This week’s earnings preview merges semiconductor signals, AI exposure, and a good old-fashioned retail heavyweight.

Earnings season might be winding down a little, but the week still has some key highlights. Read on for the lowdown on a chip designer that’s rubbing shoulders with some of Silicon Valley’s biggest hyperscalers, insights into AI agentic software, and much more.

Salesforce - Earnings preview

Salesforce reports its Q1 FY27 results after the US close on Wednesday.

The firm is guiding for $11.03bn-$11.08bn of revenue and non-GAAP EPS of $3.11-$3.13, broadly in line with consensus.

The focus will be Agentforce, Salesforce’s AI agent platform, which lets companies build AI agents that can do tasks inside Salesforce and connected systems.

The market will want evidence customers are adopting these agents at scale, rather than just testing them in small pilots.

The other thing to watch is organic growth. Salesforce’s Q1 guide includes a little over four percentage points of contribution from Informatica, an enterprise data management software company Salesforce acquired for about $8bn. Therefore, headline growth may look healthier than the underlying engine. And any sign AI investment or acquisition integration is eating into profitability will get noticed.

For the full year, management is guiding to a 34.3% non-GAAP operating margin, which sets a fairly high bar. Salesforce needs to show AI is becoming a revenue driver. A strong print would suggest the Agentforce story is starting to show up in the numbers.

