The earnings preview roster this week features Nike, Constellation, General Mills, and FactSet.

So, what’s going on with Nike’s turnaround plan? Why is demand for Constellation’s beer brands such an issue right now? Will General Mills’s price cuts get its products flying off the shelves? And could FactSet have turned an AI stumbling block into an opportunity? Find out everything you need to know below!

Constellation

Constellation’s Q1 FY2027 earnings are scheduled for release after the market closes on Tuesday.

This company is all about the booze. It’s one of the largest beer importers in the United States, boasting well-known brands like Modelo and Corona, and it has a broader portfolio of wines and spirits, too.

Despite the variety of its portfolio, the Beer segment is Constellation’s big kahuna. In FY2026, it comprised 91% of total net sales as the business shifted $8.3bn worth. However, sales fell by 3% across the full year, and margins tightened as depreciation and aluminium tariffs took a toll.

There were some signs of recovery in Q4, when the segment’s net sales edged 1% higher YoY.

Momentum is even less favourable in the Wines & Spirits segment, with organic net sales having dropped by 6% in the prior quarter. Meanwhile, operating margins capitulated last quarter, sliding from 21.7% to just 1.3%.

Here, Constellation is rebuilding after selling off parts of its lower-end wine portfolio as it aims to focus on the more attractive margins offered by premium brands.

Looking ahead, FY2027 guidance has not exactly been positive. The business is projecting that organic net sales growth will remain roughly flat in FY2027, though operating margins are expected to recover somewhat.

In its last earnings update, Constellation alluded to the problems it faces, as it said: “We expect the operating environment to remain dynamic given the evolving socioeconomic backdrop”.

Vague, right?

The socioeconomic backdrop Constellation appears to be referring to is the possibility that more selective shopping amid the ongoing cost-of-living crisis could weigh on beer consumption.

Can Constellation steady the ship, or even add a little fizz to its languishing share price, by reassuring investors that sales momentum will recover for its key Beer portfolio?

Nike

.jpg)

Nike’s Q4 FY2026 earnings are set to land after the stock market closes on Tuesday.

Right now, Nike is all about “Win Now”. That’s the title of new CEO Elliott Hill’s turnaround plan for the business. Ironically, management has warned that the Win Now strategy will hurt results for the rest of this calendar year.

Perhaps “Win Next Year” wasn’t a catchy enough name for the strategy.

Titles aside, the strategy is multifaceted but particularly concerns returning to the company’s sporting roots and expanding the business’s market reach by rekindling retailer relationships after overprioritising direct-to-consumer sales.

Investors already know the strategy is expected to weigh on results for the short term, but Nike faces other headwinds, too.

Chief among these is China. Here, the business has seen weakening sales in what was once one of its strongest growth markets.

The rise of domestic brands like Anta has not helped, and Nike has also faced criticism for losing focus in the market. Nike’s sales fell by 7% in the region back in Q3.

Finally, margins are proving to be another tricky spot. In Q3, gross margin fell by 130 basis points to 40.2%, with Nike citing higher tariffs in North America.

The reason US tariffs are so painful for the business is simple: North America is its largest market, and yet it makes almost none of its footwear or apparel there. Watch out for commentary on whether the business has reached peak margin pain, and whether mitigation strategies are starting to kick in.

Can Nike convince investors that its Win Now strategy has legs, and will it recapture sales momentum in China?

