Earnings updates this week from Micron, FedEx, Paychex, and Darden Restaurants mean investors are in for a look at some pretty diverse corners of the market.

While Micron is all about AI-fueled demand for high-end memory chips, Darden’s results will offer more insight into consumer spending habits. Elsewhere, updates will lift the lid on hiring trends and delivery volumes.

So, read on to find out what factors might make one of 2026’s hottest share price runs look fragile, and why one of the world’s largest shipping companies has been split into two.

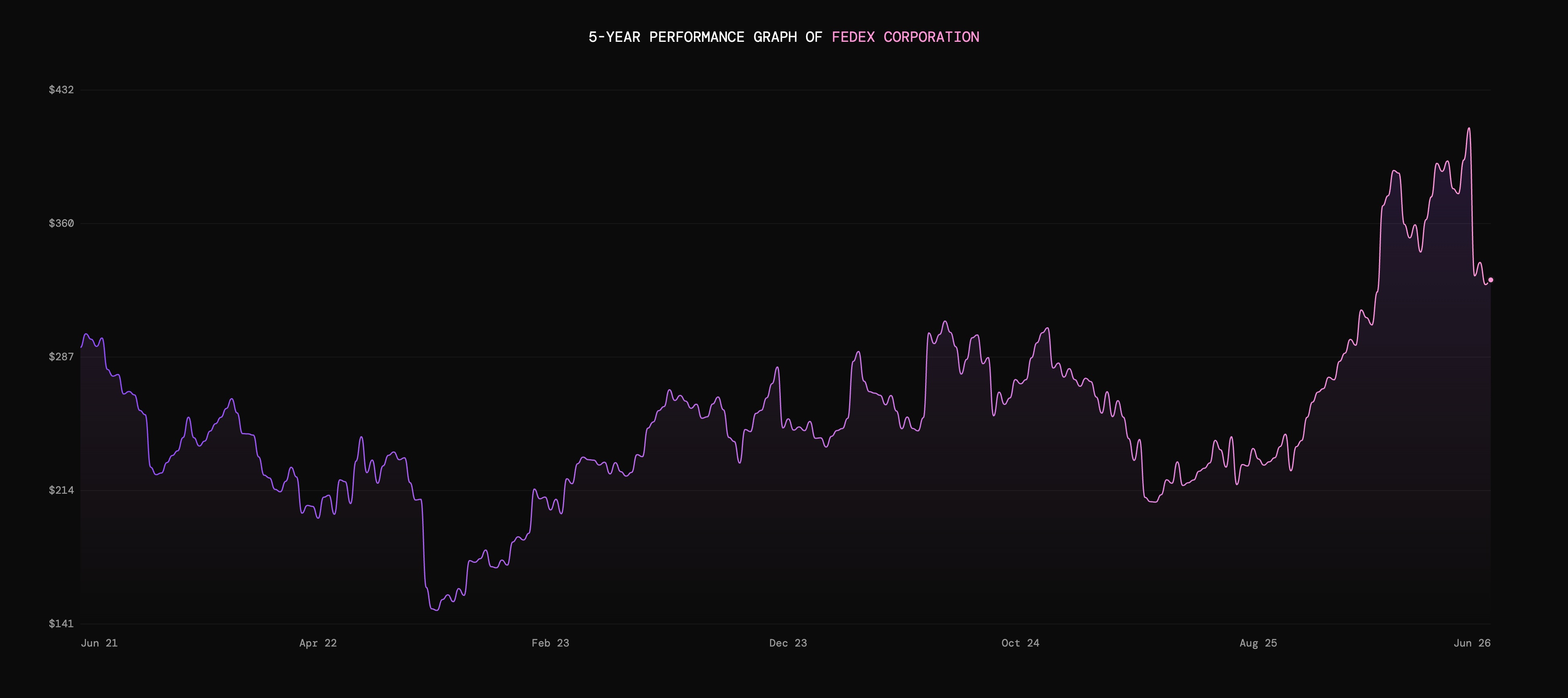

FedEx

FedEx is set to unveil its Q4 2026 earnings on Tuesday after the market close.

Consensus estimates are for the logistics and delivery company to deliver quarterly revenues of $24.03bn and EPS of $5.95.

Last time out, FedEx raised its FY2026 outlook. It boosted expectations for revenue growth to between 6-6.5%, ahead of the previously outlined 5-6%. The company also hiked guidance for diluted EPS and slashed capital expenditure.

