US earnings continue with key updates from PepsiCo, Levi’s, Delta, and WD-40.

With Levi’s, investors will hear the latest on the denim giant’s shift towards direct-to-consumer sales, while PepsiCo’s earnings will show whether price cuts can revive snack volumes. For WD-40, we’ll see if the business is firing on all cylinders, while Delta will reveal whether premium travel demand can offset fuel cost pressures.

Levi's

First up is Levi’s, which reports its Q2 FY2026 earnings on Wednesday after the market closes.

Refinitiv data shows that Wall Street’s consensus expectations are for revenue of $1.52bn and earnings per share (EPS) of $0.24.

When you think Levi’s, you think jeans. Denim might be the company’s heritage, but at the moment it is on a mission to broaden its horizons. Polos, button-downs, sweaters, dresses, and more are now part of its expanding wardrobe. This considerably expands Levi’s addressable market, giving the company room to grow.

As the company aims for brand transformation, the name of the game is direct-to-consumer (DTC). In other words, selling through Levi’s own stores and online channels.

This channel now makes up more than half of its revenues. In theory, the benefits of DTC are stronger margins, more price control, better customer data, and better customer retention.

So far, it’s a strategy that seems to be translating to more sales.

Organic net revenues were up by 9% in Q1, following significant growth across each business unit.

The business raised FY guidance for revenue, margin, and earnings, citing a strong start to the year and positive trends. FY reported revenue growth expectations are now 5.5%-6.5%, while gross margins are slated to be flat or slightly up.

This may reduce pressure on Q2 earnings, as Levi’s may be able to impress investors by simply staying on track to meet this new higher bar.

There are some stumbling blocks to keep your eye on.

Tariff-based margin pressure is a key narrative to look out for. Back in Q1, operating margins were down by 110 basis points YoY at 11.4%, a dip which was largely attributed to tariffs.

On the bright side, the business has enjoyed particular revenue growth in Europe and Asia, somewhat reducing reliance on the US consumer story.

Even so, signs of an end in sight to margin pressure would be welcomed by investors, who may be concerned that the aforementioned tariffs, along with foreign exchange issues and higher marketing spend, could start to take a greater toll on the business.

So, is prioritising DTC the right fit for Levi’s, or will margin pressure start to pull at its seams?

PepsiCo

PepsiCo’s Q2 FY2026 earnings are set for release on Thursday before the market opens.

According to Refinitiv data, consensus analyst expectations are for revenue of $23.96bn and EPS of $2.21.

Back in Q1 FY2026, PepsiCo’s organic revenues were up by 2.6% YoY, helped by pricing changes and volume growth. Operating margins were also higher, up 210 basis points at 16.5%.

In the midst of intense competition in the snacks and beverages space, PepsiCo’s strategy has been to get out there and sharpen the value it offers to consumers.

Already, the business has cut prices of some of its signature snack brands, like Lay’s, Doritos, Cheetos, and Tostitos. And to be clear, this is not shrinkflation. The company is instead aiming to appeal to increasingly price-conscious customers as household budgets continue to tighten.

The business has already seen some success in the North American market, where Q1 convenience foods volumes improved following a weaker period for the division.

If PepsiCo can continue that momentum and get its North American beverage segment firing similarly, investors may be impressed.

With its European and Asia Pacific businesses proving resilient, PepsiCo’s overall numbers appear to show the business moving in the right direction.

However, it still faces several challenges.

The flipside of PepsiCo’s volume-led growth is margin pressure. While operating margins climbed last quarter, core operating margin, which excludes one-offs and restructuring costs, was up by just 10 basis points.

So, for investors there are two key questions.

With inflation continuing to loom in the background, can PepsiCo afford to keep rebuilding volumes through lower prices? And just how much volume improvement will be needed to put the fizz back into its share price?

WD-40

WD-40’s Q3 FY2026 earnings are slated for release on Thursday after the market closes.

Consensus analyst estimates see the company achieving quarterly revenue of $172.8m and EPS of $1.56.

For the uninitiated, WD-40 is best-known for its signature product, the distinctive blue and yellow aerosol lubricant you might have applied to bike chains, door hinges, rusty tools, or anything else that should be moving but isn't.

But the business has other products in its portfolio too, including Carpet Fresh carpet cleaner and Spot Shot stain remover.

Back in Q2, total net sales rose by 11% YoY to $161.7m. This was driven by a 13% increase in maintenance product sales, which now make up 97% of the total.

Gross margin edged 100 basis points higher to 55.6% following supply chain decentralisation initiatives, which have helped to shield the business against tariff impact and price increases.

However, it could still face margin pressure from high crude oil prices or costs associated with other specialty chemicals needed to make its lubricants and cleaning products.

It’s also worth noting that, while business in the Americas and Asia Pacific grew healthily, the Europe, India, Middle East, and Africa (EIMEA) segment could prove to be a weak link in the chain. Net sales in the region were up by 9% YoY during Q2, but benefited from favourable foreign exchange conditions. On a constant currency basis, sales would have declined by 3%.

Considering it made up 40% of total net sales last time out, continued weakness here could prove problematic even if strong momentum elsewhere is sustained.

Will the business turn around its fortunes in EIMEA, or will constant currency sales continue to slide?

