The spotlight is shining on a trio of major AI infrastructure players, with Palantir, AMD, and Arm in focus this week due to earnings updates.

Find out how Palantir performed in their earnings report, as well as what to expect from semiconductor industry players AMD and Arm who report later in the week.

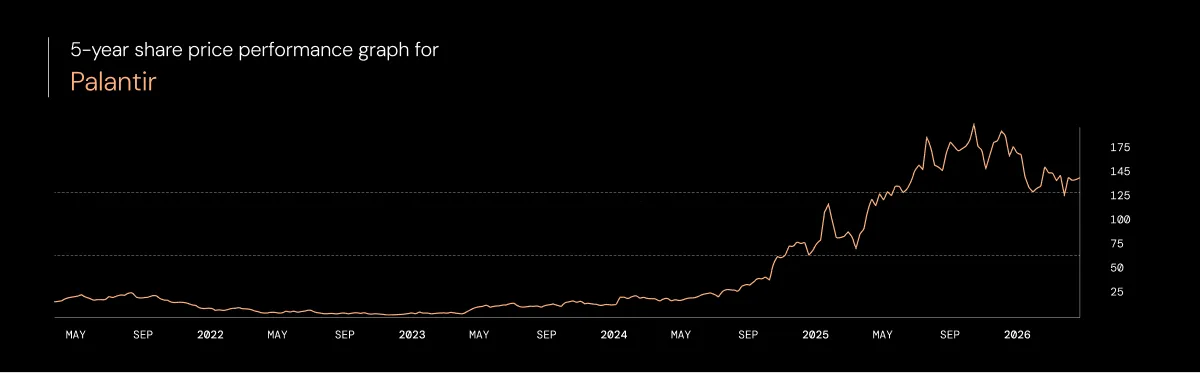

Palantir - Earnings review

Palantir’s Q1 earnings landed after market close on Monday.

The data analytics firm’s AI-powered software is designed to help clients integrate, analyse, and act on massive or complex datasets.

Quarterly revenue beat expectations as it rose by 85% YoY to $1.63bn. In addition, adjusted operating margins widened to 60% from 44% in the same period 12 months prior.

US revenues more than doubled, climbing by 104% YoY to $1.28bn. Commercial revenues from the market were up by 133%, while Government contract revenue rose by 84%.

The US is Palantir’s lifeblood and focus, accounting for 79% of Q1 revenue as CEO Alex Karp emphasised the business’s aim of strengthening US national security.

Karp was also extremely bullish in his assessment of the company’s prospects, commenting:

“To be clear, our US business more than doubled in twelve months. The growth rate of many businesses tends to slow down, to ease, as they scale within their markets. Ours has not. And the twin pistons of our US business are now firing in sync.”

The company’s outlook reflected Karp’s optimism. It hiked FY revenue guidance to $7.65-$7.66bn amid higher expected income from US commercial clients as the company sees the market accelerating.

The share price reaction tells its own story, though. Despite a consensus expectations beat, raised guidance, and confidence from leadership, PLTR’s share price dipped by over 3% in pre-market trading following the release.

The business is in the vanguard of an AI revolution which has swept investors along. Like many competitors, its valuation appears stretched with a P/E ratio sitting in the hundreds.

The business might be smashing all sorts of metrics, but, in a space where valuations appear to be becoming increasingly divorced from fundamentals, can Palantir live up to investors’ hype?

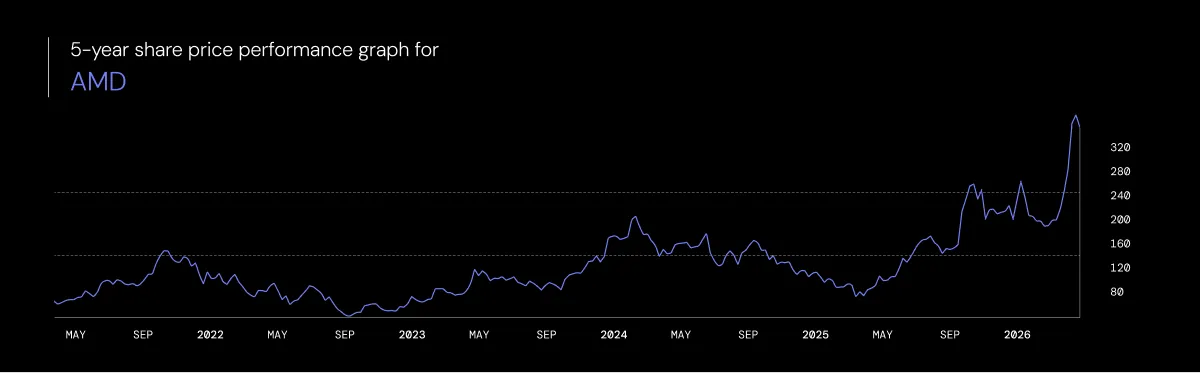

AMD - Earnings preview

AMD’s Q1 earnings are due on Tuesday evening, after market close in the US.

Consensus expectations have the chipmaker’s revenue pegged at $9.91bn and quarterly earnings per share (EPS) at $1.29.

In its own guidance, AMD flagged Q1 revenue at between $9.5-$10.1bn. The company also anticipated Q1 to show a YoY gross margin expansion from 50% to 55%.

