Earnings updates from tech giants Apple, Amazon, Alphabet, Meta, Microsoft, and Qualcomm are the big news this week.

Find out what to expect and what to look for, as some of the largest and most innovative companies in the world prepare to bare their balance sheets and update the market.

Microsoft

Microsoft’s Q3 earnings will hit after market close on Wednesday.

On Monday, the business loosened ties in its crucial relationship with ChatGPT owner OpenAI. Microsoft will no longer pay OpenAI a revenue share, and will lose the exclusivity of its products.

On the other side, OpenAI will continue to pay Microsoft a revenue share through to 2030, and Microsoft will have access to OpenAI IP to 2032.

The upshot? Both sides have more room to manoeuvre in what they describe as a “simplified” partnership.

What this means for Microsoft’s AI ambitions is key, and investors will look for insights on Wednesday.

Looking back, the company’s Q2 earnings beat top-line expectations, with revenue climbing by 17% YoY to $81.3bn. But investors were spooked by AI infrastructure spending and cloud margin pressure. In addition, Azure revenue growth decelerated across quarters from 40% to 39%.

This time, revenue is anticipated at $81.4bn, up by 16% YoY, while consensus EPS estimates are at $4.07.

Perhaps the key for Microsoft is reassuring the market. Can it prove its core cloud business remains resilient and that long-term AI plans are not compromised?

Alphabet

.webp)

Google parent company Alphabet is also reporting after market close on Wednesday.

Expectations are high, with overall revenue anticipated at over $107bn, up 18% YoY.

Driving the projected growth is the Cloud arm, slated for 50% YoY revenue growth by analysts. The segment is aided by demand for AI infrastructure and enterprise AI tools. It may prove that spending big on AI can translate into revenue, not just higher capex.

Services remains the business’s foundation, and further steady growth is crucial. AI had been seen as a stumbling block, but the segment’s revenue grew by 10% in the prior quarter. Increasing integration of Gemini may be bolstering Alphabet’s performance here.

The past quarter has also seen the company shine for its investing savvy.

Earlier this month, filings revealed Alphabet’s significant stake in SpaceX, which is reportedly prepping a 2026 IPO. In addition, autonomous driving company Waymo, in which Alphabet is majority shareholder, was valued at over $100bn in February after raising $16bn.

Alphabet is diversifying beyond Search, even as the core business maintains steady growth. Will this quarter continue to reflect this strength?

Apple

Apple’s Q2 earnings are coming after the closing bell on Thursday.

First, Apple just confirmed Tim Cook will step aside after 15 years at the helm. Hardware engineering chief John Ternus will take the reins in September.

Watch out for transition info and hints of any change of direction.

In Q1, the business scored record revenues of $143.8bn, up 16% YoY. Q2 is unlikely to match this, as festive gift-giving and reliance on product mean Q1 is always the highlight of Apple’s financial year.

However, sustained iPhone momentum, particularly in China, will be in focus. Apple’s recent success in the market comes after battling strong domestic competition and overcoming government hostility. Reports suggest a 20% increase in iPhone shipments to China in the first three months of the year.

Product may be Apple’s core, but Services and its subscription-based revenue from sources like Apple TV, Apple Music, and the App Store provide an engine for high-margin sales.

A solid showing, and positive margin impact, here could be key as AI spend hoovers up so much of tech giants’ capex. Following the delayed launch of upgraded Siri features, Apple faces increasing pressure to catch up in the AI race and may need spending flexibility.

Consensus estimates suggest revenue of $109.7bn, up 15% YoY, and EPS of $1.94 in Apple’s second quarter.

Apple appears to have momentum, but the business must prove its strength can outlast both Tim Cook and the festive season.

Amazon

Amazon reports Q1 2026 earnings after the US close on Wednesday.

Wall St is expecting roughly $177bn of revenue (roughly low-teens growth) and around $1.63 EPS.

The two growth engines are Amazon Web Services (AWS) and advertising. AWS is the AI plumbing story (compute demand + custom chips), while ads are the higher-margin tailwind that can keep profits growing even if retail margins wobble.

The main focus, though, is guidance and margins. Amazon’s spending is ginormous. The market wants to hear that AI capex is translating into durable demand, not just an ever increasing arms race. Any shift in tone on investment levels, AWS growth, or retail profitability could swing the numbers more than the headline beat.

