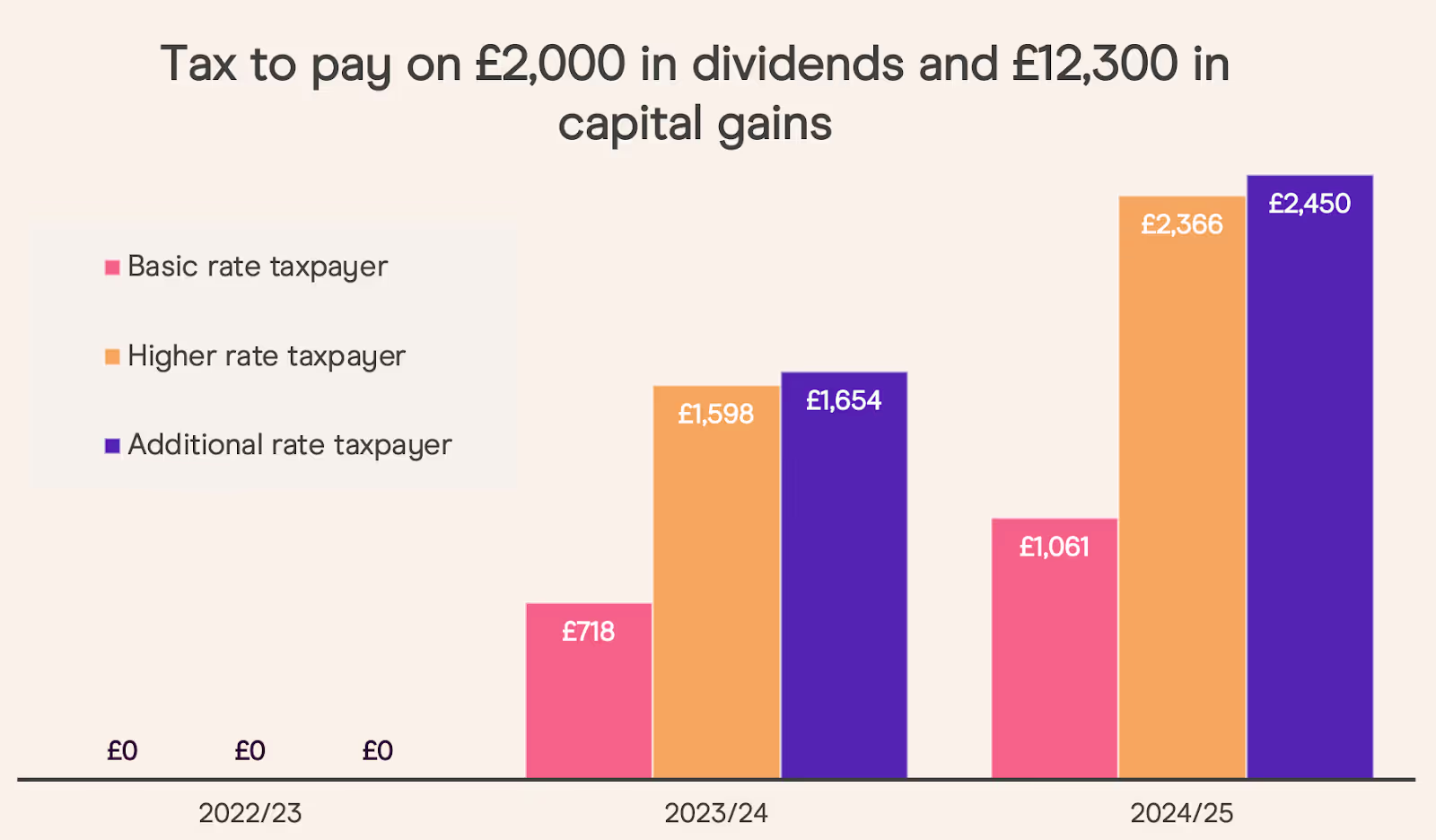

2023/24 dividend and capital gains allowances

If you aren’t investing using a stocks and shares ISA or a longer-term tax-efficient account like a SIPP, you could be forking out a load of extra tax come April.

