.webp)

Among earnings this week, gold mining giant Barrick, semiconductor outfit Applied Materials, and Chinese e-commerce mega-retailer Alibaba all update the market.

Find out how Barrick, Hims & Hers, and AST SpaceMobile performed in their quarterly updates, and read previews of CSCO, BABA, and AMAT, all of which report later in the week.

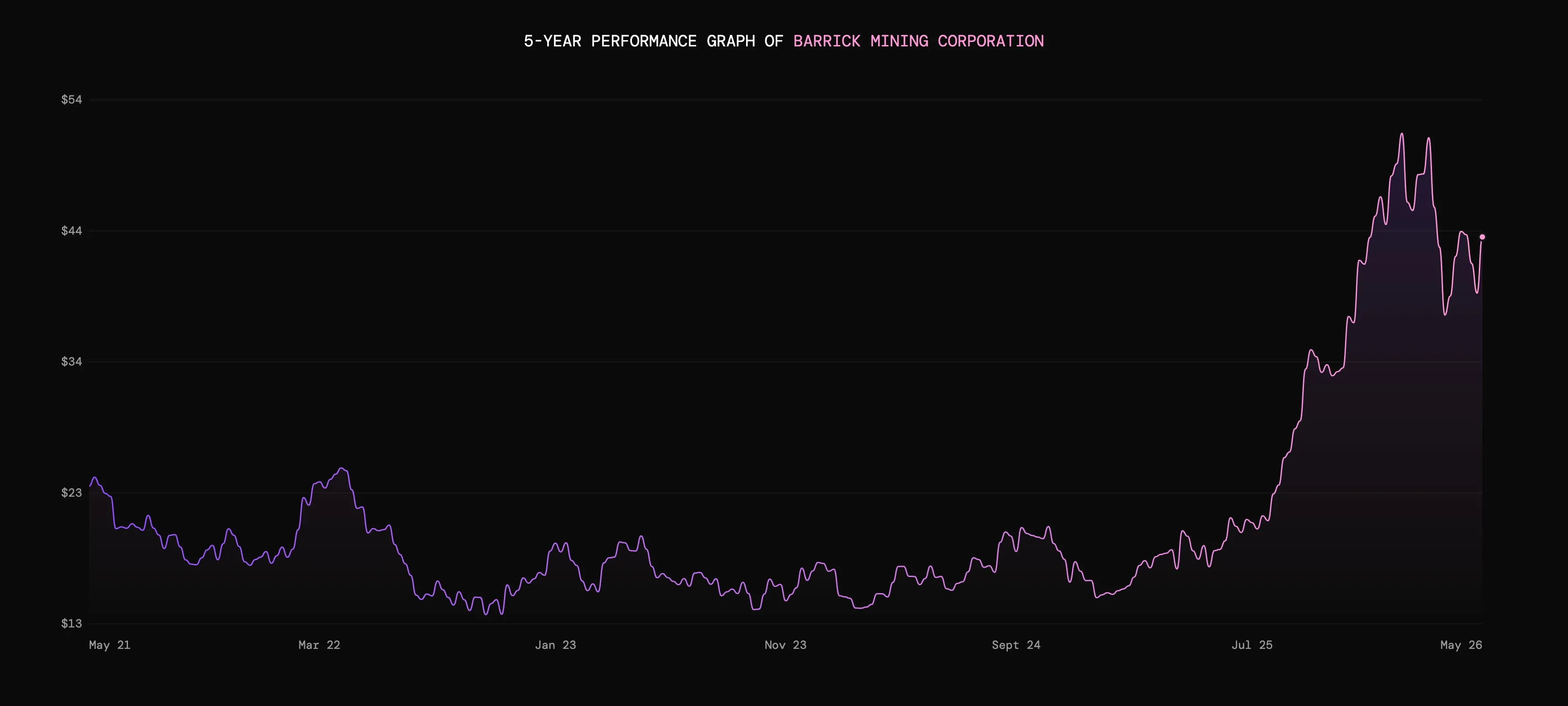

Barrick Mining - Earnings review

The gold miner produced 719,000 ounces in Q1, ahead of its 640,000-680,000 ounce guidance range, helped by stronger output at Nevada Gold Mines and Veladero, plus a faster ramp-up at Loulo-Gounkoto. Copper production landed at 49,000 tonnes, broadly in line with guidance.

