It’s the start of another busy week for earnings, and this time round we are focusing on a mix of healthcare, cybersecurity, and semiconductor names.

CrowdStrike and Palo Alto Networks will offer insights on cybersecurity budgets, Medtronic needs to show its core medical-device business can keep growing, and Broadcom will test how much confidence remains in the AI hardware boom. Get the lowdown, down below.

Palo Alto Networks - Earnings preview

Palo Alto Networks reports fiscal Q3 2026 results after the US close on Tuesday.

The company has guided for $2.94bn-$2.95bn of revenue, implying 28%-29% year-on-year growth, with non-GAAP EPS expected at $0.78-$0.80. Consensus looks broadly aligned on revenue.

Palo Alto has been hawking security bundles across cloud, network and security operations, rather than selling products one at a time. This strategy is borne out of the idea that larger customers want fewer vendors and deeper integrations, as well as more AI-enabled automation.

Next-generation security will be the number to watch. Last quarter, NGS annual recurring revenue rose 33% to $6.3bn, while remaining performance obligation grew 23% to $16bn. Those figures give a better read on future demand than one quarter’s revenue alone.

The awkward bit is profitability. Palo Alto’s Q3 EPS guidance came in below expectations after Q2, with management flagging pressure from higher memory and storage costs. So investors may be less forgiving of a revenue beat if it comes with thinner margins.

AI gives Palo Alto a new sales angle, but it also raises the spending bar, both for customers and for Palo Alto itself. The company needs to show AI is becoming a demand driver, not just another line item in the cost base.

A strong print would suggest cyber budgets are still resilient and customers are buying into the bigger bundled-security pitch. A softer one would raise the question of whether even high-quality cybersecurity names are having to spend harder to keep growth buoyant.