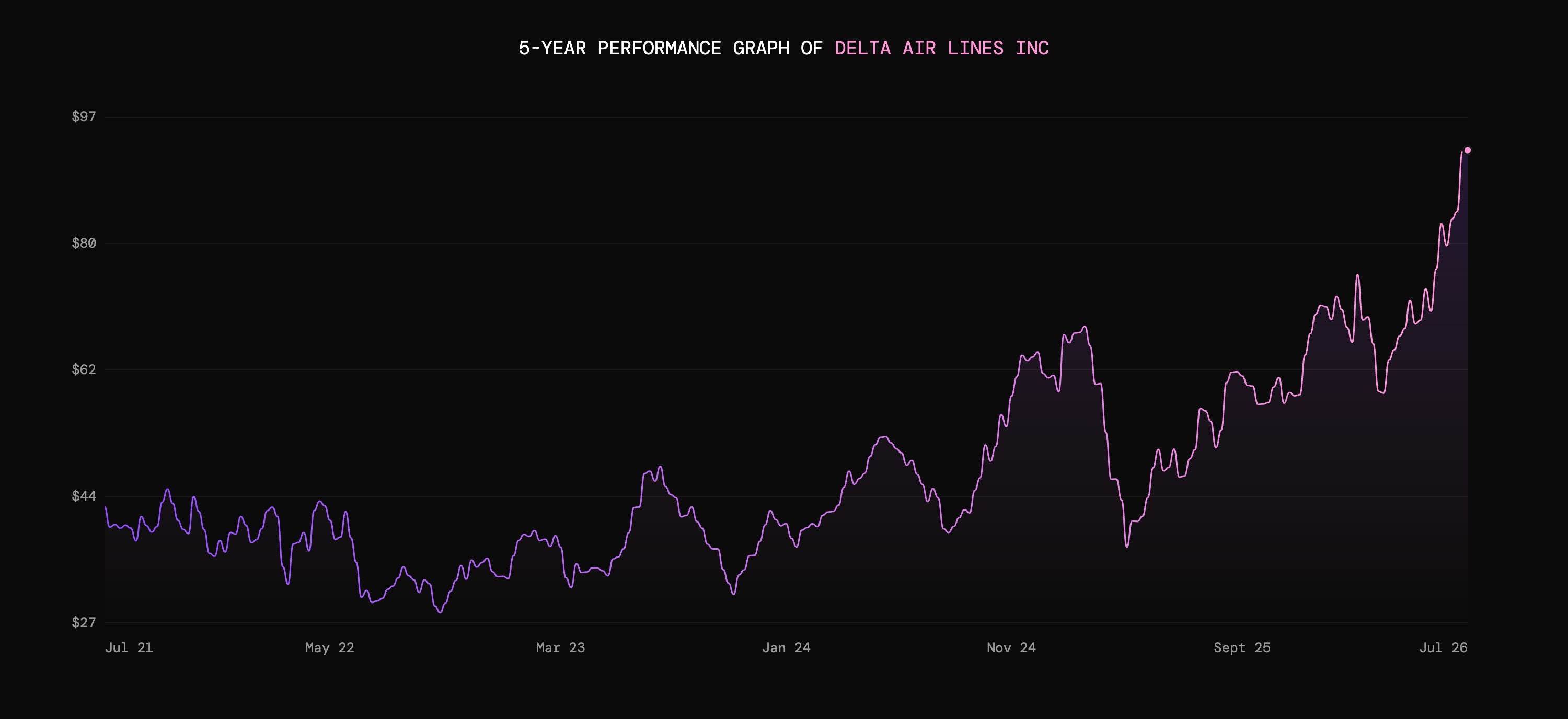

Delta

Delta’s Q2 FY2026 earnings update is coming in to land on Friday morning, before the market opens.

Analysts expect the business to deliver revenue of $17.62bn and EPS of $1.46, according to data from Refinitiv.

Back in Q1, adjusted revenues were up 9.4% YoY, driven by strength in premium cabins, corporate travel, and customer loyalty programmes. Adjusted operating income was $652m as adjusted operating margin came in at 4.6%.

Adjusted fuel expenses rose by 8% compared to the same quarter 12 months prior, and further pressure is anticipated in Q2. Investors will look for commentary on the impact of fuel prices moving lower, and whether Delta has leveraged its relatively advantaged position thanks to a wholly owned refinery in Pennsylvania.

Even so, fuel costs are set to bite.

But they do make Delta’s high-margin premium customers all the more important. Last time out, premium revenue grew by 14% as the business continued retrofitting aircraft interiors to increase the amount of premium seating on each flight.

Aside from offering higher margins, the apparent upside of attracting a greater number of premium customers is their resilience. Speaking during Delta’s Q1 earnings call, CEO Ed Bastian commented:

“I think the higher-end consumer, the premium consumer is candidly immune or becoming more immune to the headlines and not delaying their investment in the experience economy, waiting to see what the next headline's going to be on the margin.”

Will Delta’s shift towards the premium market keep margins airborne even as the business faces cost pressures from jet fuel prices?

Capital at risk. The value of your investments can go down as well as up and you may get back less than you invest.

Fluctuations in foreign exchange rates may affect investments denominated in currencies other than GBP and the amount you receive back.

Past performance is not a reliable indicator of future returns.

Freetrade does not give investment advice and you are responsible for making your own investment decisions. If you are unsure about what is right for you, you should seek professional advice.

Always do your own research.

.avif)

.avif)