With gold prices doing a lot of the heavy lifting, revenue rose 67% year-on-year to $5.2bn, while operating cash flow more than doubled to $2.6bn. Net earnings per share came in at $0.96, up from $0.27 a year earlier, while adjusted EPS rose to $0.98.

That is what operating leverage looks like when the commodity price is on your side. Barrick’s realised gold price was $4,823/oz, up 66% on Q1 2025, while gold all-in sustaining costs fell 4% year-on-year to $1,708/oz.

Shareholders got a direct slice of that uplift too. Barrick declared a $0.175 per share quarterly dividend and announced a new $3bn buyback programme.

Barrick says it is still targeting the end of 2026 for a minority listing of the company holding its North American gold assets, including Nevada Gold Mines, Pueblo Viejo and Fourmile.

Guidance was left unchanged, with full-year gold production still expected at 2.9mn-3.25mn ounces and Q2 output guided to 730,000-770,000 ounces.

Q1 was a good start, but Barrick may need the usual mining cocktail of stable operations, controlled costs, supportive commodity prices and no unwelcome geopolitical surprises.

For now though, higher gold prices, better-than-expected production and chunky shareholder returns made this a strong quarter.

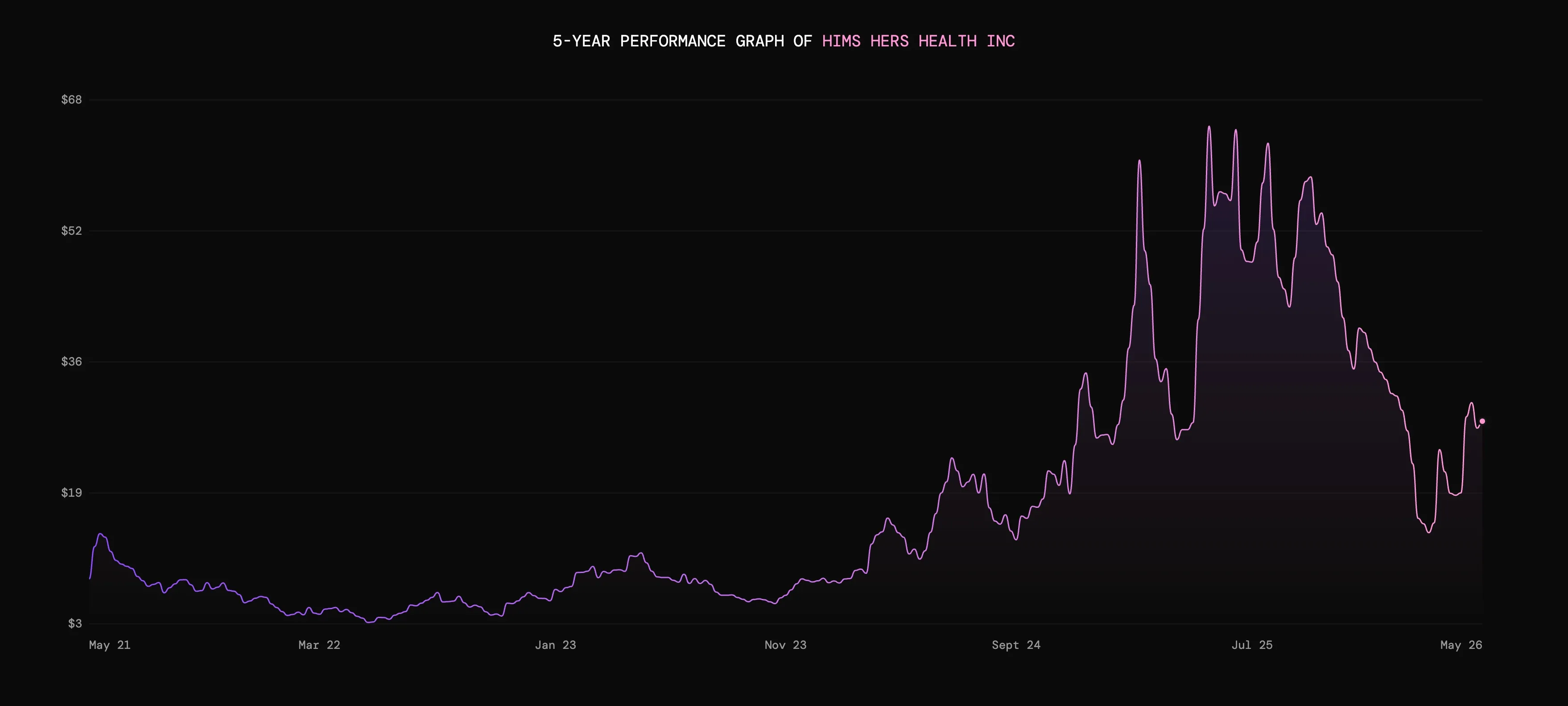

Hims & Hers - Earnings review

Hims & Hers released its Q1 earnings after the market closed on Monday.