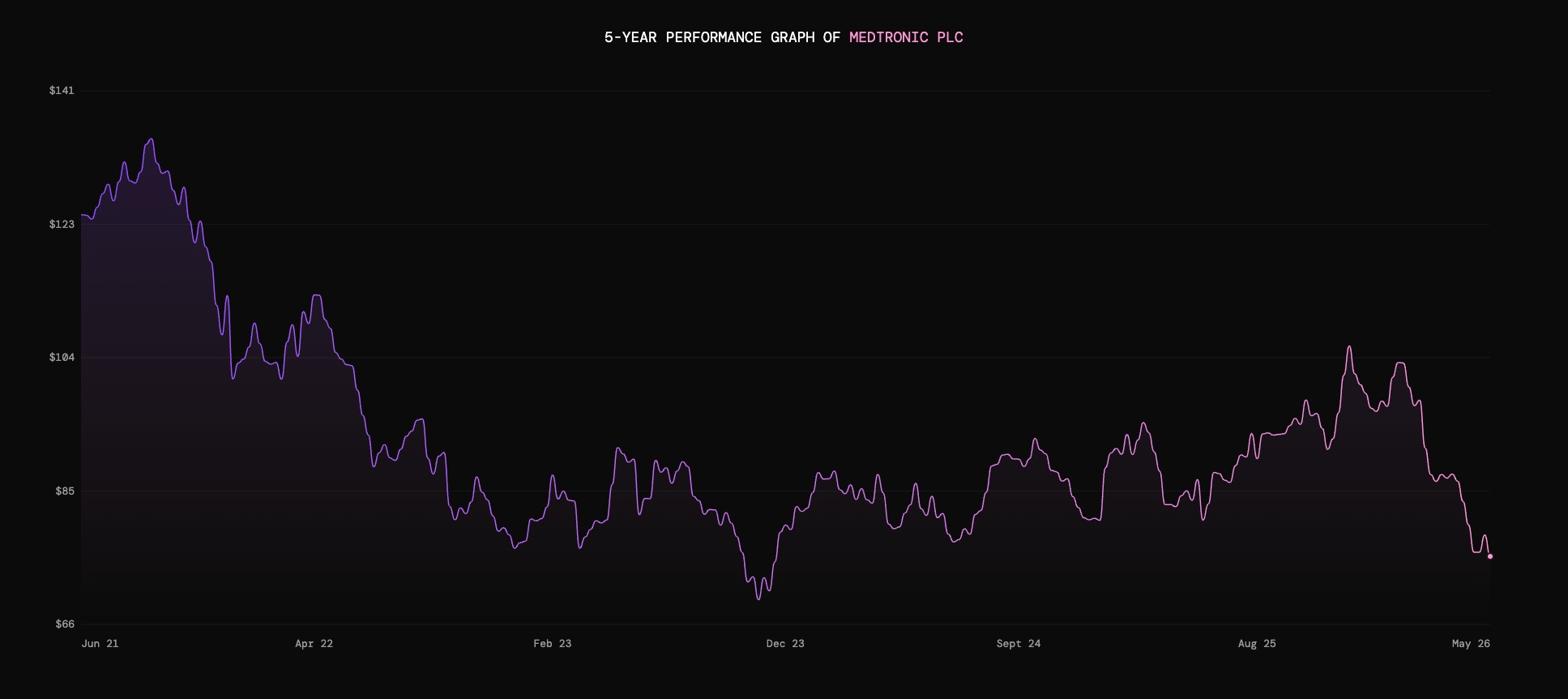

Medtronic - Earnings preview

Medtronic’s Q4 earnings are due before the market opens on Wednesday.

The business makes healthcare tech such as pacemakers, defibrillators, insulin pumps, and surgical tools. Consensus expectations are for revenue of $9.6bn and EPS of $1.55.

Last time out, the business reported headline revenues of $9.0bn, up by 8.7% YoY, while non-GAAP diluted EPS of $1.36 was toward the upper end of guidance.

The cardiovascular portfolio showed heart, contributing Q3 organic revenue growth of 10.6%. Medtronic’s Cardiac Ablation Solutions were the standout here, growing by 80%. This range of products includes pulsed-field ablation technology, which treats arrhythmia through targeted emission of electric fields.

However, operating profits dipped by 11.1% to $1.5bn. Higher product and selling costs have squeezed margins at the medical device company. Part of this is due to R&D spend, but tariff pressure is another lingering factor that may impact Q4.

The period also saw Medtronic’s diabetes business, MiniMed, go public through an IPO. Medtronic continues to hold a majority stake above 90%, and hopes the move keeps its core business clean and focused on core competencies.

However, it could cause a bit of near-term confusion, particularly around tax and earnings impact.

Can Medtronic’s cardio strength help organic revenues accelerate, or will tariffs and confusion around the MiniMed separation create fresh headaches for the business?