Often, investors will opt for the cheapest investment account out there and on the surface that makes sense. Why pay more than you have to? But investing solely in a general investment account (GIA) because it has a lower headline cost than an ISA risks missing the whole point, tax.

Now, it may be that you’ve decided you’re unlikely to go above your personal investment tax allowances. In which case, it’s probably true that an ISA wouldn’t be as useful. But, given those allowances are coming down fast (see the chart above) it’s maybe worth revisiting those assumptions.

New UK dividend tax rates from April 2023

Putting the changes to the dividend allowance into perspective, a basic rate taxpayer earning £2,000 in dividends in the 2022/23 tax year, and earning the same dividend income for the next two years, would suddenly have to pay £87.50 in 2023/24, then £131.25 in 2024/2025.

The rise in dividend tax is even more pronounced for higher rate taxpayers, who would pay £506.25 in 2024/25, and additional rate taxpayers, who’d owe £590.25.

That’s a big chunk of change for anyone, and let’s not forget it could be even bigger if your dividend payments grow, like we all hope they do.

New UK capital gains tax rates from April 2023

Dividend allowances aren’t the only limits getting the chop in the 2023/24 tax year. The amount we can earn from the growth of our assets and not pay UK tax each year (your capital gains tax allowance) is also falling from £12,300. First, to £6,000, then to £3,000 the year after.

Of course, if you don’t sell any assets it doesn’t matter all that much right now. But eventually we all want to hit the sell button and actually put that money to use. And it’s at that point that we’ll potentially have to pay tax on any gains we’ve made.

The thing is, making all that hopeful growth tax efficient needs to start long before you actually sell up and move on. If you get to that stage, the last thing you want is to be kicking yourself just because you didn’t use the most tax-efficient account to begin with.

Get planning for lower allowances and higher tax rates

It’s even more important to lend a thought to tax efficiencies when you consider the route most of us want to take is into the higher tax bands at some stage in our working lives. With that prospective rise in salary and tax rate comes a rise in dividend and capital gains tax rate too.

For example, going from being a basic rate taxpayer to being a higher rate taxpayer means potentially paying 33.75% instead of 8.75% on dividends above the allowance.

That’s even more of an issue for the UK’s highest earners from April 2023 as the additional rate income tax threshold will come down from £150,000 to £125,140. Granted, this bunch might not get a whole lot of sympathy from the rest of the nation’s savers and investors.

Read more:

Dividends and your stocks and shares ISA

Choosing the right investment account: GIA or ISA?

But the fact remains that anyone tipping the scales above £125,140 will suddenly find themselves in a 45% income tax band, a 39.35% dividend tax rate, 20% in capital gains tax and staring down the barrel of two successive reductions in investment tax allowances.

Get ISA ready

All of these hits to what investors can earn before tax kicks in mean it’s just got even more important that we make our money as tax efficient as possible. That might mean looking beyond what our current investment gains and dividend income look like, and planning for what could come down the line.

It’s a harsh reality that a lot of investors investing outside of an ISA will eventually have to stump up tax payments eventually, when they could have just used an ISA instead.

It’s still important to make sure an ISA is right for you though. It could be that you genuinely get nowhere near these allowances or tax thresholds and never plan to. But that’s often the thing with investing. Compounding small amounts and incremental contributions over the years can really build up the snowball effect that good investing is based on.

Whichever way you go, deciding if an ISA suits you or not is at least worth the peace of mind right now.

Protect your investments from UK tax with tax-efficient investing accounts like a stocks and shares ISA or a SIPP. Check out the ins and outs of both accounts before opening one. Take a look at what is a stocks and shares ISA and what is a SIPP. We summed up the key differences in our SIPP vs ISA guide.

Important information on SIPPs

SIPPs are a pension product designed for people who want to make their own investment decisions. You can normally only access the money from age 55 (set to rise to 57 from 6 April 2028).

Before transferring a pension you should ensure you will not lose valuable guarantees or incur excessive transfer penalties. Pensions are usually transferred as cash so you will be out of the market for a period.

Freetrade does not currently offer drawdown products for our SIPP.

This should not be read as personal investment advice and individual investors should make their own decisions or seek independent advice. This article has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is considered a marketing communication.When you invest, your capital is at risk. The value of your portfolio can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future results.