The business is a digital health platform, offering users direct access to treatments for issues concerning sexual health, hair loss, dermatology, weight loss, and more.

Total revenue edged 4% higher YoY driven by the company’s expansion into foreign markets. Rest of World revenue leapt from $7.3m to $78.2m, but that remains pocket change compared with the business’s core US market. Here, revenue fell by 8% to $529.9m.

Subscriber growth of 9% is an encouraging sign, though revenue per subscriber fell by 6% to $80. Margins tightened to 65% from 73% in the same period last year, and the business swung to a net loss of $92.1m.

Looking ahead, the company said it expected Q2 revenue to land between $680m and $700m, and boosted FY revenue guidance to $2.8bn to $3.0bn.

However, it also flagged a greater than expected margin squeeze as the business continues to prioritise getting new subscribers through the door with branded GLP-1 products and expansion of the lower margin weight loss and international parts of its customer base.

GLP-1 agonists include the popular weight loss drugs Wegovy and Ozempic. Hims & Hers has shifted its weight-loss strategy towards branded treatments, including through a partnership with Novo-Nordisk to offer Wegovy.

Hims & Hers continues to grow its addressable market at pace, but lower customer spend and further margin pressure mean that profitability is taking a hit. Can the business prove that securing a larger customer base is the correct way for it to disrupt the healthcare market and achieve long-term growth?

