Earnings season may be quieter than usual this week, but updates from Accenture, Jabil, Kroger, and CarMax mean there are still plenty of insights for investors to sift through.

Accenture and Jabil should offer a read on the extent of AI disruption, and the strength of data centre demand respectively. As for Kroger and CarMax, this duo will offer insight into US consumer spending just as sentiment seems to have lifted from historic lows. Read on to explore the key issues to watch this week.

Jabil Circuit

.jpg)

Jabil Circuit releases its Q3 earnings before the market opens on Wednesday.

The company offers outsourced engineering, manufacturing, and supply chain services. Effectively, it helps businesses to design, build, and manage the complex electronics and components they need to make things like data centres, electric vehicles, consumer electronics, healthcare devices and more.

That means high-speed transceivers, battery systems, photonics systems, and more intricate bits and bobs.

Wall Street is anticipating quarterly revenues of $8.66bn and earnings per share (EPS) of $3.12.

Back in Q2, the business reported revenue of $8.28bn, up by 23.1% YoY, while net income increased by 89.7% YoY to $222m. On the back of this, the company lifted its guidance and noted it had “increasing confidence in the back half of the year”.

The source of much of this confidence is outperformance driven by AI data centre buildout, which is expected to continue over the near-term. The Intelligent Infrastructure segment comprised 49% of total revenue last time out, and its influence is likely to increase if Jabil can win more hyperscaler customers.

However, that’s not to say the business is a one-trick-pony.

The business has also highlighted improvements in the automotive, transportation, and energy spaces, which it has suggested shows recovery in demand after recent headwinds.

Margins are a bit of a sore spot though. Jabil is not a high-margin business like some other hardware beneficiaries of the AI boom. Core operating margin was just 5.3% in Q2, and this sits below its FY26 target of 5.7%.

While investors and observers alike will be keen for insights into the strength of AI infrastructure demand, the diversity of Jabil’s portfolio means it is not a picks and shovels pure-play. However, increased guidance and excitement about the sector may have contributed to the stock’s strong run.

Can Jabil live up to raised expectations, and can it bulk up its slim margins to align with FY targets?

CarMax

.jpg)

CarMax’s Q1 FY27 earnings are scheduled for release before the market opens on Wednesday.

This company is an auto-resale kingpin. It's the largest used-car retailer in the United States, and something of a bellwether for automotive retail and consumer discretionary spending.

Current consensus expectations are for revenue of $7.42bn and EPS of $0.94.

Last time out, things looked pretty bruising for CarMax.

The business is under significant pressure to make improvements. Used vehicle sales and average sale prices dipped in the last period, as the business cut prices in an effort to patch up momentum. This led gross profits to tumble by 9.4% YoY. In addition, the business paused its share repurchase program.

The company’s new President and CEO, Keith Barr, who took the top job in March, sought to assure investors:

“We are moving with urgency to improve execution, drive efficiencies, and sharpen our customer offering.”

These improvements are particularly important given how highly exposed CarMax is to consumer affordability and credit conditions. The business also faces rapidly growing competition from e-commerce used car retailer Carvana, which displayed strongly improved profitability last quarter.

But there are reasons to be positive.

CarMax is still the dominant player in terms of market share. And according to the University of Michigan’s Consumer Sentiment Index, American optimism has twitched back into life as prices at the gas pump dipped.

Amid these green shoots, will CarMax’s earnings update show turnaround plans accelerating, or will another downbeat update show a business running out of road?