Amazon is the week’s cleanest test of whether the AI buildout is still showing up in cloud demand. And whether the cost of all that building is starting to pinch

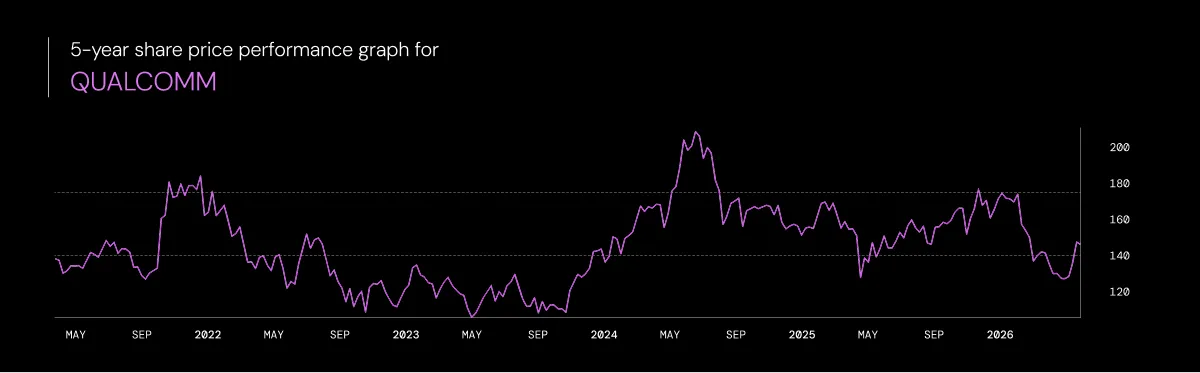

Qualcomm

Qualcomm reports its Q2 2026 earnings after the US close on Wednesday.

Consensus expectations are around $10.59bn revenue and $2.58 EPS, which sits close to the company’s own guidance range (EPS $2.45-$2.65).

This print is a read on the phone cycle and Qualcomm’s push beyond phones. Investors will be listening for momentum in automotive and IoT/edge AI. In particular, whether those segments are offsetting a mature handset market.

Two shareholder return numbers to clock: Qualcomm approved a $20bn buyback (about 14.5% of shares) and raised its quarterly dividend to $0.92 (annualised $3.68, ~2.7% yield).

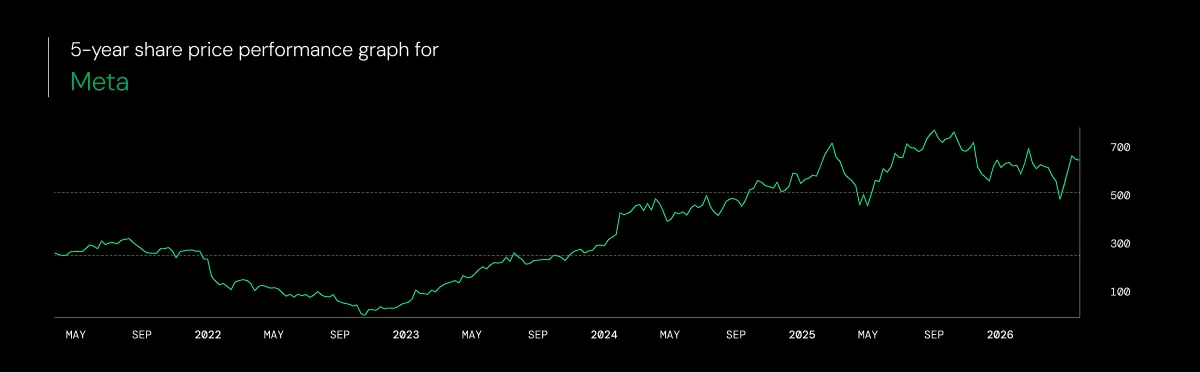

Meta

Meta reports its Q1 2026 earnings after the US close on Wednesday.

Wall St is expecting another bumper quarter: roughly $55.56bn of revenue (about +31% YoY) and $6.64 EPS (roughly +3% YoY).

Can the Meta ad machine keep printing money fast enough to feed the AI monster? Meta has guided to $115-$135bn of capex in 2026, and has leant into layoffs in order to fund that AI infrastructure spend.

Keep an eye on ad pricing and volumes, Reels monetisation, and whether management can sound confident on efficiency while still ploughing cash into data centres. If capex stays huge and the ad cycle wobbles, the stock gets sensitive fast.

Capital at risk. The value of your investments can go down as well as up and you may get back less than you invest.

Fluctuations in foreign exchange rates may affect investments denominated in currencies other than GBP and the amount you receive back.

Past performance is not a reliable indicator of future returns.

Freetrade does not give investment advice and you are responsible for making your own investment decisions. If you are unsure about what is right for you, you should seek professional advice.

Always do your own research.

.png)

.avif)