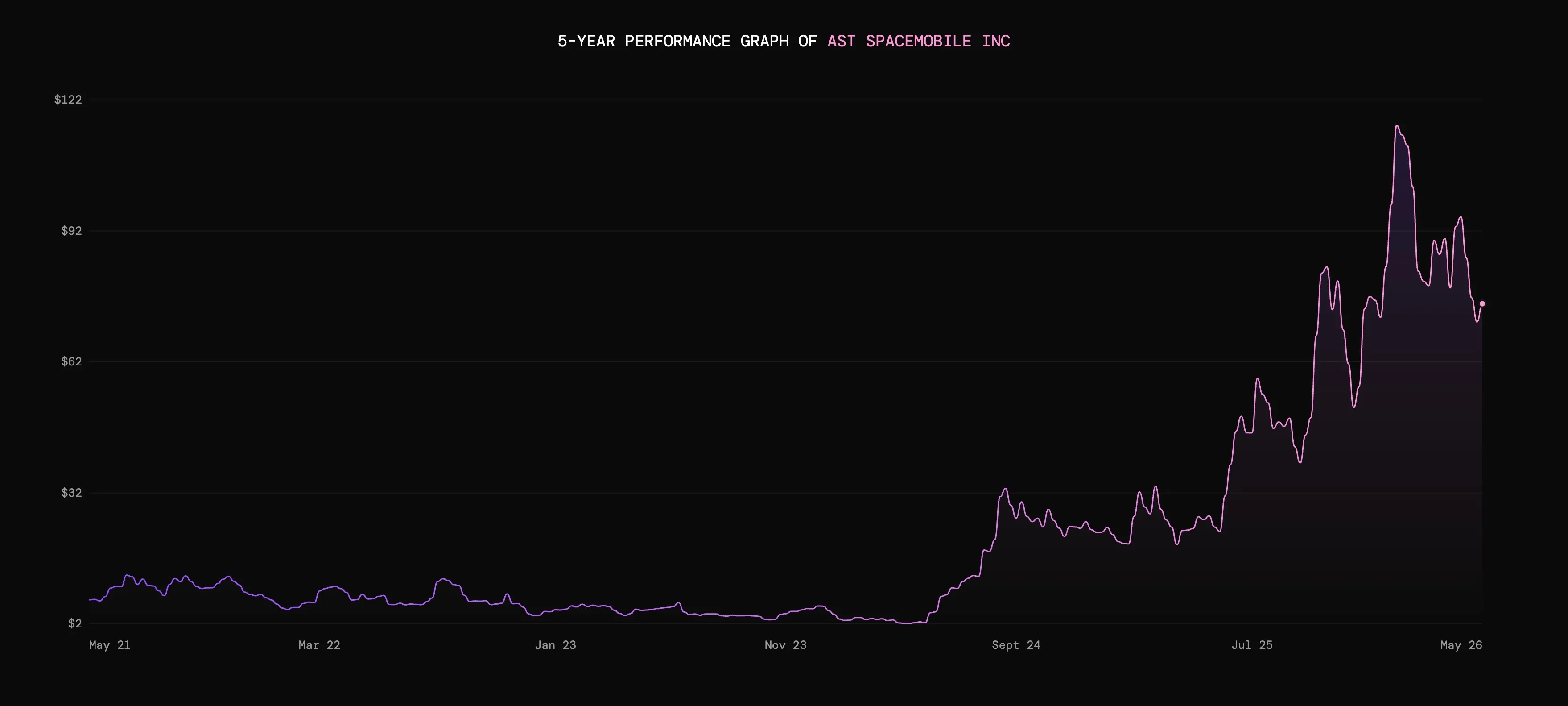

AST SpaceMobile - Earnings preview

AST SpaceMobile also reported its Q1 2026 earnings after market close on Monday.

Consensus expectations had revenue pegged at $36.6m and loss per share of $0.20. The company’s numbers fell considerably short of this. Q1 Revenue missed by some distance, coming in at $14.7m, while loss per share was wider than anticipated at $0.66.

The business is building what it calls ‘the world’s first and only space-based cellular broadband network’. The aim of this is to offer total connectivity, regardless of location.

To achieve the goal, AST aims to have approximately 45 satellites in orbit by the end of the year, a target it doubled down on as it said its BlueBird 8, 9, and 10 launches are all on track.

But firing satellites into space is no simple feat. In April, the company’s BlueBird 7 launch ended in failure, as the craft did not reach the correct altitude. Further dud launches could jeopardise AST Spacemobile’s ambitions and investor confidence.

Its latest update is perhaps a jarring crash back to earth. Back in Q4 2025, the business reported revenue of $54.3m and loss per share of $0.26.

The business is early in its revenue-generating journey, with 2025 its first year of significant sales, as it brought in $70.9m.

Even this might not yet have caught up with costs, but the company indicated 2026 would see accelerated growth thanks to increasing partner revenue and government contract milestones.

This failed to emerge in Q1, but the business does still have over $1.2bn in contracted revenue commitments. It’s worth noting that the balance sheet remains relatively healthy, with $3.5bn in cash providing AST a significant runway.

In addition, the business has also pledged to launch commercial direct-to-device services this calendar year.

There are risks around the success of its launches, but the business faces intimidating competition from Elon Musk’s SpaceX and its Starlink project.

AST has solid financial foundations and a bold plan, but can it recover from an underwhelming quarter to deliver proof of concept before the year is out?

Cisco - Earnings preview

Cisco’s Q3 2026 earnings release is scheduled for after the market close on Wednesday.

Consensus expectations are for revenue of $15.6bn and EPS of $1.04. But hitting these figures might not be enough for investors.