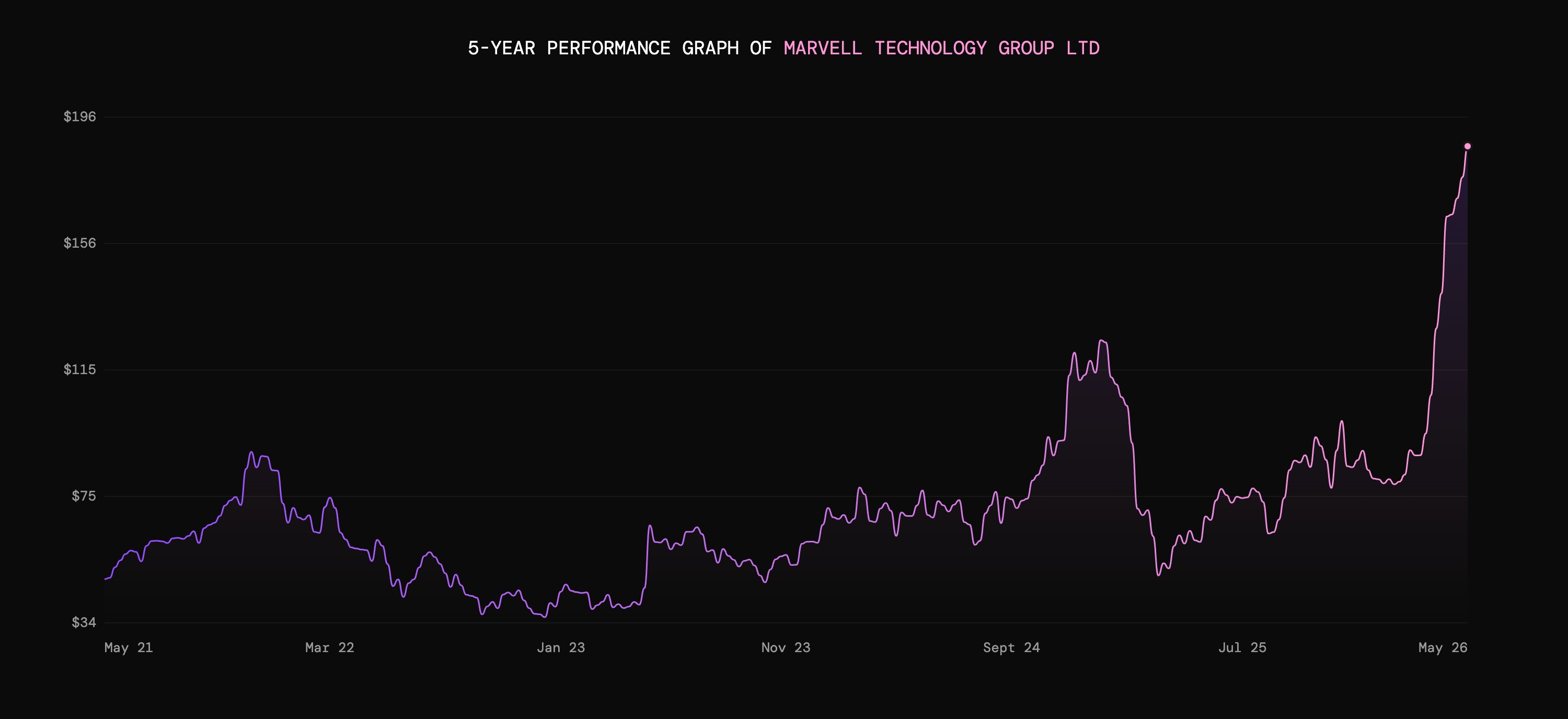

Marvell Technology - Earnings preview

Marvell reports its Q1 2027 earnings on Wednesday, after the market close.

The company is a designer of semiconductors and related components. This has left it well-placed to benefit from AI infrastructure demand for custom chips, optical networking, and data-centre components.

Last time out, the company hit net revenue of $2.2bn, up 22% YoY, and net income nearly doubled as it reached $396.1m. Data Center revenue rose by 21% in the period, and accounted for 74% of total revenue.

The business set out clear goals for its year ahead, with Chairman and CEO Matt Murphy commenting:

“We expect year-over-year revenue growth to accelerate each quarter in fiscal 2027, driven by continued strength in our data center business, with bookings continuing to grow at a record pace.”

Looking to Q1, consensus estimates are broadly in line with company guidance, with revenue pegged at $2.4bn, and EPS of $0.79.

Over the last quarter, pressure to vertically integrate AI infrastructure has led hyperscalers to knock at the chip designer’s door. Unconfirmed reports have linked Marvell to Alphabet’s Google Tensor Processing Units (TPUs).

These are specially designed machine-learning chips that compete directly with industry leader Nvidia’s GPUs.

Speaking of Nvidia, the chip kingpin also came a-calling in the period as it invested $2bn in Marvell as the duo launched a design partnership.

Marvell really is moving in elevated circles now.

This has not gone unnoticed. Marvell’s share price has more than doubled year-to-date, pushing its market cap north of $150bn.

But that raises the bar. Meeting top-line expectations or toting basic connections to big players might not cut it. Fussy investors will want clear evidence the AI ramp means sustainable growth.

There are vulnerabilities too. For example, the business is highly reliant on a few key customers, with its largest reportedly accounting for 16% of H1 2026 revenue. Just one relationship souring could leave a gaping hole in the business’s earnings.

So, can Marvell Technology’s next update satisfy investor appetite, or will we see the semiconductor stock’s mammoth valuation get chipped away?