Aside from how results stack up against this higher yardstick, the spin-off of FedEx Freight is sure to be in focus. The separation occurred as planned on 1 June, with FedEx shareholders receiving one share in the newly separate freight business for every two FedEx shares owned.

Why the spin-off? The idea is to create two different businesses with distinct identities and priorities.

FedEx’s services encompass ecommerce, transportation, and business services.

On the other hand, FedEx Freight is primarily focused on less-than-truckload (LTL) freight services in North America.

Obviously, investors and onlookers will want insight into what things look like post-freight. Expect package volumes to be a particularly important metric, as the business is now more exposed to the demand and success of its core delivery operations.

Last quarter, total average daily package volumes were up by 3% YoY, helped by particular strength in the US domestic market. Meanwhile, composite package yield, which is effectively revenue earned per package, also rose by 6% YoY. This led operating margins in the core Federal Express business segment to expand by 70bps to 7.4%.

Forward margin guidance for FY2027 will be key, with particular focus on how the business might achieve further margin improvement.

Finally, tariff and trade policy commentary is also worth watching. This could cause cross-border delivery headaches and therefore impact performance expectations across the year ahead.

FedEx might be a more focused and leaner package, but can the business deliver significant improvements after its streamlining efforts?

Paychex

Paychex reports before the US open on Wednesday 24 June. The firm’s results will provide investors with a decent read on the US jobs market.

This is Q4 FY2026 and full-year results for the payroll and HR services group, covering the period ended 31 May. Analysts are looking for roughly $1.61bn of revenue and EPS of about $1.31.

Paychex’s core business depends on employers hiring staff, running payroll, managing benefits, and outsourcing HR admin. So these results should say something about whether smaller and mid-sized US businesses are still expanding, or quietly tightening their belts.

Paychex’s acquisition of HR software group Paycor has lifted reported growth, but it also makes the underlying organic picture more important. Investors will want to know whether Paychex is growing because the core business is healthy, or because M&A is doing more of the heavy lifting.

Paychex needs to show that its small business customer base remains resilient and Paycor is adding useful scale. A weaker print would be an early warning that the US jobs machine is becoming a little less well-oiled.