Looking at Cisco’s Q2 earnings delivered double-digit growth in revenue and net income, beating both consensus expectations and company guidance.

But the firm’s share price declined sharply in the immediate aftermath. Why?

Profitability appears to be a concern. This starts with an evident squeeze on non-GAAP gross margins, which fell by 120 basis points YoY, which may have raised investors’ hackles. Forward guidance also showed EPS at between $1.02 and $1.04, remaining flat or dipping slightly quarter-on-quarter.

The cost of memory is a significant drag for Cisco.

As a reminder, many memory suppliers have shifted focus to specialised AI chips due to surging demand. This means more standard DRAM and SSD memory units are becoming harder to source.

Memory chips are a crucial component of Cisco’s networking hardware, so the shortage puts it in a tricky position.

Last quarter, the company said it was proactively tackling the issue through price rises and contract renegotiations. The impact on margins and any related guidance could drive investor sentiment.

The other key driver is what is emerging as Cisco’s key product.

AI infrastructure demand drove the company’s product revenues 14% higher to $11.6bn. Hyperscaler infrastructure orders for Cisco hit $2.1bn in Q2, up from $1.3bn in Q1, and the business is confident orders from the top table will hit $5bn across the FY.

The key is its Silicon One chipset, a highly programmable building block with applications across data centres, service providers, and more. The company’s new G300 variant of the system was announced in February and was slated for release later in 2026. More roadmap news and insight into continued chipset demand could be crucial for Cisco.

Product-led growth has made Cisco’s top-line numbers impressive, but can the company navigate the choppy waters of the memory crisis with its margins intact?

Alibaba - Earnings preview

.webp)

Alibaba reports its Q4 FY2026 results before the market opens on Wednesday. Alibaba’s fiscal year ends on 31 March 2026. Investors are likely to be watching for AI and cloud momentum on one side, and profit pressure on the other.

Expectations are around $35.8bn in quarterly revenue and EPS of roughly $0.89.

Last quarter, cloud revenue rose 36% year-on-year, with AI-related product revenue delivering triple-digit growth for the tenth consecutive quarter.

But Alibaba’s December quarter net income fell sharply, with non-GAAP net income down 67% year-on-year, as the company pumped money into AI, cloud infrastructure, user experience and quick commerce. Sales and marketing spending also rose materially as a share of revenue, mostly because of investment in China e-commerce.

Management has been leaning hard into the idea that AI and cloud are now primary growth engines, but the market will want evidence that investment is translating into revenue growth, pricing power and, eventually, operating leverage.

The other moving part is the firm’s core commerce engine. Alibaba still has to defend its home turf against JD.com, PDD and Meituan, while also spending to keep consumers engaged across faster-delivery and local services.

A clean beat on revenue alone may not be enough if profits keep sliding. But if the company can show that its AI spending is building a higher-growth, higher-quality business rather than just a more expensive one, investors may be willing to look through another messy quarter.