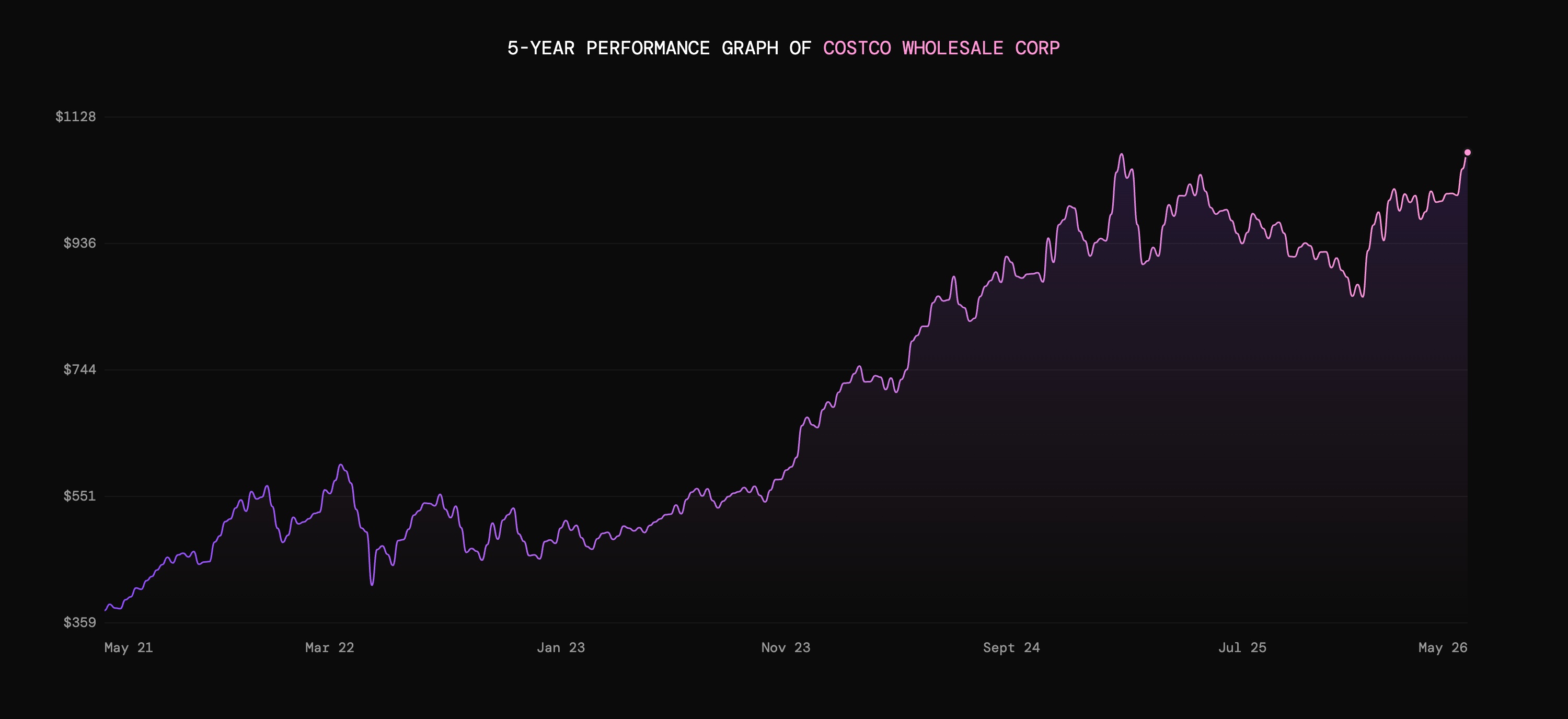

Costco - Earnings preview

Costco’s Q3 earnings update is scheduled for Thursday, after the market closes.

The business is a leading example of membership-led retail. The core of its business model is charging customers an annual fee to access its warehouses of bulk quantity goods, which often retail at lower prices than competitors.

In essence, Costco has turned bulk buying into a loyalty machine.

Wall Street’s expectations are for Q3 revenue to stand at $69.52bn, while EPS is seen at $4.92.

The business releases monthly sales updates, and these suggest shoppers are still getting through the doors and filling their carts.

In April, total company sales were up by 11.6% YoY, following 9.4% in growth in March, and 9.5% in February. Digitally-enabled sales growth has also been strong, running at more than 18% in a large portion of Q3.

Then, there’s membership. This is Costco’s standout factor.

Fee income rose 13.6% to $1.36bn in Q2 following a 2024 membership price increase and growth in paid members. This high-margin recurring revenue is gold dust for the business, and growth can have a major impact on profits. As such, it’s always one to watch.

This weapon is all the more important as Costco’s low prices leave it particularly exposed to rising wages, freight costs, food inflation or tariff pressure.

Can Costco’s membership model help it to continue absorbing cost pressures, or will the big-box retailer start feeling the squeeze?