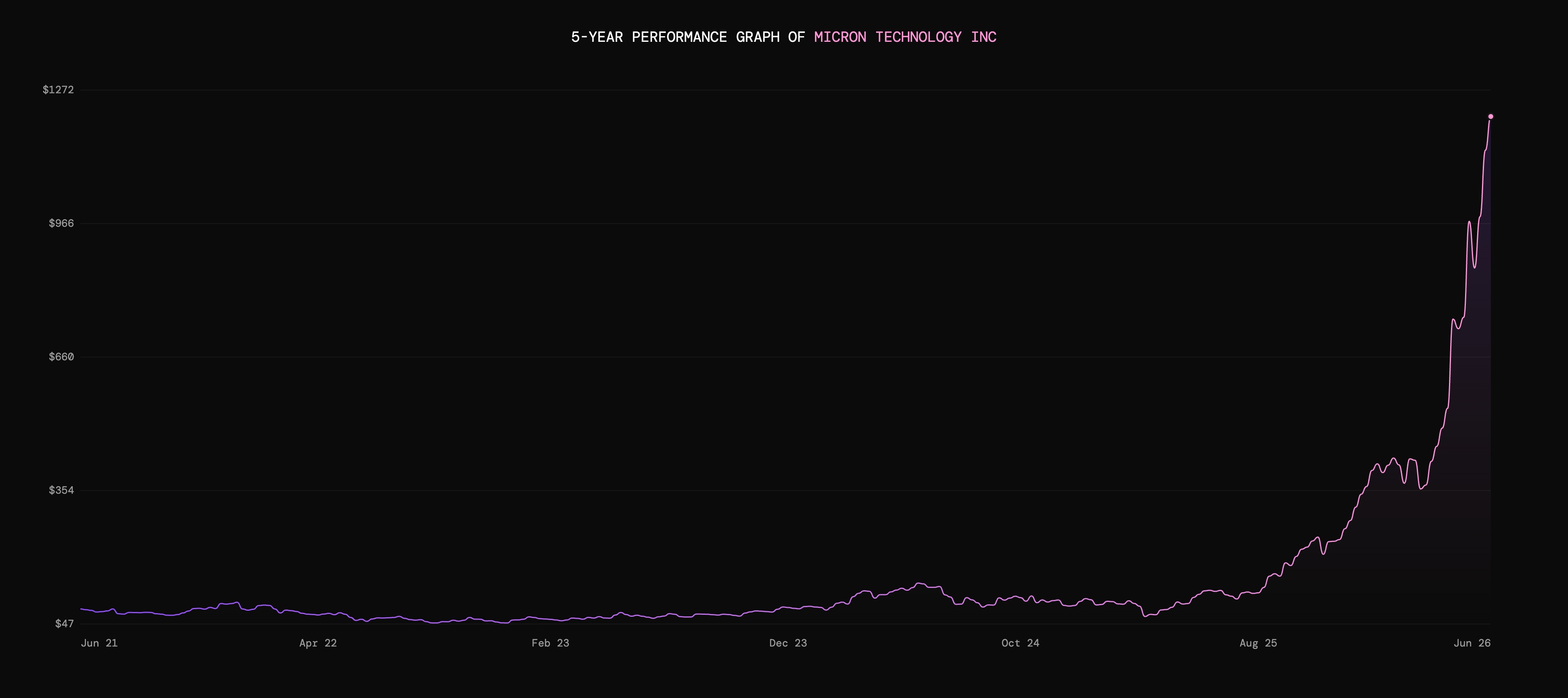

Micron Technology

Micron Technology’s Q3 2026 earnings are set for release on Wednesday after the market close.

Consensus analyst expectations are for the business to score quarterly revenues of $35.02bn and EPS of $20.05.

Back in Q2, Micron recorded 196.3% YoY revenue growth to $23.86bn. The quarter showed a rapid strengthening of gross margins, which climbed to 74.4% from 36.8% in the same period 12 months prior.

This rapid improvement came as Micron stood out as one of the major beneficiaries of the memory chip squeeze. For the uninitiated, demand for advanced Dynamic Random Access Memory (DRAM) and High Bandwidth Memory (HBM) has significantly outpaced supply as tech hyperscalers pour resources into the AI boom.

This has sent memory prices, and therefore margins, higher and higher. For the coming quarter, Micron has said it anticipates gross margins will climb above 80%.

This has all sent the company’s share price soaring, up by over 850% across the last 12 months. Micron is fairly uniquely positioned to benefit from the situation, with its only major competition coming from Eastern Hemisphere rivals SK Hynix and Samsung.

That US presence makes Micron a crucial cog in the United States’ AI hardware supply chain. Indeed, last time out, Micron’s chairman, CEO, and president, Sanjay Mehrotra, said memory was now a “strategic asset” for its customers, highlighting the business’s key role in ongoing AI buildout.

However, the kind of share price growth Micron has enjoyed comes with consequences.

For one thing, expectations will be high, and any sign that the current cycle has peaked or margin pressure could pose a problem. For example, HBM supply catching up with demand, or any softness in memory pricing, could rattle investor confidence.

There’s also the matter of investor behaviour.

Just this week, a tech sell-off in Korea sent Micron’s aforementioned rivals Samsung and SK Hynix tumbling. Micron followed suit, with its share price dipping by over 7% in premarket trading on Tuesday.

This highlights how precarious it can be after such a strong run. Enormous expectations and the potential for bouts of profit-taking mean Micron’s share price may slip even if its earnings update appears to be strong.

So, will Micron’s earnings be another rousing success, or has the bar become too high for the memory specialist?

Darden Restaurants

Darden Restaurants reports before the US open on Thursday 25 June.

This is Q4 FY2026 and full-year results for the owner of Olive Garden, LongHorn Steakhouse, Ruth’s Chris, Cheddar’s, and Yard House. Analysts expect EPS of around $3.64 on revenue of roughly $3.73bn.

Olive Garden and LongHorn have been two of the stronger brands in the group, helped by consumers still wanting to eat out, but being more selective about where.

Sales will be the number to watch. Darden has been guiding for solid full-year sales growth and restaurant openings, but the market will want evidence that growth is not just coming from new units, pricing or acquisitions. Traffic reveals whether diners are actually showing up.

Restaurants are still dealing with wage pressures and food costs. Investors will be watching whether Darden can protect profitability without pushing menu prices too far.

For Darden, a strong print would suggest brands like Olive Garden and LongHorn are still taking share from weaker rivals. A softer one would hint that even relatively resilient restaurant chains are starting to feel the pinch.

Capital at risk. The value of your investments can go down as well as up and you may get back less than you invest.

Fluctuations in foreign exchange rates may affect investments denominated in currencies other than GBP and the amount you receive back.

Past performance is not a reliable indicator of future returns.

Freetrade does not give investment advice and you are responsible for making your own investment decisions. If you are unsure about what is right for you, you should seek professional advice.

Always do your own research.