Back in Q4 of FY2025, the business reported 34% YoY revenue growth to $10.27bn and EPS of $1.53.

Its Data Centre segment showed 39% revenue growth to $5.4bn, while the Client and Gaming arm achieved 37% growth to $3.9bn. Gross margins steadily expanded too, rising from 54% to 57% YoY.

Continued strong growth of AMD’s Data Centre segment is key. Huge tech players with deep pockets are pouring massive amounts of capital into AI infrastructure.

An acceleration in Data Centre revenue growth would demonstrate that AMD’s hardware can capture a share of this, particularly if it doesn’t come at the expense of margins.

Looking ahead, investors will want more insight into the MI400 series roadmap, particularly how this next-generation of AI accelerators may offer broad applications for a variety of clients.

For example, its new Instinct MI440X GPU is designed for on-premises deployment. For clients who do not need or cannot afford full rack-scale systems, such a solution may appeal.

Here, the business may be able to carve out a niche in mid-market of data centre builds, an area where the business will hope to out-compete rival Nvidia.

Zooming out and looking at the stock, it appears expectations are high. AMD has had a barnstorming run of late, as its share price has risen by 50% over the YTD.

Can the business turn AI hardware demand into meaningful revenue growth, and does recent share price movement mean that good news is already priced in?

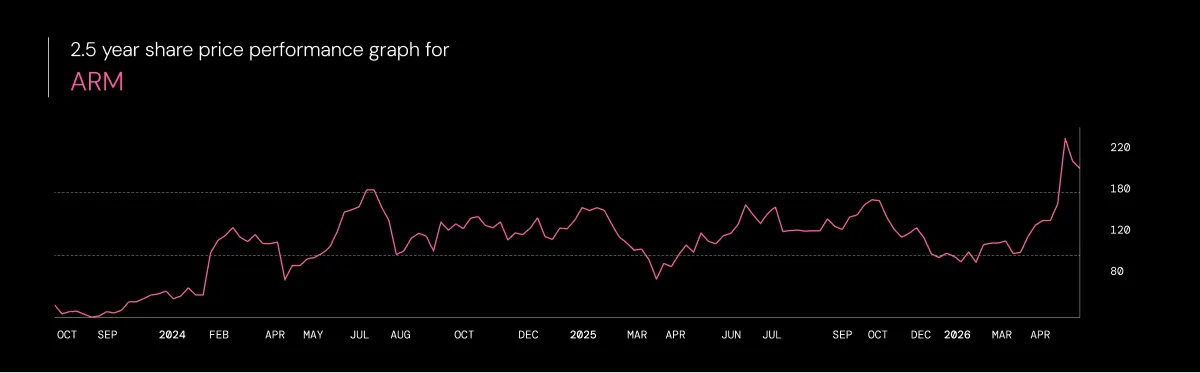

Arm - Earnings preview

Arm reports its Q4 FY2026 results tomorrow after the close.

Wall St is expecting around $1.47bn in revenue and $0.58 in adjusted EPS, almost bang in line with Arm’s guidance, plus or minus $50m, and non-GAAP EPS of around $0.58.

The Cambridge-based chip designer is certainly riding a wave of momentum. Last quarter, revenue rose 26% year-on-year to $1.24bn. Royalty revenue, money earned each time a customer ships a chip or device built on Arm’s designs, hit a record $737m. Licensing revenue, the money Arm gets when customers pay to access its chip designs and architecture, rose 25% year-on-year.

Data centre demand is driving royalties too, as Arm-based CPU cores ripple across cloud and AI infrastructure from names like AWS, Microsoft and Nvidia.

That’s the upside. Now for the headwinds.

Smartphones are a mature market, with global shipments growing in low single digits, and Arm’s technology already powers 99% of them. That could put a dent in growth if handset demand continues to weaken.

There’s also something of a memory drought at the moment. AI data centres need huge amounts of specialist memory, especially high-bandwidth memory, or HBM.

To cash in on that demand, memory makers have shifted capacity and investment toward higher-margin AI memory. That tightens supply for more ordinary DRAM and NAND, the memory used in phones, PCs, servers and storage.

Gartner estimates combined DRAM and SSD prices could rise 130% by the end of 2026.

That is not a direct drag on Arm. Arm does not sell memory. But if memory shortages dampen shipments of Arm-based chips and devices, that means fewer royalty payments.

These headwinds, smartphone saturation and the memory drought, could be offset if more phones use premium chips, newer Armv9 designs or its pre-built Compute Subsystems.

With Arm still trading on a demanding multiple, being ‘good’ may not be good enough. Investors have already pegged Arm as a long-term AI winner.

So, can Arm reach those numbers? And can royalties prove Arm is still earning more from the chips spreading through smartphones, data centres and AI devices?

Capital at risk. The value of your investments can go down as well as up and you may get back less than you invest.

Fluctuations in foreign exchange rates may affect investments denominated in currencies other than GBP and the amount you receive back.

Past performance is not a reliable indicator of future returns.

Freetrade does not give investment advice and you are responsible for making your own investment decisions. If you are unsure about what is right for you, you should seek professional advice.

Always do your own research.

.avif)