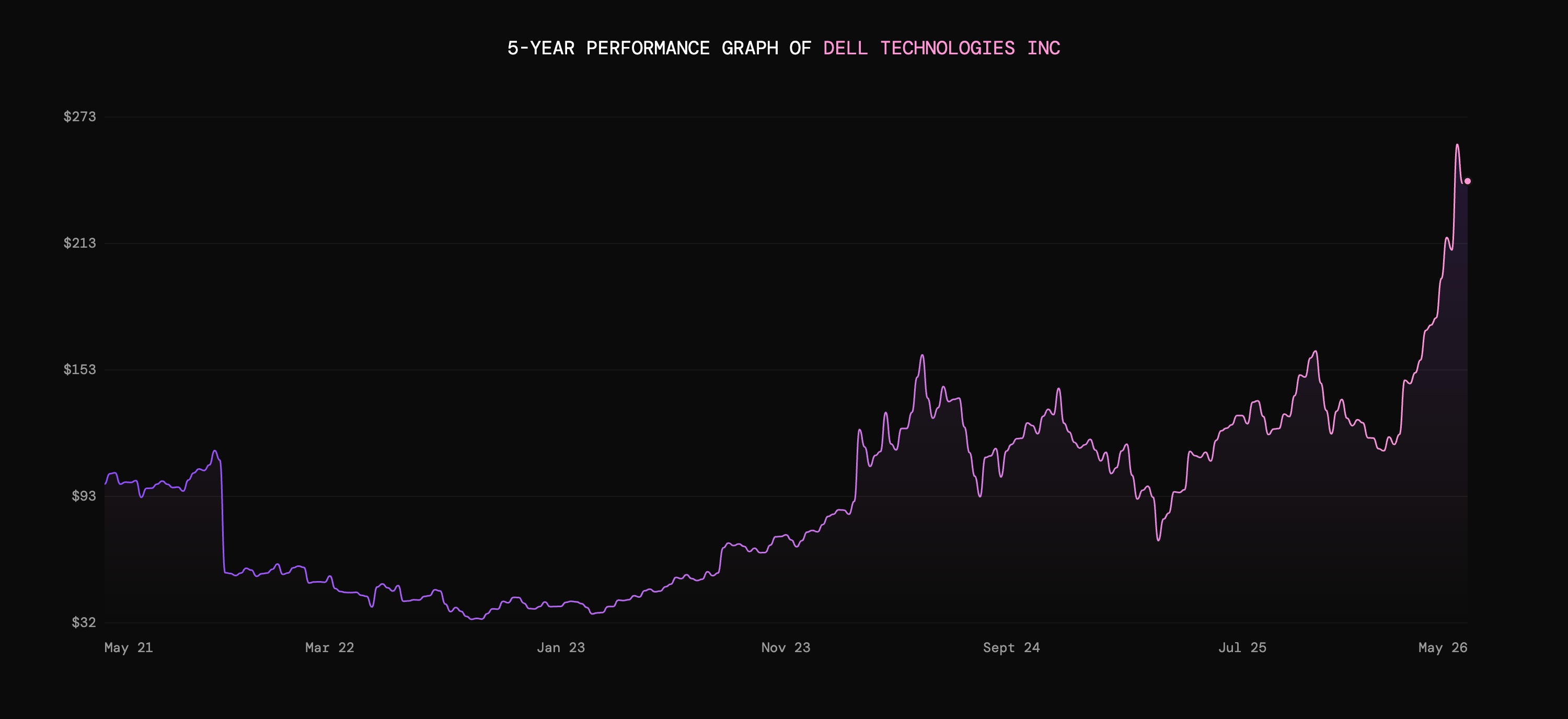

Dell - Earnings preview

Dell reports its Q1 FY2027 results after the US close on Thursday. The firm has guided for $34.7bn-$35.7bn of revenue and non-GAAP EPS of around $2.90.

Analyst expectations are close to the top end, with consensus at $35.66bn of revenue and $2.91 EPS.

Dell has become one of the picks and shovels plays in the AI buildout, selling the servers, storage and networking kit needed to run large-scale AI workloads. Last quarter, the company reported record Q4 revenue of $33.4bn, up 39%, helped by booming AI-optimised server demand.

The question is whether that demand is still accelerating. Dell’s AI server backlog is a key number for investors, because it gives a cleaner read on future shipments than one quarter’s revenue alone. A strong backlog and confident guidance would suggest the AI capex wave is still energising Dell’s infrastructure business.

Margins will matter too. AI servers can add huge revenue, but not always huge profit. So investors will want to see whether Dell is turning AI demand into operating leverage, rather than just more sales with thinner margins.

A strong print would support the idea that the AI buildout is still feeding through to the companies supplying the physical infrastructure. A weaker one would raise the question of whether the boom is creating lasting earnings power.

Capital at risk. The value of your investments can go down as well as up and you may get back less than you invest.

Fluctuations in foreign exchange rates may affect investments denominated in currencies other than GBP and the amount you receive back.

Past performance is not a reliable indicator of future returns.

Freetrade does not give investment advice and you are responsible for making your own investment decisions. If you are unsure about what is right for you, you should seek professional advice.

Always do your own research.