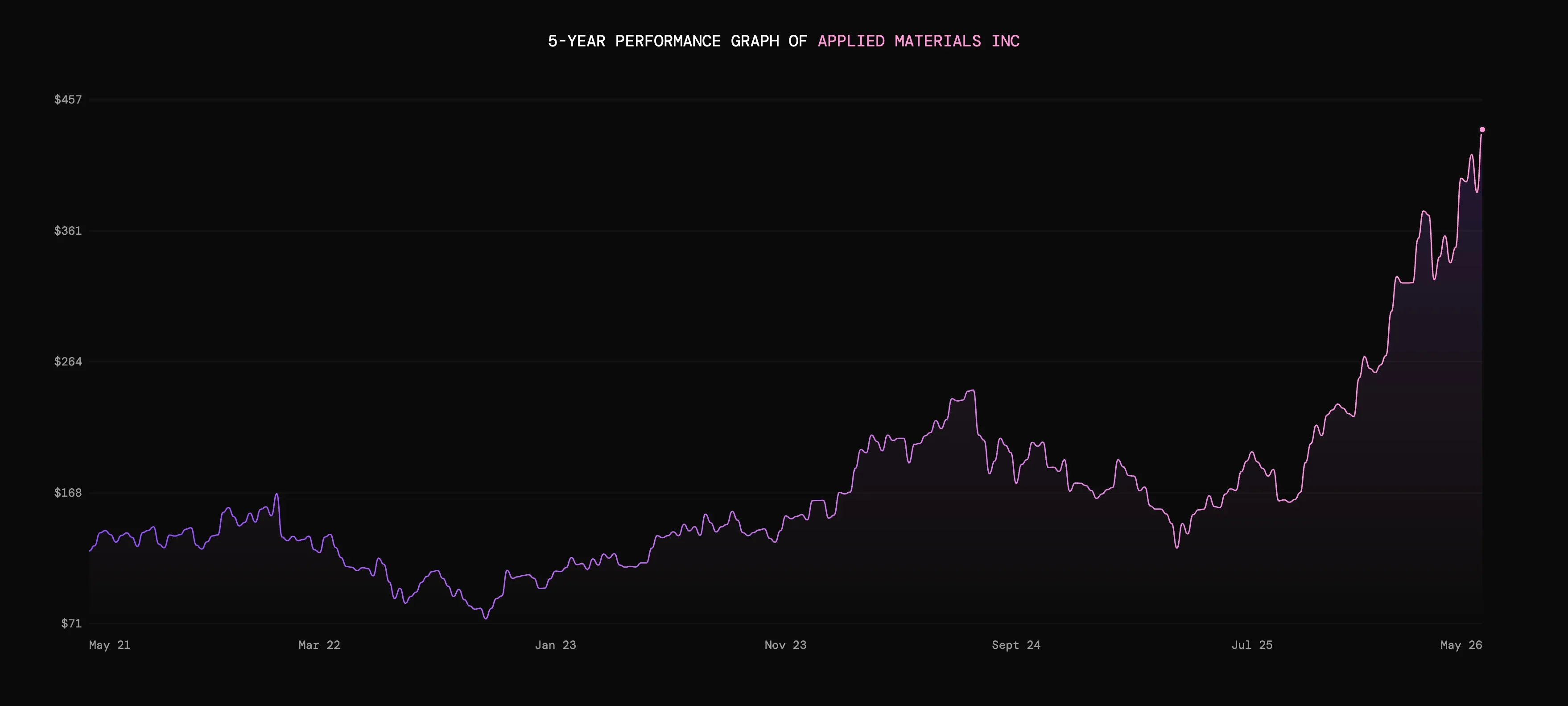

Applied Materials - Earnings preview

Applied Materials reports its fiscal Q2 2026 results on Thursday after US market close.

Investors will be looking for a read on the machines behind the machines.

Applied Materials makes the manufacturing equipment and materials engineering tools used by chipmakers, which puts it close to the pick and shovel end of the semiconductor boom.

Wall Street is expecting roughly $7.7bn in revenue and $2.66 in EPS, while Applied Materials’ own guidance range is $7.2bn-$8.2bn in revenue and $2.44-$2.84 in EPS.

Last quarter, the company beat expectations with $2.38 EPS on $7.01bn of revenue, and management guided to a stronger fiscal second quarter, helped by demand tied to advanced logic, high-bandwidth memory and advanced packaging.

Investors will want to know whether spending from leading-edge customers is still strong enough to offset softer areas elsewhere, particularly if memory, mature-node equipment or China demand wobble.

China is the obvious pressure point. Applied Materials has previously had to deal with a shifting mix of export controls, customer uncertainty and weaker China-related demand.

Margins will matter too. The market already knows AI needs more chips. The question is whether Applied Materials can keep converting that demand into profitable growth without too much friction from supply chain costs, geopolitics or lumpier customer spending.

Capital at risk. The value of your investments can go down as well as up and you may get back less than you invest.

Fluctuations in foreign exchange rates may affect investments denominated in currencies other than GBP and the amount you receive back.

Past performance is not a reliable indicator of future returns.

Freetrade does not give investment advice and you are responsible for making your own investment decisions. If you are unsure about what is right for you, you should seek professional advice.

Always do your own research.

.png)

%2520(1).avif)