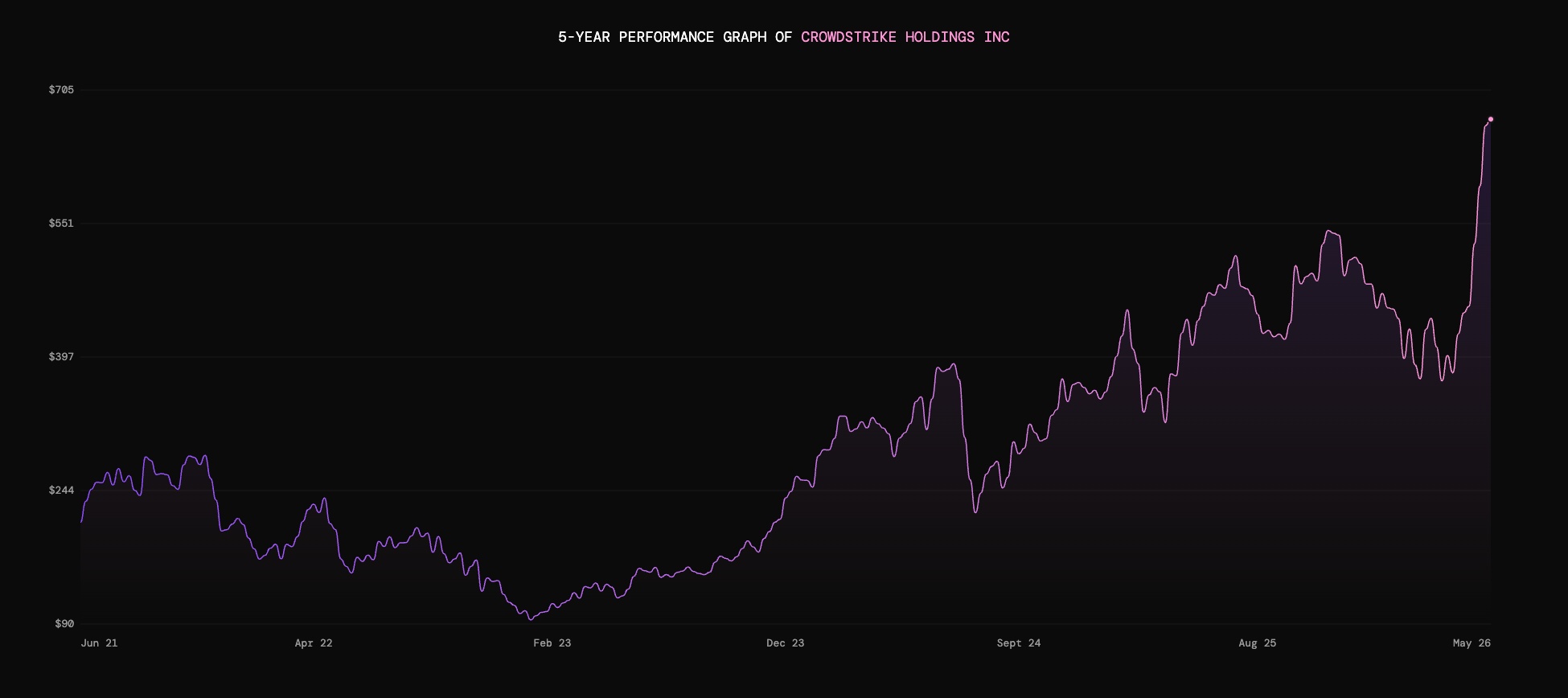

CrowdStrike - Earnings preview

CrowdStrike reports fiscal Q1 2027 results after the US close on Wednesday.

Consensus is revenue of around $1.36bn, while EPS estimates sit around the $1 mark.

CrowdStrike’s platform model Falcon has made it one of the bigger cybersecurity growth names, because the pitch is getting customers to consolidate more of their protection, detection and response spending in one place.

Cybersecurity is one of the areas where AI is both a threat and a sales tool: attackers can move faster, but defenders can also automate more of the work. Investors will want to see that CrowdStrike’s AI messaging is turning into larger deals and stronger recurring revenue.

The hangover from the 2024 outage has not fully disappeared. CrowdStrike has done a lot to rebuild investor confidence, but the market will still be watching. A solid quarter would suggest the reputational damage is increasingly behind the firm.

All in all, CrowdStrike needs to show that cybersecurity budgets are still resilient and AI is helping rather than just inflating expectations.