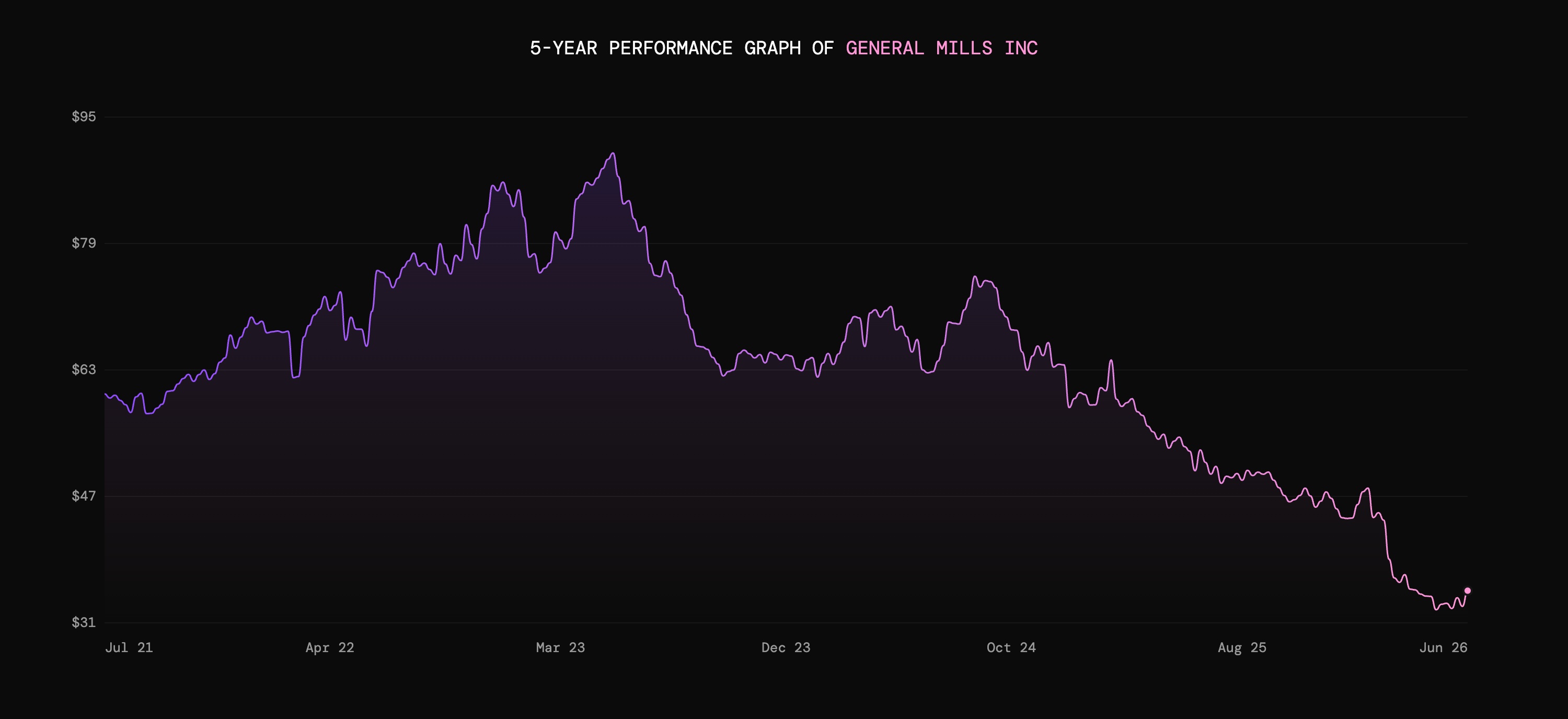

General Mills

Next on the docket is General Mills, which will release its Q4 FY2026 earnings update on Wednesday before the market opens.

Refinitiv data suggests consensus estimates of Q4 revenue of $4.59bn and EPS of $0.80.

The company owns a wide range of pantry staples, including Cheerios, Nature Valley, Häagen-Dazs, and Old El Paso.

While its brands might be instantly recognisable, General Mills is going through a tricky period.

Sales and profits have declined YoY in each quarter across its financial year to date. In Q3, net sales dropped by 8% to $4.4bn.

Ongoing ‘strategic divestitures’, or sales, spinoffs and disposals of different arms of the business, are a key driver of this decline. For example, just last week General Mills confirmed the planned disposal of Häagen-Dazs branded ice cream shops in mainland China.

This year has also been marked by investment in value, innovation, and price cuts.

The goal is a trimmed-down business that retains market share through lower pricing and improved relevance to shoppers. The business says these cuts have been well-received by customers, with an improvement in volume trends evident in Q3.

But cutting prices obviously puts pressure on margins. This was evident in Q3, when gross margin dropped by 310 basis points to 30.8%, primarily due to higher input costs.

Investors will of course want to see sales momentum, but they might balk if General Mills appears to be simply buying growth with aggressive price cuts and shrinking margins.

Either way, the company has already flagged that it expects a return to earnings growth in Q4, as it benefits from favourable comparatives, strong market share, and an anticipated improvement in sales trends.

But will Q4 actually constitute a return to form for General Mills, or will the period simply be less bad than the rest of what has been a challenging year?

FactSet

Finally, let’s look at FactSet. The company’s Q3 FY2026 earnings are set for release before the market opens on Wednesday.

Consensus estimates from Refinitiv suggest Q3 revenue of $618.25m and EPS of $4.46.

FactSet deals in numbers and graphs. It provides financial data, analytics, and tools to professional investors. It makes money by charging its clients, such as investment banks and asset managers, subscription fees based on the number of user seats and tools they need.

FactSet’s share price has been under pressure for over 12 months now.

Like many software players, it has faced concerns that generative AI may commodify parts of its offering. After all, why should businesses shell out for expensive data terminals and workflow subscriptions if AI has the potential to make financial analysis and dashboard-building so much easier?

In addition, the business faces competition from larger and more well-known names like Bloomberg, LSEG/Refinitiv, and S&P Global.

But could the business be turning a corner?

Its numbers looked pretty mixed last time out. Q2 organic revenue climbed by 6.8% to $606.18m, but net income fell by 8.1% to $133.06m. Operating margin tightened from 32.5% to 30.3%, but organic annual subscription value (ASV) rose by 6.7% to $2.45bn.

Ultimately, revenue growth looks steady, but perhaps not punchy enough to support the premium valuation investors once gave it. Sustaining and expanding growth now could be key.

Here, FactSet actually sees AI as part of the solution. It is embracing the tech with new AI-powered workflow tools, such as a document ingestion application for easy extraction and mapping of financial data.

Developing products costs money, though. FactSet CFO Helen Shan has partially attributed tighter margins to “accelerated technology spend on cloud infrastructure and AI tools”.

For investors, the key question will be whether these investments are worth it. Are they improving revenue and subscription growth without over-inflating FactSet’s cost base?

Capital at risk. The value of your investments can go down as well as up and you may get back less than you invest.

Fluctuations in foreign exchange rates may affect investments denominated in currencies other than GBP and the amount you receive back.

Past performance is not a reliable indicator of future returns.

Freetrade does not give investment advice and you are responsible for making your own investment decisions. If you are unsure about what is right for you, you should seek professional advice.

Always do your own research.

.png)

.avif)