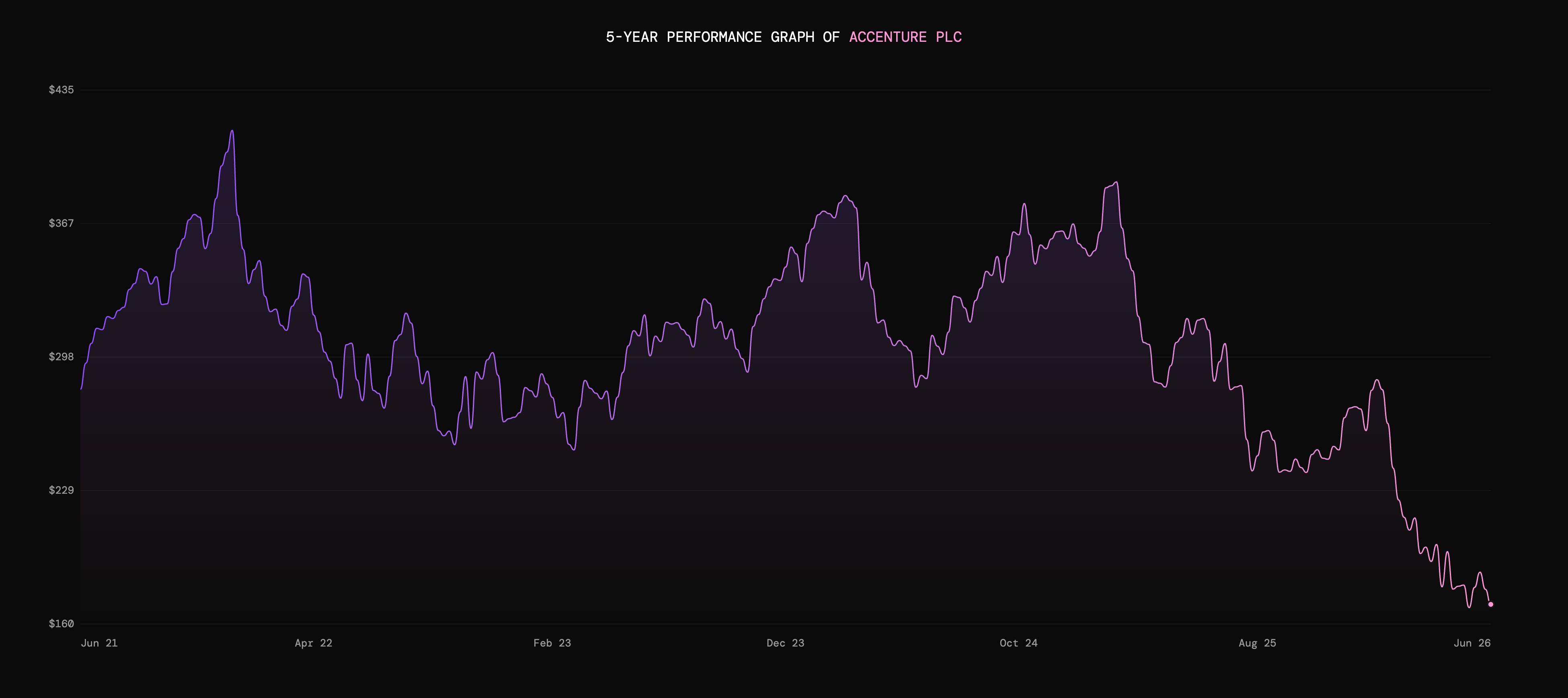

Accenture

Accenture releases its Q3 earnings report on Thursday morning, before the market opens.

The company operates largely as a professional services consultancy, helping other businesses to modernise business models and implement new tech. Accenture works with companies from a wide range of sectors, including financial services, healthcare, public sector, retail, and energy.

Consensus expectations are for the company to record Q3 revenues of $18.76bn and EPS of $3.71.

Back in Q2, US dollar revenues climbed by 8% to $18.04bn, or up by 4% in local currency. While helped by a more positive than anticipated foreign exchange impact, 5% local currency revenue growth from its Managed Services segment helped to drive revenues higher.

Margins also crept upward, with operating margin at 13.8% compared to 13.5% 12 months prior, though a higher effective tax rate kept net income roughly flat at $1.86bn.

Looking to the current quarter, the business said it anticipated revenues between $18.35bn and $19.0bn, with local currency revenue growth remaining in the low single digits and a slightly less positive impact from foreign exchange.

This might all sound like things are moving in the right direction, albeit unspectacularly. But Accenture’s share price is down by nearly 35% across the year-to-date.

There could be a few reasons for this.

One is that lower US federal spending has a significant impact, as the firm has historically been able to rely on government and public-sector revenues. AI is a complicating factor too. After all, if the automation it offers reduces the need for traditional consulting services, can Accenture’s current business model offer sustainable growth over the long term?

In an attempt to tackle this concern, Accenture launched a Reinvention Services business unit in 2025. This part of the company focuses on AI-led transformation, and could represent an opportunity for the business. Investors will be looking out for signs of tangible results from this restructuring.

So, will Accenture be able to produce the kind of cold hard results that will offset concerns about AI disruption and lower public spending?

Kroger

.jpg)

Kroger’s Q1 FY26 earnings update is scheduled to drop before the market opens on Thursday morning.

Kroger is a heavy-hitter in the US retail sphere. It operates a number of major supermarket and department store chains, including Dillons, Fred Meyer, and Harris Teeter, as well as its core Kroger brand. Despite its diverse array of regional brick-and-mortar grocery brands, it’s the company’s online segment that may catch the eye.

Consensus analyst estimates are for revenue of $45.49bn and EPS of $1.59.

In Q4 FY25, Kroger reported identical sales without fuel up by 2.4% YoY. Meanwhile, operating profit increased by 36.6% to $1.25bn and gross margins climbed by 40 bps to 23.1% even as the business invested in lower prices.

Looking at this week’s release, E-commerce has emerged as a key growth opportunity for Kroger to realise, and an increasingly crucial part of the business.

Across the FY, more than $16bn of total company sales came from the web. In Q4, ecommerce revenues grew by 20% and Kroger is targeting online profitability this year. After seven consecutive quarters of double-digit ecommerce growth, the company is still seeking means to accelerate the segment.

The downside is pharmacy. Here, the business faces headwinds from the Inflation Reduction Act, with reimbursement changes weighing on sales growth.

The company has stressed that performance from the segment is still strong, but it anticipates the legislation will contribute to a 130 basis point headwind to identical sales without fuel in 2026, meaning targeted growth of between 1-2%.

Can Kroger continue to deliver ecommerce growth at pace and meet its profitability goals, and will pharmacy pressure take the shine off its performance?

Capital at risk. The value of your investments can go down as well as up and you may get back less than you invest.

Fluctuations in foreign exchange rates may affect investments denominated in currencies other than GBP and the amount you receive back.

Past performance is not a reliable indicator of future returns.

Freetrade does not give investment advice and you are responsible for making your own investment decisions. If you are unsure about what is right for you, you should seek professional advice.

Always do your own research.