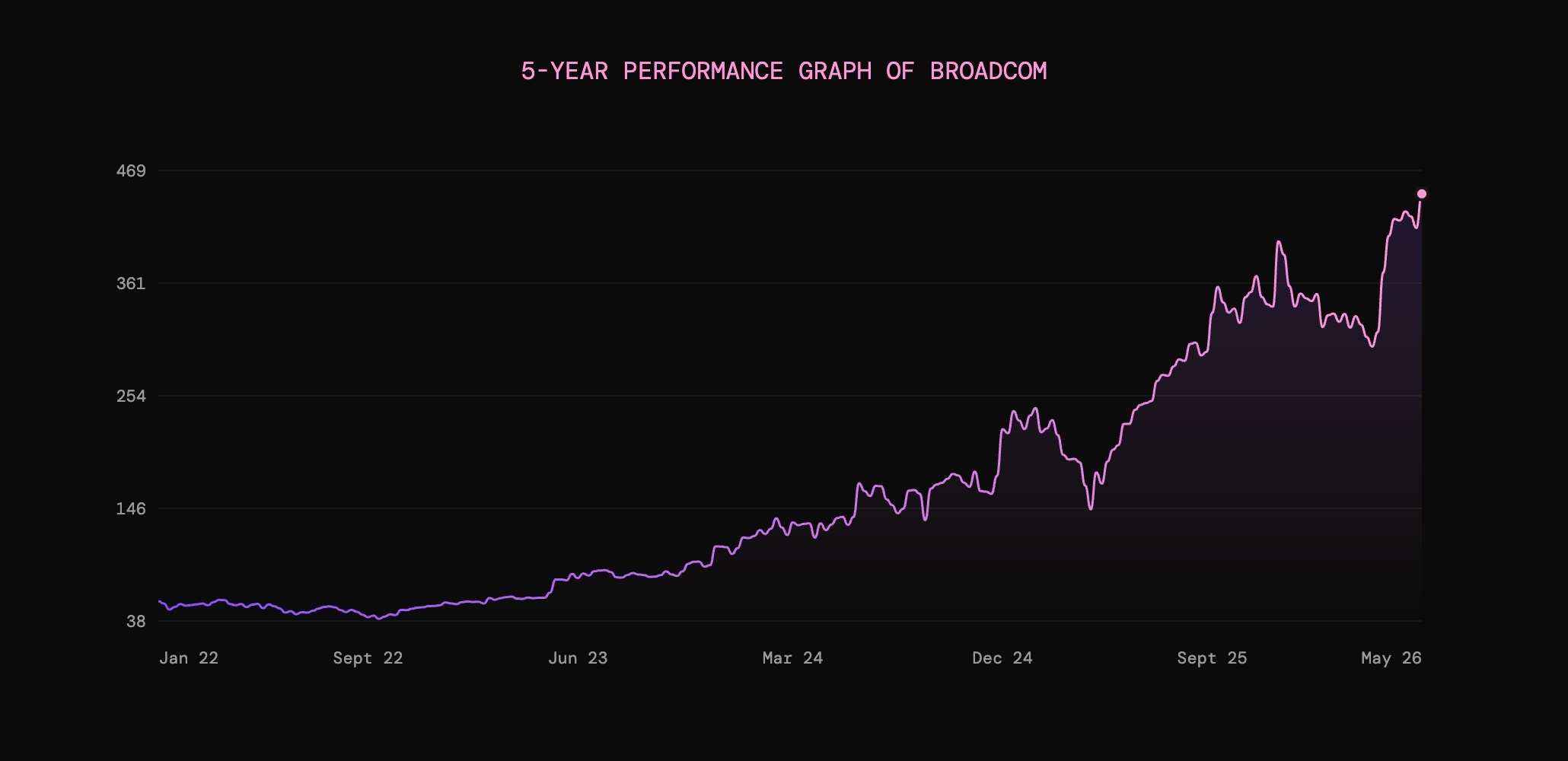

Broadcom - Earnings preview

Broadcom’s Q2 FY2026 earnings release is scheduled for after the market close on Wednesday.

The company makes hardware and software for digital networks and communications. On the hardware side it makes components and semiconductor chips for applications in data centres, wireless devices, and more. Meanwhile, its software offering includes cloud infrastructure and network cybersecurity.

Consensus expectations are for Q2 revenue of $22.1bn and EPS at $2.40.

Back in Q1, revenue came in at $19.3bn. This 29% YoY growth was driven by AI semiconductor revenue, which soared by 106% to $8.4bn. Demand for purpose-built AI processors and networking technology has been a major tailwind.

President and CEO Hock Tan forecasted AI revenue of $10.7bn for Q2. With hyperscaler demand for AI infrastructure still rocketing, the big question is whether Broadcom’s custom chips and networking tech are attractive enough to rake in the capex pouring out of Silicon Valley.

But this growing segment is reliant on very few high-spending customers. If orders slow, projects shift, or one or two hyperscalers bring more chip design in-house, Broadcom could be vulnerable.

In the background, Broadcom’s infrastructure software segment gives it a high-margin facet to fall back on. But growth here is sluggish, with revenues up by just 1% YoY in Q1. In Q2, the business guided to 9% YoY growth.

Can Broadcom firm up its foundations by delivering software revenue growth, and will it keep up with the AI hardware boom?

Capital at risk. The value of your investments can go down as well as up and you may get back less than you invest.

Fluctuations in foreign exchange rates may affect investments denominated in currencies other than GBP and the amount you receive back.

Past performance is not a reliable indicator of future returns.

Freetrade does not give investment advice and you are responsible for making your own investment decisions. If you are unsure about what is right for you, you should seek professional advice.

Always do your own research.

.avif)